Q1 companies’ reporting is better than expected, however investors are taking this with cautiousness. Large caps look quite resilient, mid-cap tech stocks, by contrast, were sent lower, marking the traders’ intention to cut risk.

Q1 reporting comments.

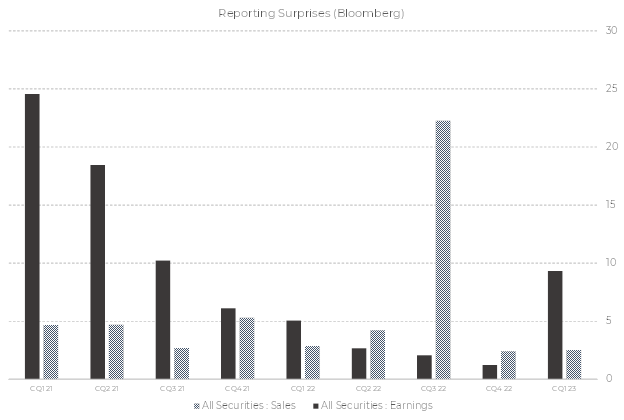

Q1 reporting seems one of the best reporting periods over the past two years:

Figure 1

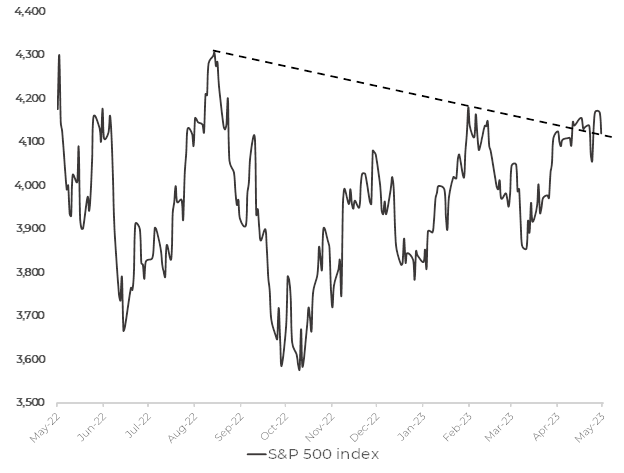

S&P 500 index has stalled, though, near its resistance level (Figure 2). Risky stocks behave much worse: the ARK ETF has lost 13% respective to S&P 500 since the beginning of April. Pinterest (PINS) is a bright example: having beaten both earnings and revenues expectations, the company’s stocks were sent 20% down immediately after reporting. The investors badly took the Pinterest CEO Bill Ready’s words about ongoing stagnation in the Ad market.

In fact, it is not a surprise that the economy is going to grow at a low rate in quarters to come. This was explicitly said by various top US financial officials. It is also hard to imagine the growing Ad market on the back of stagnating economy. META’s reporting, by contrast, revealed some optimism about the near future. The company also beat expectations, but its shares jumped to their significant resistance level of 240. It does not look probable that both companies, operating in one field, are going to experience opposite trends. It is more likely that META’s results were influenced by the US restrictions in Tik-Tok. In this case this jump can be a one-off.

Figure 2

The common impression from the Q1 reporting is that investors are waiting for ‘magical’ tools helping companies to weather an upcoming recession. Once they find out that such a tool does not exist, they cut risk.

We have already highlighted the situation in the banking sector. Almost all banks showed a record income, but the ongoing bank run, and poor economy prospects do not allow the bank stocks to grow.

Car dealers are in the same situation. Ford motors reported $.63 of EPS (vs expected $.40) and $39bn of revenues that matches an upper bound of expectations range. The investors’ reaction was sending the stock 2% down.

It is interesting that Ford is expecting 4.4 million cars to be sold in 2023 versus 6.6 million cars in 2016 with revenue remaining unchanged. The profit margins have expanded respectively. This is pure inflation pressure. The company realizes that and warns of ‘Opaque’ 2023 outlook.

The most dramatic swings in the labor market happened in the sector of leisure and restaurants. The companies in this sector also feel the inflation pressure resulting in high demand for their services accompanied by the lack of workforce. As an example, Marriott hotels (MAR) reported $2.09 EPS vs 1.85 expected and $5.6bn of revenue beating expectations by a quarter of billion. The whole Q1 report looks solid except for the number of rooms and number of locations growing at a 0.5% rate. This is lower than an average level of 1-1.5%. As in the case of Ford, we see contracting real figures and expanding margins.

The best performing sector so far is consumer discretionary with e-commerce playing the leading role (Amazon, Overstock). In a discretionary retail the champions are Avis, Hertz and Sleep Number Corporation mirroring the hot situation in the leisure sector.

Tech stocks also beat expectations on average. Tech hardware and semiconductors strongly underperform, while software services are in a much better form. The picture inside the sector is quite motley, though.

Tenable (TENB), Alterix (AYX) and Cloudfare (NET) provided solid earnings, but the market reaction to reports was very negative resulting in significant downward gaps in stock prices.

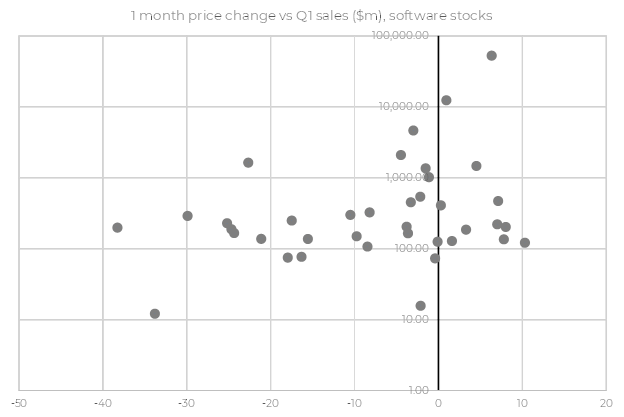

Microsoft (MSFT), Microstrategy (MSTR) and several other stocks gained after reporting. Figure 3 demonstrates that large cap stocks are more resilient in current market conditions. Investors are less nervous holding stocks of mature companies with predictable profits and a better market position. Small caps do not meet bad attitude if they manage to convince investors of their unique capability of maintaining growth no matter what condition the market is.

Figure 3

Summary

The overall impression of the Q1 reporting season is that investors do not care what companies are demonstrating unless it is something very bad or very good. On average the US companies beat expectations, but the risk of potential recession prevails in investors’ minds.

It looks like investors take it seriously that the growth of the tech sector can be over, so that companies can remain in their current financial condition for long. No one doubts that the large caps will hold their market position. Smaller companies which have not reached their targeted market share with profits fluctuating around the breakeven level raise questions. For example, the revenue of Pinterest, with its better-than-expected reporting, has only grown 4.6% YoY. Its profit margin has not gone solidly above nil.

The same is fair for other companies. So, the macro environment is becoming the major factor driving stocks, individual reporting has become secondary.