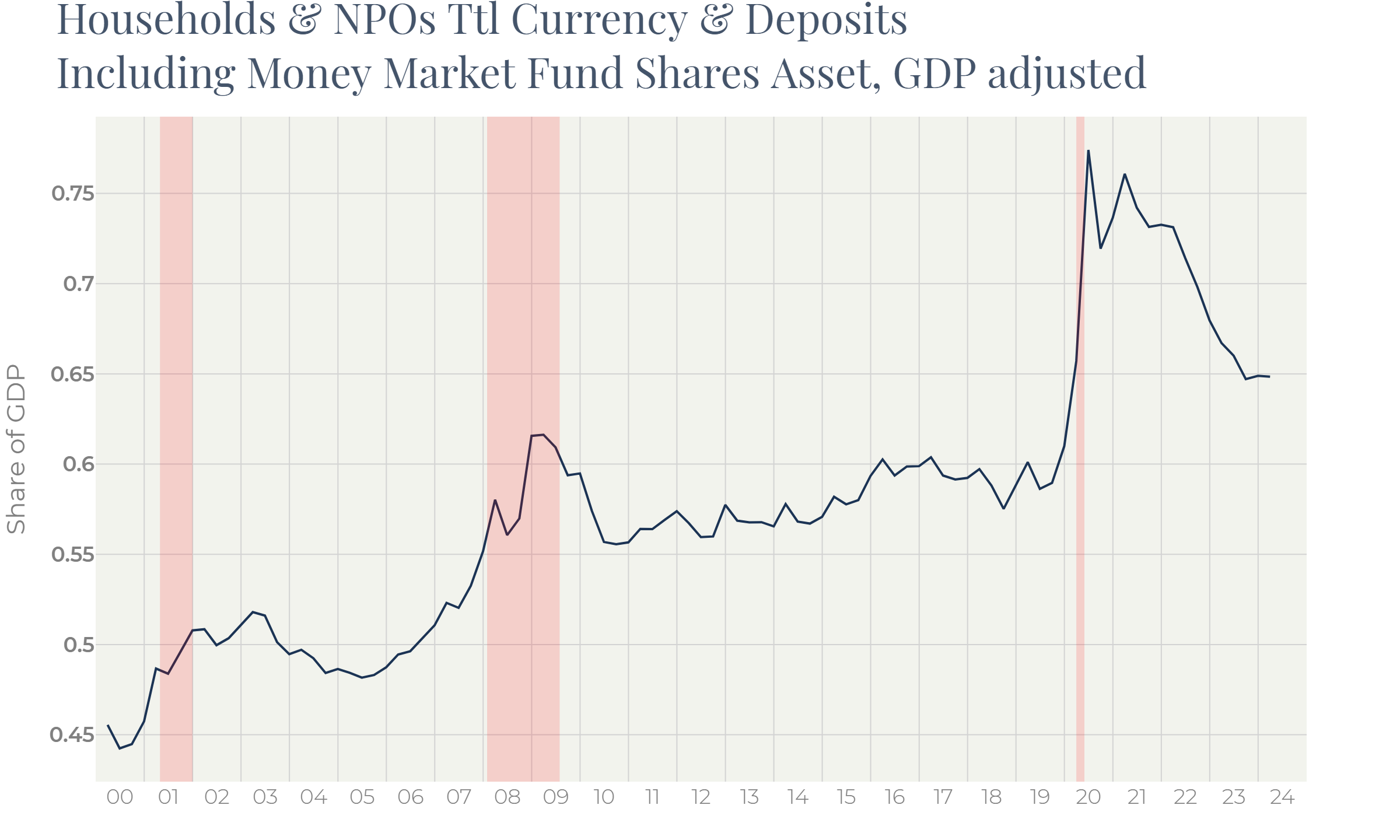

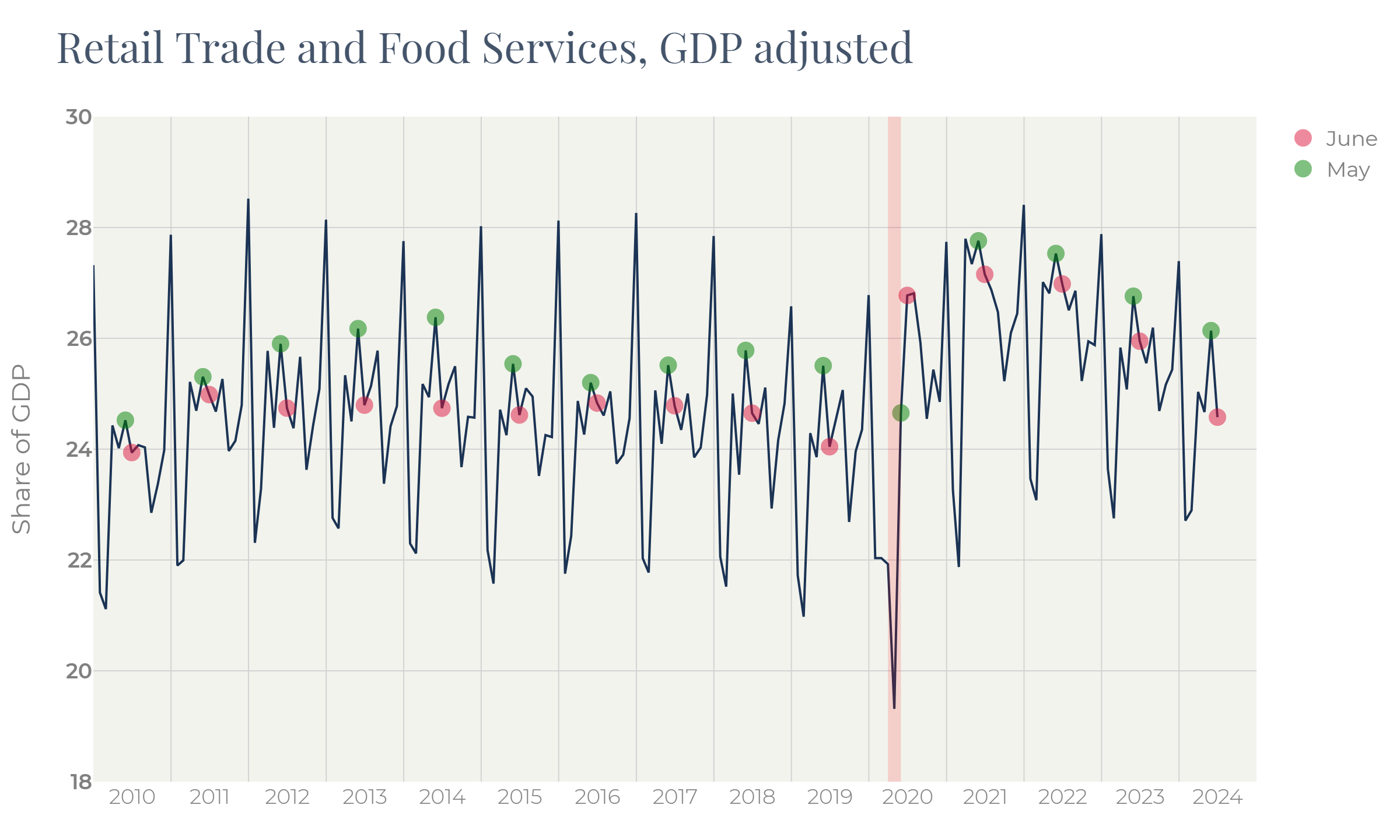

Consumer spending is probably the most important gauge of the current economic conditions. Household savings are returning to the pre-pandemic levels, the share of Retail Sales in the GDP structure is nearly there as well.

Figure 1

Figure 2

This note is the selected commentaries of US corporations on the way they assess consumer demand.

According to most companies, consumers are becoming more sensitive to price levels and shift their preferences to less pricy segments. It is more typical of low-income consumers:

• Home Depot highlight weakness in big ticket items,

• Costco talks about pricing pressure in the fresh food segment,

• Airbnb and Booking noticed slower demand from non-US residents, shorter booking lead times and decrease in Q2/Q1 booking window (Booking),

• McDonalds, Starbucks and Coca-Cola highlight the gap between home and away-from-home inflation which put pressure on restaurants spendings,

• GM and Ford said they feel pricing headwinds with retail clients displaying more skepticism,

• Both Tractor supply Co and Disney mention stress in the low-income consumer segment and week domestic demand on the back of high-income consumers traveling internationally,

• Target commented on 1 in 3 American families nearing their limits on credit cards.

More positive commentaries came from Costco, Netflix and companies exposed to e-commerce. In some cases, we can observe idiosyncratic stories: for example, Netflix points to the shift to advertising, which means that the company is gaining its share in the Ad sector offsetting weak consumer demand by that. Another example is Shopify which benefits from the ongoing migration to online. Costco is a typical consumer staple offering good with less margins and therefore most resilient against drops in consumer demand.

Brief Summary of Q2 2024 AMZN earnings call

In the Q2 2024 earnings call, Amazon expressed cautious optimism regarding the macro environment and consumer demand. Despite a challenging environment where customers are being more careful with their spending, evidenced by a tendency to trade down on price and prioritize lower ASP (Average Selling Price) products, the company saw solid growth in certain areas.

Opinions on the Macro Environment and Consumer Demand:

1. Consumer Spending Behavior :

• Consumers continue to trade down, seeking lower-priced items and deals.

• Discretionary spending on higher-ticket items like computers, electronics, and TVs has been slower, reflecting broader economic conditions.

2. Sector-Specific Trends :

• Essentials and everyday items have shown robust growth, driven by improved delivery speeds and strong operational performance.

• On AWS, despite significant capital requirements, investments in Generative AI, custom silicon (like Trainium and Inferentia), and modernized infrastructure are seen as sustainable growth drivers.

• The advertising sector, especially sponsored ads, remains a bright spot, contributing significantly to profitability.

Signs of Weakness in Demand :

1. Average Selling Prices (ASPs) :

• There continues to be a noticeable trend where consumers opt for lower-priced items.

• Higher-ticket discretionary items are not seeing robust growth compared to essentials.

2. Regional Discrepancies :

• The North America segment’s unit growth outpaced sales growth due to trading down.

• International segments also exhibited careful spending but were bolstered by better cost structures and inventory placements.

3. Margins Under Pressure :

• Intensive investment areas like Project Kuiper and stock-based compensation have impacted operating margins.

• Retail gross margins were slightly weaker than anticipated due to discounting and investments in new initiatives.

Overall, while Amazon acknowledges ongoing macroeconomic pressures and shifts in consumer spending behavior, the company remains focused on long-term investments in AWS, AI, advertising, and improved operational efficiency. The balance between cost management and strategic investments is aimed at sustaining growth and enhancing customer value.

Brief Summary of Q2 2024 EBAY earnings call

During the second quarter 2024 earnings call, eBay's management discussed various aspects of the company's performance and offered insights into the macro environment and consumer demand. Here's a summary of their views:

Macro Environment and Consumer Demand Insights :

1. Continued Macro Headwinds and Uncertainty :

• eBay acknowledged that Q2 was influenced by ongoing macroeconomic headwinds, geopolitical uncertainty, and evolving regulatory landscapes. The company noted the challenging nature of the current environment several times.

2. Demand for Value Products :

• eBay highlighted that consumers are increasingly searching for value due to the economic backdrop. This trend has benefited the company as 40% of their products are used or refurbished. These product categories have consistently outpaced the sales of new goods.

• Jamie Iannone commented on the pressures faced by less affluent customers but mentioned that eBay's focus on trust, value, and quality in refurbished products, among other areas, has successfully resonated with this segment.

3. Uneven Discretionary Spend :

• Steve Priest pointed out an uneven discretionary demand environment in key markets, noting softness specifically in discretionary spending areas, which has been a trend affecting GMV.

4. Geographical Variances :

• The company mentioned challenging economic conditions, particularly in Germany, and emphasized that their C2C initiative in Germany has helped navigate these challenges by sustaining positive growth.

• There were also mentions of pressures in the U.K. around new digital sales reporting requirements impacting the C2C volumes.

5. Specific Signs of Weakness :

• Regional Challenges: Both the UK and Germany were highlighted as experiencing economic pressures. This includes uneven discretionary demand and regulatory challenges impacting consumer activity.

• Discretionary Spend: The overall environment for discretionary spending in major markets appeared uneven, affecting general merchandise volume (GMV) growth.

Overall, while eBay demonstrated resilience and positive growth in certain areas, the macroeconomic pressures and demand weaknesses were clearly recognized and acknowledged during the call.

Brief Summary of Q2 2024 ETSY earnings call

Macro Environment and Consumer Demand

During the call, Etsy acknowledged facing stiff macroeconomic headwinds impacting their type of goods. The company noted that consumer discretionary product spending remains under pressure, which was evident in GMS performance. Although the macro environment has been volatile and pressures from external factors persist (e.g., holidays, political events), Etsy conveyed cautious optimism, continuing to invest in initiatives to drive growth despite these challenges.

Signs of Weakness in Demand

Etsy mentioned specific signs of demand weakness during the call:

• Overall GMS declined by 2.1% year-over-year, with Etsy marketplace GMS down 3.2%.

• Types of goods such as lower-priced jewelry under $10 faced significant demand pressure.

• New buyer additions were down 9% year-over-year, though the decline moderated sequentially.

• GMS per active buyer decreased by 3.2%, continuing to show signs of stabilization.

However, Etsy also highlighted areas of improvement, such as growth in specific segments like demifine jewelry and stronger performance in gifting categories.

Brief Summary of Q2 2024 RVLV earnings call

Opinion on Macro Environment and Consumer Demand :

Revolve Group expressed a cautiously optimistic view on the macro environment and consumer demand during their Q2 2024 earnings call. They noted strong performance in their REVOLVE segment with a 4% year-over-year increase in net sales, their best performance in six quarters. However, they acknowledged continued headwinds in the dynamic luxury environment, particularly affecting their FWRD segment.

Signs of Weakness in Demand :

Yes, the company mentioned signs of weakness in demand, particularly within the FWRD segment. They observed a 4% decline in FWRD segment net sales, an improvement from the previous quarter, but indicative of challenges in the luxury market. They referred to this as "headwinds in a dynamic luxury environment" but positioned themselves as a financially strong operator actively pursuing strategies to capture market share through strategic acquisitions and other initiatives.

Additionally, the company referenced broader trends in the industry, noting recent industry disruptions and the closure of other luxury retailers such as Matches Fashion, signaling broader market turbulence.

Overall, while there is optimism based on improved marketing efficiency, logistics efficiency, and international growth, challenges remain, particularly in the luxury segment, which reflects the mixed nature of the current consumer demand environment.

Brief Summary of Q2 2024 ABNB Earnings Call

Macroeconomic Environment and Consumer Demand :

The company expressed a positive outlook on the macro environment, marking Q2 2024 as another strong quarter, with significant milestones like an 11% revenue increase year-over-year and the highest-ever trailing 12-month free cash flow of $4.3 billion. However, they acknowledged signs of demand volatility driven by global macroeconomic pressures. They are closely monitoring these trends while continuing to invest in less penetrated markets and new offerings.

Signs of Weakness in Demand :

1. Shorter Booking Lead Times : Ellie Mertz noted a recent trend toward shorter booking lead times, particularly in July, where there's strong growth in last-minute bookings but a notable softening in long-term bookings (two months or more ahead). This behavior differs from Q1 and Q2, which saw lead times equivalent to those in 2023.

2. Slowing Demand from U.S. Guests : Brian Chesky mentioned observing some signs of slowing demand specifically from U.S. guests.

3. Regulatory Impacts : The new regulations in California beginning July 1st on total price display and cancellation grace periods have had a modest headwind on their business in that state, which impacts about 10% of their gross booking value (GBV).

While these signs indicate a cautious outlook, the company remains optimistic and committed to its growth strategy, which they believe will counterbalance any temporary macroeconomic trends.

Brief Summary of Q2 2024 BKNG Earnings Call

During the Q2 2024 earnings call for Booking Holdings (BKNG), the company expressed a cautiously optimistic view on the macro environment and consumer demand, notwithstanding certain challenges. Below are the key takeaways:

Macro Environment and Consumer Demand

• Overall Market Normalization : The travel market continues to normalize following pandemic disruptions. This normalization aligns with the company's expectations.

• Strong Underlying Business : BKNG reported robust underlying business performance with year-over-year increases in key metrics such as room nights, revenue, and adjusted EBITDA, despite macroeconomic uncertainties.

Signs of Weakness or Concern

• Booking Window Trends : There was a noted decrease in the year-over-year expansion of the booking window in Q2 compared to Q1. This potentially signals a more cautious consumer sentiment.

• Regional Performance Variations : A mild moderation in the travel market growth was observed in Europe, though BKNG's performance remained stable relative to the market. Asia showed high growth levels, and the U.S. saw a slight improvement.

• Third Quarter Outlook : BKNG expects a similar expansion of the booking window in Q3 as seen in Q2, potentially translating to a deceleration in room night growth. The company anticipates slower growth in gross bookings partly due to a slight decline in accommodation ADRs and lower flight ticket prices.

Confidence in Long-Term Growth

• Strategic Initiatives : BKNG remains confident in the long-term growth profile of the travel industry and continues to focus on strategic initiatives:

• Expanding its connected trip offering.

• Enhancing AI capabilities.

• Growing alternative accommodations.

• Developing the Genius loyalty program.

• Cost Efficiency Measures : The company is also taking measures to drive cost efficiency and improve operating leverage, evidenced by actions to carefully manage fixed OpEx growth.

Specific Weakness Indicators

• Europe Market Growth: Despite steady internal performance, the overall travel market growth in Europe has shown some mild signs of slowing over recent months.

• U.S. Market Slight Trade Down: The company highlighted a mild indication of consumers trading down in the U.S. market, suggesting some sensitivity to price or economic conditions.

Strategic Responses

• Increased Direct Bookings : A continued shift toward growing the direct booking channel is noted, with the Genius loyalty program playing a significant role.

• Alternative Accommodations : With strong growth in this segment, the company is committed to increasing its listings, highlighting an 11% year-over-year growth in global alternative accommodation listings.

• Marketing Adaptations : The company is leveraging more social media marketing channels due to their attractive incremental ROI, and is also optimizing its marketing spend for better returns.

Conclusion

Through focused initiatives and an adaptable marketing strategy, BKNG continues to show resilience in the face of macroeconomic challenges, positioning itself for sustainable long-term growth despite some near-term moderation in consumer behavior and market conditions.

Brief Summary of Q2 2024 MCD Earnings Call

Overview of Macro Environment and Consumer Demand

During the Q2 2024 investor call, McDonald's highlighted several observations about the macro environment and consumer demand:

• The company had previously noted a more discriminating consumer, especially within lower-income households, a trend which has now deepened and expanded.

• The Quick Service Restaurant (QSR) sector has significantly slowed in most markets with noticeable declines in industry traffic in major markets including the US, Australia, Canada, and Germany.

• External factors such as the war in the Middle East have further impacted performance in several regions.

Signs of Weakness in Demand

McDonald's detailed several signs of weakness in consumer demand:

• Traffic Decline : Major markets (e.g., US, Australia, Canada, Germany) saw a decline in industry traffic.

• Financial Pressure : Lower-income consumers and larger family groups, especially in Europe, have become more deliberate with their spending.

• Macro-economic Factors : A 300 basis point gap persists between food at home and food away from home inflation, leading to consumers increasingly choosing to eat at home.

• Market-Specific Challenges :

• France: Facing both broader market slowdown and market share loss due to aggressive pricing from competitors and cultural factors tied to demographics (e.g., higher Muslim population affected by the war in the Middle East).

• China: A highly promotional market with weak consumer sentiment, leading to frequent deal-seeking behavior from consumers.

Strategic Responses

Despite these challenges, McDonald's outlined several strategic actions:

• Value Execution: Emphasized reasserting leadership in providing value through initiatives like the $5 meal deal in the US, which has shown positive results in shifting consumer sentiment and trial rates among lower-income consumers.

• Menu Innovation: Focus on core menu improvements including the roll-out of the Best Burger recipe in majority markets, and piloting new burger offerings like "The Big Arch" in international markets.

• Digital Growth: Strong focus on growing digital engagement with a loyalty membership goal of 250 million members and enhancing personalized customer experiences through their app.

• Marketing and Promotions: Continued to adjust marketing strategies to increase brand relevance and consumer engagement through promotional offers and localized campaigns.

Conclusion

McDonald's acknowledges the challenging macro environment and current weaknesses in demand. However, they remain committed to leveraging their brand strength, innovative menu, digital engagement, and tangible value offerings to regain market share and drive future growth.

Brief Summary of Q3 2024 SBUX Earnings Call

During the Q3 2024 earnings call for Starbucks (SBUX), the company outlined its current performance and its insights on macroeconomic conditions and consumer demand:

Opinion on Macro Environment and Consumer Demand :

Starbucks acknowledged the challenging macroeconomic environment, noting cautious consumer spending particularly away from home. The company highlighted persistent challenges and significant disruptions in some of its international markets, especially China, due to intensified competition and economic headwinds.

Signs of Weakness in Demand :

• Global comparable store sales declined by 3% year-over-year, driven by a 2% decrease in North America and a sharp 14% decrease in China.

• The company identified a significant decline in transactions, primarily among non-Starbucks Rewards members in the U.S.

• Weaker consumer spending was particularly noted in parts of Europe and China, with the latter facing competitive market dynamics, aggressive store expansion by competitors, and price wars.

• While Starbucks Rewards membership and member engagement in the U.S. showed growth, broad customer traffic remained a point of concern, reflecting the cautious consumer environment.

Overall, Starbucks expressed dissatisfaction with the current results but remained optimistic about the future, buoyed by various strategic initiatives aimed at improving operational efficiencies, enhancing the customer experience, and targeted product innovations.

Brief Summary of Q2 2024 TSCO Earnings Call

Opinion on the Macro Environment and Consumer Demand :

During the Q2 2024 earnings call, Tractor Supply Company (TSCO) expressed a cautiously optimistic outlook on the macro environment and consumer demand. The company noted that the macroeconomic indicators were mixed and consumer spending on goods seemed fatigued across income cohorts.

• Economic Indicators : Improvements were noted in the consumer inflation rate, but unemployment had ticked upwards to its highest rate since late 2021. Consumer sentiment and confidence were subdued, contributing to a choppy consumer spending landscape.

• Retail Sales : The company observed that overall U.S. retail sales for the second quarter were flat to modestly positive, especially with growth in non-durable categories. However, the farm and ranch channel experienced mid-single-digit declines, indicative of Tractor Supply's continued share gains in the channel.

Signs of Weakness in Demand :

TSCO highlighted several signs of weakness in consumer demand:

• Consumer Sentiment and Confidence : Both were described as subdued.

• Moderating Customer Cohorts :

• Higher income customers showed slight moderation in spending due to increased vacation travel.

• Lower income customer cohort showed sequential moderation up from the first quarter.

• Non-Core Customer Disengagement : There was a slight disengagement of non-core customers, attributed to macroeconomic headwinds and fatigue from prolonged inflation and higher living costs.

Overall, despite these challenges, the company's results for the first half of 2024 fell in line with their expectations, showing a nuanced but steady performance amidst a challenging macro environment.

Brief Summary of Q1 2025 TGT Earnings Call

Opinion on the Macro Environment and Consumer Demand

During the Q1 2025 earnings call, Target Corporation (TGT) expressed a cautious yet optimistic stance regarding the macro environment and consumer demand. The company acknowledged the challenges posed by elevated prices and higher interest rates, but it highlighted the resilience of U.S. consumers despite these adversities. Target noted that consumers are gradually shifting their spending away from home-related categories and back into services and entertainment, a trend that began more than two years ago.

Target also mentioned a notable improvement in discretionary spending trends, particularly in the Apparel segment, signaling some optimism for a better balance between discretionary and essential spending in the future. However, the company remained cautious about the near term due to continued uncertainty around the economy, social and political divisiveness, and the upcoming election cycle.

Signs of Weakness in Demand

Target did highlight specific areas where demand remained weak. The home and hardlines categories experienced continued softness, with softening trends also observed in frequency categories. Christina Hennington, Chief Growth Officer, pointed out that the sustained high prices have impacted budgets and savings for many families, with 1 in 3 Americans maxed out or nearing the limit on at least one of their credit cards. This financial strain indicated a pressure on discretionary spending, leading to declines in Home, Hardlines, and frequency categories.

Comparable sales for the first quarter were down 3.7%, driven largely by the said soft trends in Home and Hardlines categories, as well as reduced benefits from price as compared to a year ago. This suggests a prevailing caution among consumers and a preference for essential over discretionary items given the economic backdrop.

Brief Summary of Q1 2024 HD Earnings Call

During Home Depot's investor call for Q1 2024, the company emphasized several key aspects about the macro environment and consumer demand.

Macroeconomic Environment and Consumer Demand

• Macro Environment Concerns: HD acknowledged a challenging macro environment, highlighting the impact of a delayed spring season and ongoing softness in larger, discretionary projects.

• Consumer Behavior: They noted that customers were more cautious, particularly with large, financed projects such as kitchen and bath remodels. The company mentioned a "deferral mindset" related to the uncertainty around interest rates.

• Regional Variations: In regions where the weather was favorable, HD saw strong engagement and robust performance, especially in outdoor projects.

Signs of Weakness in Demand

• Drop in Big Ticket Items: There was a noticeable reduction in big-ticket transactions (items over $1,000), which were down 6.5% compared to the same period last year. Categories like kitchen and bath remodels, which often require financing, were specifically mentioned as areas of softness.

• Decreased Comp Sales: Comp sales declined 2.8% from the same period last year, with U.S. stores experiencing a steeper decline of 3.2%.

• Pro and DIY Customers: Both Pro and DIY customer segments were negative for the quarter. The company noted that homeowners continue to take on smaller projects rather than large ones.

Commentary on Future Outlook

• Spring and Seasonal Trends: HD remains hopeful for improved performance as spring progresses, anticipating better weather ahead which could uplift sales. There was optimism around strength seen in outdoor categories during favorable weather.

• Pro Ecosystem Expansion: The company continues to invest in its Pro ecosystem, aiming to capture a larger share of the Pro contractor market.

• Maintaining Investments: Despite market pressures, HD emphasized its ongoing investments in the business including adding new stores and technology enhancements to improve the shopping experience.

Overall, while HD is facing some demand headwinds related to the macroeconomic environment and large, discretionary projects, the company remains confident in its strategic initiatives and future growth prospects, particularly with Pro customers and in regions where weather conditions improve.

Brief Summary of Q3 2024 COST Earnings Call

Opinion About the Macro Environment and Consumer Demand :

During the third quarter 2024 earnings call, Costco expressed a cautiously optimistic view on the macro environment and consumer demand. The company highlighted several key indicators of consumer behavior and economic sentiment:

• Inflation Trends: The company noted that inflation has essentially leveled off, with fresh foods experiencing close to zero inflation and a slight increase in food and sundries prices being offset by deflation in non-food categories.

• Discretionary Spending: Costco observed a return to more discretionary spending by its members, signaling possible stabilization or improvement in consumer sentiment. Categories such as toys, tires, lawn and garden, and health and beauty aids saw significant growth.

• Member Traffic and Engagement: Traffic or shopping frequency increased by 6.1% worldwide and 5.5% in the U.S. Additionally, the company saw growth in average transaction size, concluding that its strategy of delivering high-value items resonates well with consumers.

Signs of Weakness in Demand :

While Costco did not emphasize significant weakness in demand, certain nuances in their commentary indicated some areas of cautious observation:

• Consumer Behavior: There was a keen emphasis on managing competitive pricing, particularly in fresh foods and other essential categories, indicating that the company is sensitive to any shifts in consumer spending habits due to economic uncertainty.

• Non-food Deflation: The company acknowledged deflation in non-food categories like hardware, sporting goods, and furniture, suggesting some lingering effects from previous inflationary periods and potential softness in these areas.

• Careful Cost Management: Though broad consumer demand appears stable, the commentary on cost management and deliberate margin control across different categories reflects a vigilant stance on maintaining competitive positioning amidst potential economic fluctuations.

Overall, Costco conveyed a message of stable performance with areas of strength in discretionary spending and member engagement, while remaining attentive to broader economic conditions and consumer price sensitivity.

Brief Summary of Q2 2024 GM Earnings Call

Macroeconomic and Consumer Demand Assessment :

During the Q2 2024 earnings call, GM management expressed a mixed assessment of the macroeconomic environment and consumer demand. The overall sentiment was cautiously optimistic, bolstered by strong financial performance and strategic initiatives.

Strengths Highlighted :

1. Ongoing Strong ICE Business: The company cited the high-performing sales of ICE trucks and SUVs, and highlighted stable pricing and low incentives as favorable trends helping maintain strong margins and market share.

2. EV Growth and Scaling: GM’s EV portfolio showed considerable year-over-year growth, particularly in U.S. deliveries, with a market trend of 40% growth compared to the industry's 11%. The company expressed confidence in the continued adoption of EVs. Excitement around upcoming models like the Chevrolet Equinox EV was also noted.

3. Inventory and Production Discipline: GM maintained disciplined production aligned with market demand, enabling stable dealer inventory levels.

Areas of Concern :

1. China Market Weakness: GM outlined significant challenges in the Chinese market, where excess capacity and aggressive pricing strategies by competitors have severely impacted profitability. Despite expecting a return to profitability in Q2, GM reported a loss and acknowledged persistent headwinds.

2. Potential Pricing Headwinds: The company anticipated pricing challenges in the second half of the year, expecting a year-over-year pricing decline of 1% to 1.5%.

3. Production and Inventory Risks: There were concerns about maintaining alignment between EV production and consumer demand, with a cautious approach towards inventory buildup.

Investor Actions :

GM demonstrated effective capital allocation, including significant stock repurchases totaling $1 billion in Q2 and an ongoing $10 billion Accelerated Share Repurchase (ASR) program.

Future Outlook :

1. EV and ICE Flexibility: Looking ahead, GM aims to provide consumers with a broad choice between ICE and EV models, leveraging their production flexibility to meet a range of consumer demands and potential regulatory changes.

2. Upward Revised Guidance: GM raised its full-year guidance for EBIT adjusted, EPS diluted adjusted, and adjusted automotive free cash flow, showing confidence in the company's core operational performance and strategic initiatives despite market uncertainties.

Conclusion :

Overall, while GM showed strong performance and an optimistic outlook on most fronts, the company acknowledged ongoing weaknesses in the Chinese market and anticipated pricing pressures in the latter half of 2024. They are taking proactive steps to align production with market reality and ensure sustained profitability.

Brief Summary of Q2 2024 F Earnings Call

Overview of the Call

The Q2 2024 earnings call for Ford Motor Company featured key executives including Jim Farley, President and CEO, and John Lawler, Vice Chair and CFO. The conversation covered Ford's current performance, strategies, and future expectations, with a robust Q&A session highlighting pertinent investor concerns.

Opinions on Macro Environment and Consumer Demand

During the call, Ford expressed a cautiously optimistic outlook on the macro environment and consumer demand:

1. Balanced Supply and Demand: Ford CFO John Lawler mentioned that they see the supply and demand for vehicles in balance, indicating a stable macro environment.

2. SAAR Assumptions: The company’s planning assumptions for the U.S. include a flat to slightly higher SAAR (Seasonally Adjusted Annual Rate) in both the U.S. and Europe, hinting at a stable consumer demand outlook.

3. Government and Infrastructure Spending: Jim Farley highlighted significant ongoing investments in infrastructure and 5G upgrades, which support demand in segments like Ford Pro, further reinforcing a positive demand outlook.

Signs of Weakness in Demand

While the overall outlook was positive, several signs of potential weakness in demand were noted:

1. EV Pricing Pressures: Jim Farley mentioned pricing pressures in the EV market due to excess capacity, leading to more consolidation and necessity for partnerships. This suggests stress in maintaining competitive pricing for EVs.

2. Early Majority vs. Early Adopters: Farley noted a divergence in the adoption rates of electric vehicles between early adopters and the early majority, indicating potential challenges in accelerating EV uptake among mainstream consumers.

3. Commercial vs. Retail Demand: A divergence was also noted between commercial and retail demand for EVs, with commercial customers focusing more on total cost of ownership and retail customers displaying more skepticism.

4. Market Dynamics: Despite the overall balanced market outlook, there are emerging headwinds in warranty costs and inflationary pressures in Turkey, as flagged by John Lawler. Additionally, the company expects a lower industry pricing driven by higher incentive spending in the second half of the year, which could hint at potential demand softness.

Key Risks and Opportunities

Ford highlighted key risks and opportunities:

• Product Freshness: Ford emphasized their refreshed product lineup, especially in commercial vehicles, as a strong driver of demand despite market pressures.

• Software and Digital Services: The company is heavily investing in software and digital services, which are expected to drive substantial revenue and margin growth.

• Infrastructure-related Demand: Long-term government investments in infrastructure are expected to keep demand robust for specific vehicle segments.

In summary, Ford remains optimistic about its strategic direction amidst a challenging environment but is aware of the potential demand weaknesses, especially concerning EV adoption and market pricing pressures. The company's strategic investments in product innovation, software, and strategic partnerships are seen as vital levers to navigate these challenges.

Brief Summary of Q2 2024 PM Earnings Call

During the Q2 2024 earnings call, Philip Morris International (PM) expressed confidence in the macro environment, highlighting robust performance despite various challenges. They discussed strong growth across multiple categories, particularly smoke-free products such as IQOS and ZYN. The company noted a record first half (H1) in organic top-line and operating income (OI) growth, driven by solid demand in key markets like Japan and Europe, despite the impact of the EU characterizing flavor ban.

Opinion on Macro Environment and Consumer Demand

PM demonstrated an optimistic outlook on consumer demand, reflecting confidence in their strategic initiatives. The company referenced broad-based growth across different product categories and significant increases in shipment volumes and adjusted in-market sales volumes (IMS).

Signs of Weakness in Demand

While PMI reported overall strong performance, they acknowledged some signs of weakness linked to specific issues:

• EU Flavor Ban: The implementation of the flavor ban in Europe, particularly Italy, caused an impact on the growth dynamics of IQOS. The effect in Italy was slightly more pronounced than anticipated due to earlier sell-through of affected SKUs and concurrent pricing adjustments.

• Supply Tensions for ZYN: ZYN experienced supply chain constraints which affected volume growth. However, PMI expects these constraints to gradually improve through Q3 and be resolved by Q4, coinciding with expanded production capacity.

Overall, PMI's forward-looking statements indicate proactive measures to mitigate these challenges, with expectations of continued strong performance and further growth in the second half (H2) of 2024.

Brief Summary of Q2 2024 NFLX Earnings Call

Macroeconomic Environment and Consumer Demand

Netflix expressed optimism about its position in the macroeconomic environment, emphasizing healthy revenue growth, member growth, and profit growth across all regions. CFO Spence Neumann highlighted that the company saw 17% reported revenue growth and a margin increase of 5 percentage points year-over-year. The company demonstrated confidence in sustaining healthy revenue growth and margin expansion despite external economic factors.

Consumer Demand

Netflix reported strong demand driven by several factors:

1. Content Slate: A wide variety of popular titles across genres and regions significantly contributed to member growth.

2. Paid Sharing: Continued positive impact from the paid sharing initiative, which helps convert previously unpaid accounts.

3. Ads Plan: The attractiveness and entry price point of its advertisement-supported membership tier add to member growth.

Signs of Weakness in Demand

The company mentioned anticipated headwinds in engagement due to the paid sharing measures, i.e., transitioning users from unpaid to paid status, which was expected to impact engagement levels initially. However, it was noted that engagement levels among members unaffected by paid sharing remained steady and even improved year-on-year, showing resilience in consumer demand.

While the advertising business is scaling and growing, it’s not yet a primary revenue driver, indicating that it is still in its early growth stages. However, Netflix projects that advertising will become a more significant contributor in the coming years.

Conclusion

Overall, Netflix displayed confidence in its strong performance metrics and growth strategies, with no significant signs of weakness in demand. The company highlighted a steady and optimistic outlook in light of the competitive landscape and macroeconomic conditions.

Brief Summary of Q3 2024 DIS Earnings Call

Analysis of the Macro Environment and Consumer Demand

During The Walt Disney Company’s Q3 2024 earnings call, the company expressed a cautiously optimistic view regarding the macro environment and consumer demand. While there was some indication of demand moderation, particularly within their theme parks, Disney executives did not present it as a significant concern, nor did they consider it a protracted issue.

Signs of Weakness in Consumer Demand

The company did acknowledge a "slight moderation in demand" within the theme parks segment, which was attributed to a mix of factors:

1. Lower Income Consumers Feeling Stress: There was a mention that lower-income consumers are experiencing some financial stress, which could potentially affect their spending on discretionary items like theme parks and vacations.

2. High-Income Consumer Travel Trends: High-income consumers appear to be traveling internationally more frequently, possibly affecting domestic park attendance.

Additional Insights

• The openness about expected flattish revenue for Q4 indicates Disney is cautiously managing expectations for short-term growth within their parks and experiences segment, including incorporating some anticipated costs for new cruise ships.

• Despite these signs of demand moderation, Disney executives emphasized strong underlying business fundamentals, including solid attendance figures and slight per capita spending increases within the parks segment.

• Forward-looking, the company remains bullish on its diversified portfolio, including streaming services, live sports broadcasting rights, and upcoming movie releases, which they believe will drive future growth and consumer engagement.

Brief Summary of Q2 2024 PEP Earnings Call

Macro Environment and Consumer Demand :

PepsiCo management, primarily CEO Ramon Laguarta, acknowledged a challenging macroeconomic environment, especially citing a softer U.S. consumer landscape affecting low single-digit growth in recent quarters. The company expressed a mixed sentiment regarding consumer demand. While certain segments, such as Quaker and international markets, are performing well or expected to improve, parts of the U.S. portfolio, particularly Frito-Lay North America, are facing challenges.

Signs of Weakness in Demand :

• U.S. Consumer Challenges: PepsiCo noted that U.S. consumers are increasingly price-conscious, seeking more value across several products. This behavior is not limited to low-income households but extends to middle and higher-income groups, indicating a broader trend of cautious spending.

• Frito-Lay North America: Soft volume results were highlighted for this segment, with a specific mention that some value adjustments might be needed for certain products, especially basic items like unsalted potato chips and tortilla chips.

• Salty Snack Category: Observations suggest that the entire snack category is under pressure, potentially becoming more discretionary for consumers. Promotional efforts have not yielded significant responsiveness, underscoring the value-centric demands of consumers.

Mitigation Strategies and Positive Indicators :

• Reinvestment: PepsiCo plans to reinvest the savings from productivity and cost reduction efforts back into the business to spur growth in the second half of the year.

• Specific Products and Markets: Success in certain areas such as the Gatorade brand gaining share, positive growth for zero-calorie beverages, and improved supply chain issues for Quaker products were cited as positive indicators.

• International Growth: The company remains bullish on international markets, particularly in regions like Latin America, Europe, and Asia, with ongoing investments in infrastructure and brand development.

Overall, while there are clear signs of weakness in demand and heightened sensitivity to price among consumers, PepsiCo also identified multiple areas of resilience and growth, providing a balanced outlook for the remainder of 2024.

Brief Summary of Q2 2024 KO Earnings Call

Company’s Opinion on the Macro Environment

During the Q2 2024 earnings call, James Quincey, CEO of Coca-Cola, shared the company's perspective on the macro environment. He noted that the operating environment is characterized by a wide spectrum of dynamics, but Coca-Cola’s "all-weather strategy" is yielding success. Despite the diverse challenges and market conditions globally, the company sees the beverage industry as attractive and expanding, providing substantial opportunities for growth.

Consumer Demand

Quincey touched on consumer demand across various regions. In general, they reported strong performance and maintained optimism about achieving global objectives. However, there were specific comments indicating nuanced consumer behaviors in different regions:

• North America: Despite overall resilience in consumer sentiment, there were signs of weakness in away-from-home channels, such as lower traffic and budget-conscious behavior like seeking out combo meals.

• EMEA: The external environment in Western Europe showed mixed results, with some pressure from reduced foot traffic and adverse weather affecting the away-from-home business. Meanwhile, geopolitical tensions and economic uncertainties impacted business in Eurasia and the Middle East.

• Asia Pacific: In China, consumer confidence remains subdued, although the company emphasized a focus on core business and long-term profitable growth investment.

• Africa: There were multiple currency devaluations and intense inflationary environments in regions like Nigeria, where accessible price points and refillable packaging were used to win market share.

Further details from John Murphy, CFO, corroborated this mixed consumer demand landscape and included financial insights that reflect the resilience and adaptations Coca-Cola is implementing to navigate through the various challenges and opportunities in different markets.

Signs of Weakness in Demand

Yes, there were several mentions of signs of weakness in demand:

• North America: Volume decline driven by softness in away-from-home channels, with some indications of lower traffic and increased value-seeking behavior among lower-income consumers.

• EMEA: In Western Europe, the away-from-home business faced pressure due to reduced foot traffic and adverse weather conditions.

• China: The region showed subdued consumer confidence.

Despite these challenges, Coca-Cola continues to find ways to adapt, innovate, and drive growth in these markets through strategic investments, digital innovation, and focused marketing and pricing strategies.