In the previous review we analyzed similarity of market behavior at the peak of the dot-com crisis and current conditions. This analysis is an update of this view and an attempt to determinate optimal assets for investment.

Executive summary:

- Despite the optimism that dominates the market, the similarity of the 2000 and 2021 patterns is rather confirmed.

- The main difference in 2021 is the risk of interest rate growth. In 2000, rates were relatively high, so the bond market had a good headroom. The situation in 2021 is worse in the sense that the main risk now is an increase in rates, and, therefore, a fall in bond prices. Thus, the investment opportunities now are a bit narrower.

- As a first approximation, the stock market consists of stocks of fast-growing companies with low current profitability, but high potential and stable companies providing 4-5% annual return (meaning net profit margin). Under the prevailing conditions, the first category of companies (growing companies) is riskier. The greatest risk is posed by companies that have not reached the breakeven level. One should also be wary of giants-monopolists, whose growth potential may be overestimated by the market now.

- The portfolio should be structured in such a way so that in the event of negative trends, it would be possible to increase the share of equities in the portfolio$

- The role of bonds in this scenario is to preserve funds.

Inflation has been a main concern this year. In the long term, stocks provide excellent protection against inflation. The rise in prices brings with it an increase in corporate profits (even after considering the increased wage costs). This is followed by a rise in share prices.

However, in practice, everything is a bit more complicated. Rising inflation may lead to an increase in rates by central banks, and this pushes the stock market down.

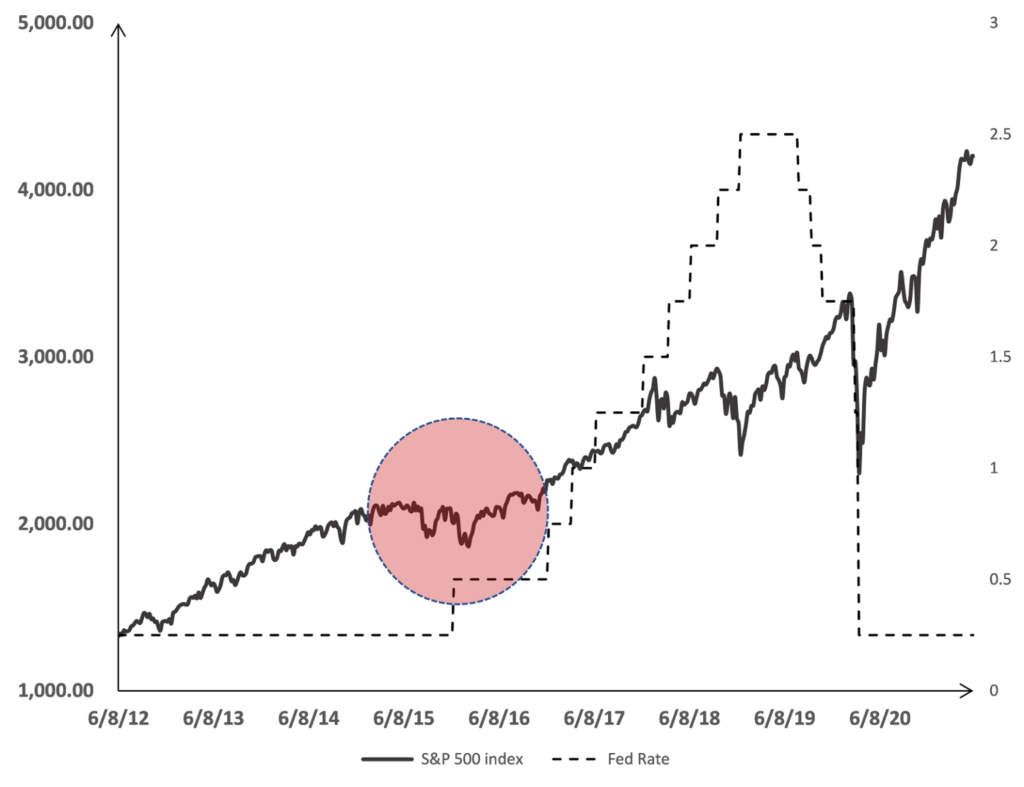

A good illustration is 2015, when the market for several months in a row constantly expected the increase in interest rates (which has been happening since 2016) (Fig. 1)

It is important to make two points related to the current conditions.

First, it doesn’t matter at all whether we will be overwhelmed by inflation or not. There are different points of view in this regard. This question is very complex and confusing, and its analysis is not the mail purpose of this review. More important is that any idea most often goes through several stages of faith in it by market participants: from complete disbelief and disregard (recall the stability of the market in January-February 2020, when the coronavirus epidemic was already raging in China) to panic and exaggeration of problems. Based on this, it follows that a wave of market drops on the expectation of inflation alone is quite likely.

Secondly, the growth of interest rates does not change the investment case and does not affect the real side of the business in any way, at least for companies with a low level of indebtedness. Nevertheless, the impact of growth in rates on the stock market is negative and everyone knows it. Regardless of the direct effect of the growth in interest rates on enterprises, stocks may sink due to a wave of selling on the fear of growth of interest rates alone. The “high price” of stocks is a more important factor here. The overheated market may fall even on minor news. An increase in interest rates or inflation can only bit a trigger, which can lead to a slide of equity prices to “normal” levels.

A previous review on this topic “dot.com # 2” was devoted to analysis of overheating markets and the success of investments at the beginning of 2000.

Summary of this analysis:

- The riskiest 3 types of investments were:

- Developing companies that did not break even by the time the crisis began. For most companies in the IT sector, access to the financial market was closed, and companies began to “burn” their liquidity. The term “cash burn” became the main for assessing the quality of an IT project for some time[1].

- Developing companies with positive cash flow, but with extremely high valuation by the market due to the high rate of business growth.

- The vast majority of IT giants, with the exception of Microsoft. These companies, due to their popularity and scale, were the targets of investors, which led to a reassessment of the growth rates of these companies.

Other sectors not affected by IT fever have proven to be safer investments.

The hallmark of the current market conditions is that the inflation risk has already been partially taken into account in prices, but mostly with a “plus” sign. The following assets have already risen on expectations of inflation:

- Commodity markets

- Equities connected with commodities: oil companies, metal and fertilizer producers, etc.

- The banking sector, whose profit links with the growth of interest rates

We can also mention auto manufacturers, whose capitalization increased on the expectations of their transition to the EVs. “Tesla” set a new height for the entire market: Market Cap/Sales ratio in January 2020 grew to 25, with a normal level of 0.4-0.6 for the car market majors.

In these conditions, “safe heaven” might be, oddly enough, companies that have not been on a spotlight for a long time: retailers and companies from any sectors that do not have any particular drivers. Examples of such companies are CISCO, Verizon, AT&T, Unilever, Danone.

Facebook, which profits will provide about 5% annual return on investment in 2022 stands apart. The vast majority of other majors like Microsoft or Apple will reach this level in about five years with more or less reasonable forecasts of sales development.

And, finally, another interesting segment is the most profitable companies in the sectors which were hit hard by the coronavirus. A striking example of such a company is Ryan Air, which has one of the highest margins in the industry. Such companies can act as a center of consolidation for less fortunate competitors and provide good long-term growth.

What has changed in the market over the past three months

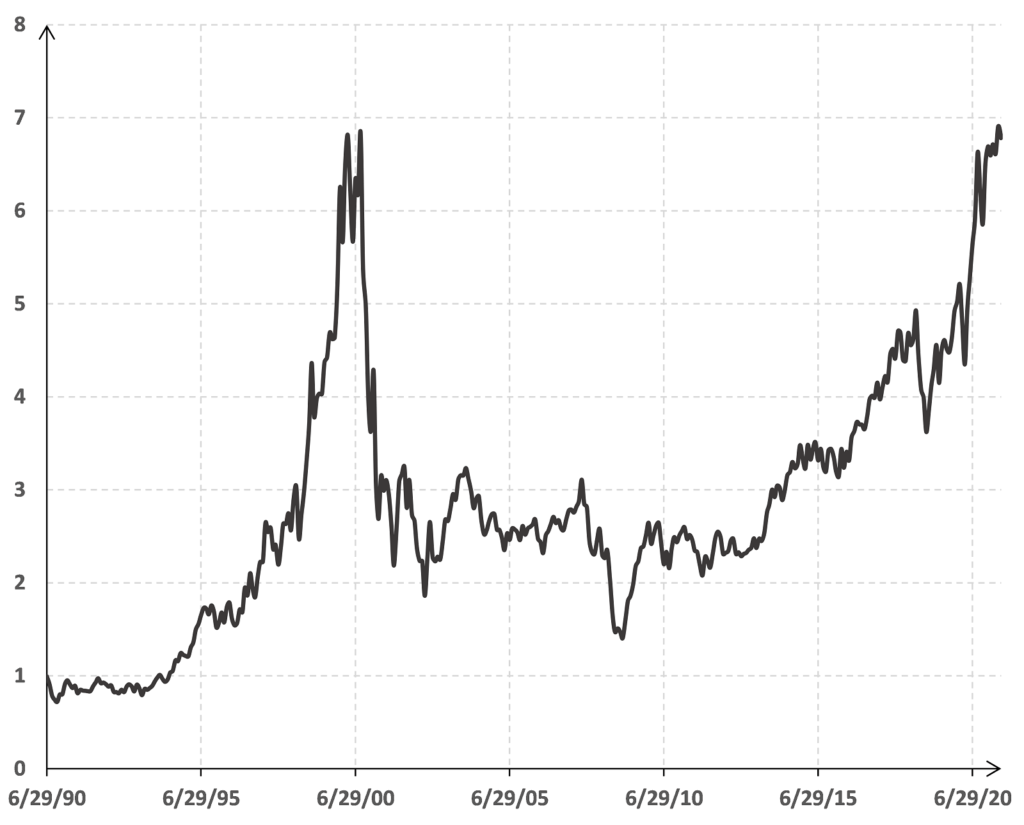

The overall level of “high price valuation” companies of IT – the sector holds the level reached in August 2020, but the dynamics is lost (Figure 2.).

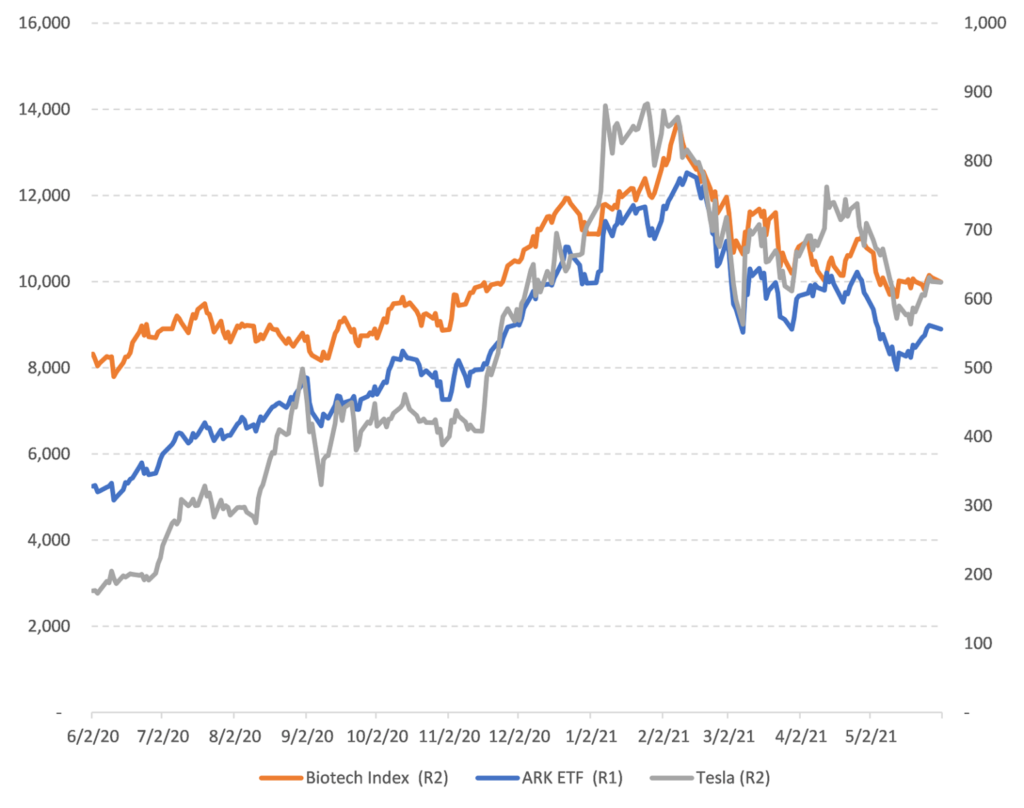

We can see a more interesting picture in the sub-sectors that have been the most popular with investors over the past six months.

In Fig. 3. The graphs are shown:

- Tesla shares. The soar of its stock price in 2020 was one of the most impressive developments of the past year. Its capitalization reached 750 billion USD , approaching the total capitalization of the entire global automotive industry with a global market share of 0.5%[2];

- US Biotechnology Sector Index. In 2020, it doubled on the growth of the segment’s popularity amid the coronavirus;

- ETF of innovative companies from management company ARC – This ETF has almost quadrupled in 2020.

All these investments have 1 similar characteristic: these companies are showing very modest current results at best. Their popularity is based on their very long-term prospects.

The current market situation qualitatively reminds us of the pattern observed in 2000 when investors began to think “for decades ahead” as well. Fig. 3 suggests that in order to understand the dynamics of the shares of all “growth” companies, it is much more important to understand general investor perception, rather than the specifics of each individual company

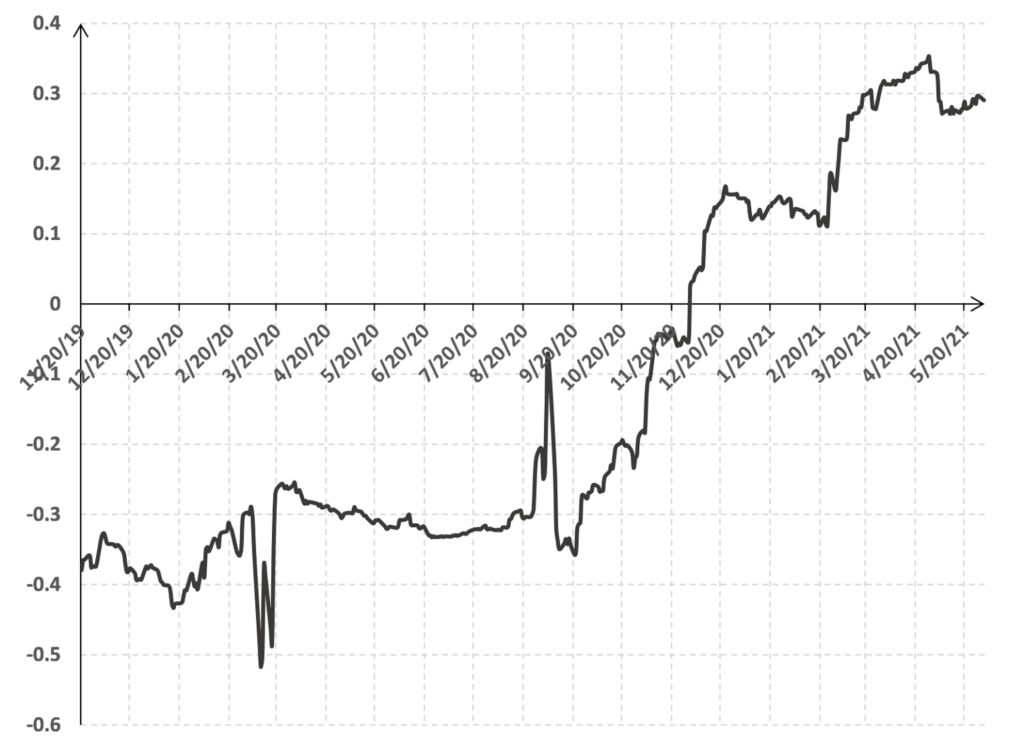

The correction in the “growth” market segment is closely related to expectations of an increase in interest rates as it is shown in Fig. 4. The textbook relationship between bond and equity markets is negative correlation – when stock markets fall, bonds rise, and vice versa. Starting from the end of last year, in the case of the “growth” segment, stocks began to show positive correlation with bonds. Moreover, happened on the background of the correction of the bond market. Thus, the fear of inflation and rate hikes begin to weigh on both markets: bonds and stocks.

However, as already mentioned, the impact of interest rates on the stock market is rather psychological in nature [3]. The real reason for the price slide is the boom in investment from unqualified, retail market participants. Modern electronic brokerage platforms opened up amazing opportunities for them to trade from smartphones in a matter of seconds, from anywhere in the world using Internet.

This led to the overvaluation of many securities and entire sectors. By now, the excitement has subsided, and the market has begun to cool down.

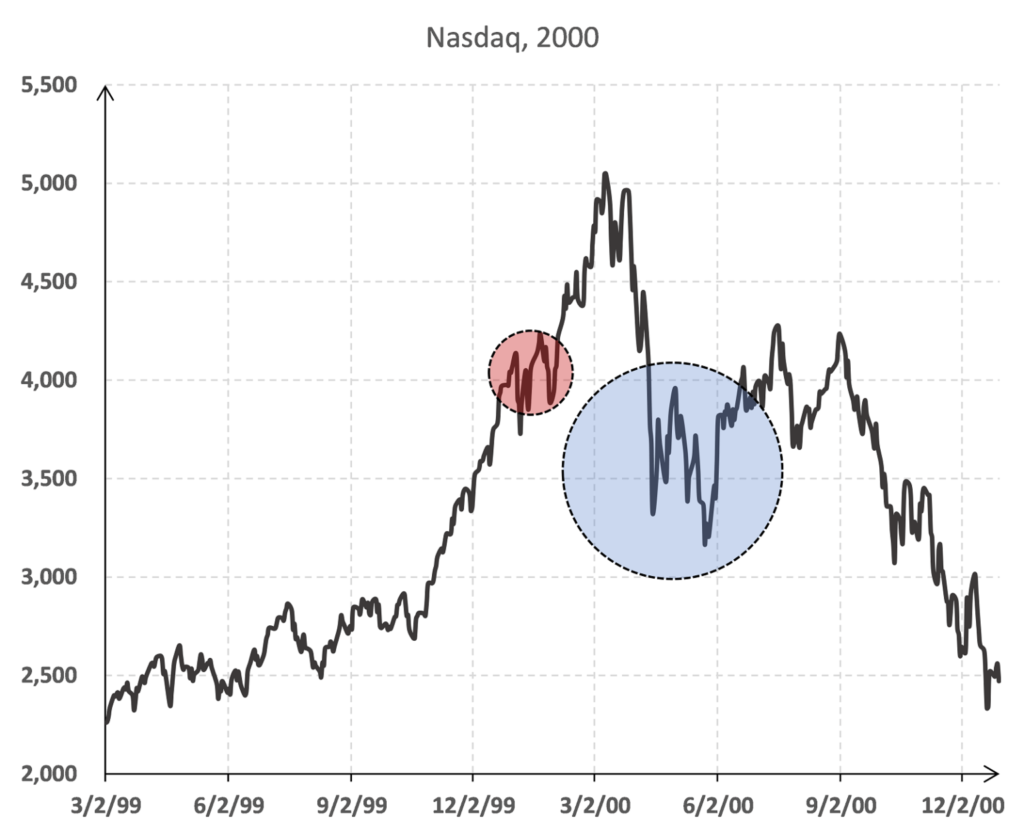

Fig. 5 shows the qualitative similarity in the behavior of the NASDAQ index in 2000 during the dot.com crisis and the behavior of innovative companies now. It is worth to note the following:

- The NASDAQ in 2000 was much more innovative than it is now. Now shares included in NASDAQ have grown to the level of global players and outperform classical companies in terms of capitalization such companies like industrial and energy.

- Market growth in both cases began after the crises: after the default and a series of devaluations in emerging markets in 1997-1999 and after the coronavirus epidemic in 2020.

- In both cases, investors turned their attention to the “hype” sectors of the economy. The growth rate of shares in these sectors noticeably accelerated. In both cases, the growth wave was split into two “sub-waves” with market consolidation in the middle of the growth (these areas are marked with red circles).

If we continue this analogy further, then speculative growth is possible for now, but further behavior of stocks may be depressive in the long-term. As in 2000, there is a danger that eventually the negative will spread to other sectors, only with a lag in time.

The behavior of cryptocurrencies should not be ignored either. There is no fundamental link between the behavior of cryptocurrencies and the stock market, but the crypto market is a good litmus test of investor risk appetite. Since non-professional, retail investors are now in some sense the dominant class in the stock market, the behavior of cryptoassets, especially Bitcoin, shows the nature of stock market fluctuations.

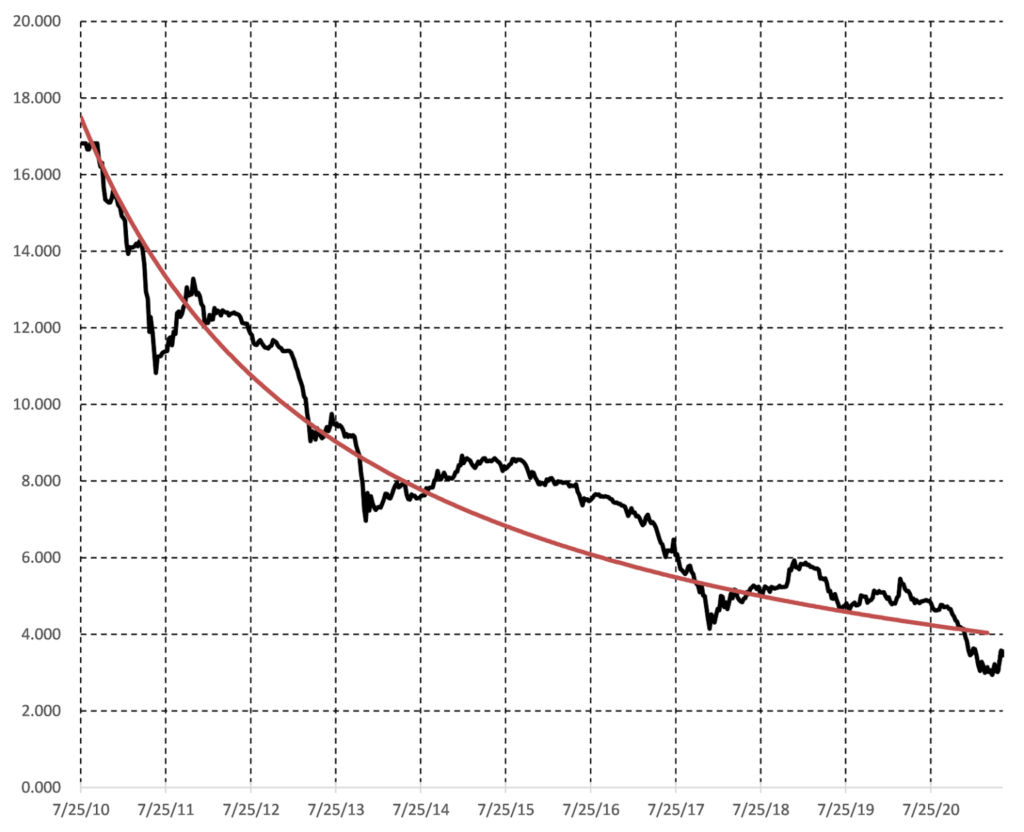

In Fig. 6 we show a Bitcoin model developed by the company. The red line is a simple hyperbole. According to some reasons it is a good interpolation of the long-term behavior of Bitcoin. Without going into the mathematical details of this simple model, we came to several conclusions:

- Bitcoin is in downward correction approximately every three to four years. From the point of view of this cycle, now is a good time for correction.

- In all cases, the Bitcoin correction that occurs at the bottom of the red line Is long-term (the chart is inverted!) and drives the price upward for a comparable amount above the red trend line.

- Based on typical Bitcoin fluctuations, its low point could be in the range of 10’000-12’000 USD.

In 2011 and 2017, the bitcoin correction led to a correction in the stock market with a lag of 1-3 months. In 2013, there was no correction in the stock market.

Gold

______________________________

In the backdrop of a deficit of investment instruments, gold may represent some interest. As a rule, gold is not part of our investment portfolios for various reasons[4]. However, since the risk of interest rates hikes removes both stocks and bonds from the list of rising market assets, gold can serve as a safe-haven investors with free resources. Gold is a pro-inflationary asset and the risk of a spike in inflation is positive for the gold market.

Potentially, gold can account for up to 10% of the total portfolio.

As of early June, gold is locally overvalued. A wave of short-term optimism may now be seen in the stock and cryptocurrency markets. On this wave, gold may return to the 1’800 level . Technically, this can be a good time to enter the market. Moreover, in terms of cyclicality, this moment may correspond to the end of the wave of optimism in the stock market.

Bond market

The potential of the bond market is shown in Fig. 8. It depicts a long-term ETF chart for emerging market bonds. All coupons and redemptions of bonds included in the structure of this fund are paid to the investor in the form of dividends. The dividend flow is fairly stable at about 35 cents per fund share per month, or about 3.85% per annum in US dollars at current prices.

A market correction will put pressure on bonds as well. Potential for possible drawdown – up to 6.5% of the current levels. However, corrections on the bond market are very short term, as a rule. Therefore, in any case, bonds of developing countries are more likely to preserve capital, and in the long term, they provide a relatively stable cash flow. Investing in such an ETF is a quasi-deposit. However, this is a diversified investment (there are several hundred positions in the fund), the reliability of which is higher than the reliability of many large banks.

In the case when the bond market becomes more strategically interesting, you can invest in individual bonds. The main objects of investment are government and quasi-government bonds of developing countries (Russia, Brazil, Mexico, South Africa, Indonesia, Eastern Europe)

Current market conditions, with excess liquidity and risks of rising interest rate force asset managers to invest into high yield and short duration instruments. So, in order to incorporate some short duration exposure with high income we can add U.S. High Yield Corporate Bond ETFs (PIMCO US Short-Term High Yield Corporate Bond ETF – STHY) as an example. This fund provides high yield of about 4.05% to maturity, low duration of 1.64 year – this will limit price volatility in case of rising interest rates and provide high current yield. As current financial conditions remain super loose – level of corporate default is very low – noninvestment grade companies have access to capital markets to refinance their obligation, extend maturities and thus improve credit profile.

Another option that can provide similar characteristics – Senior Loans. It is also high yielding asset class (example: Invesco Senior Loan ETF – BKLN). Senior loans are covered loans to corporations and their interest is linked to money market rates (Libor), so in rising interest rate environment they provide high current yield (3.5% YTM) and inflation hedge.

Summary

There are many reasons to believe that the current state of the market is “cooling” after the overheating like the late 2000 – early 2021.

Investors see the surge in inflation and the subsequent cycle interest rate rise as the main market risk. Stock market is the only tool that can strategically protect an investor from inflationary risks. In addition, the probability of a negative scenario is not 100%. Therefore, some allocation to equity markets is essential. When structuring a portfolio, the main attention is paid to securities without signs of overheating (“stable” companies) and growing companies whose stocks have corrected already.

Bonds serve as a “deposit” part of a portfolio to preserve funds or receive some income (about 4% per annum). The basic instrument for investing in bonds is the iShares EM Fixed income ETF by the largest asset management company Black Rock which consists of with sovereign (government) quasi-sovereign bonds emerging markets.