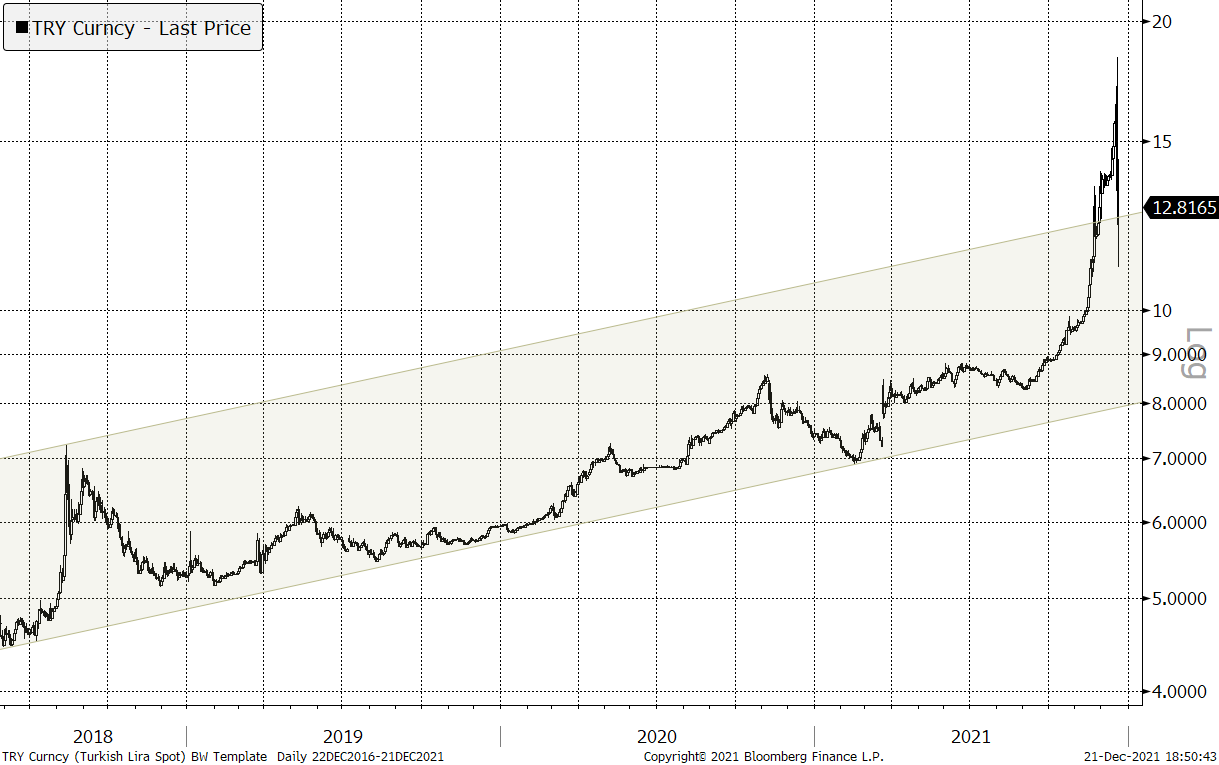

Chart I. Turkish Lira

Turkish Lira rebounded on Tuesday on the Erdogan’s rescue plan. The key point of the plan is that the Turkish Government will compensate losses of private deposits caused by Lira devaluation. Lira plunged on its support level (Chart I).

Bonds also rebounded, their move is much more modest, though (Chart II).

These two charts displays the difference between the attitudes of professionals and non-professionals towards the same situation. The devaluation of Lira was caused by panic of individuals trying to save their deposits in local currency. After they got the free put-option from the government they turned opposite fixing high Lira deposit rate without the devaluation risk.

The key question, however, is at whose expense this put option is expected to be. Turkey’s budget is well balanced, it is negative, though, with 1.5% of GDP deficit. FX reserves have been under disputes in the past years — the Central Bank’s balance sheet is not transparent. Turkey has never been a country with solid Central Bank’s FX position.

Actually, the only way Turkey can compensate FX losses is printing money. Emission can hardly be a good tool of fighting inflation and devaluation. What economic agents are motivated to do in a case of negative real rates is borrowing cheap money and placing it on a local currency deposit, getting high interest align with the “free” hedge against possible devaluation.

Another point we would like to highlight is that Lira has not entered into high volatility mode like it was in 2018. Generally last day or two of currencies devaluation comes along with incredibly high swings. Turning before such an extremum point is reached can be a sign of a temporary recovery. Now Lira is trading around 12.75. This is a top range of the trend channel (Chart I). After Lira broke this level this level became a support for the cross rate.

So, the upside is not justified both from fundamental and technical perspectives. Turkey remains to be a toxic investment, the rebound on the rescue plan can be a good point to reduce the Turkish risk.