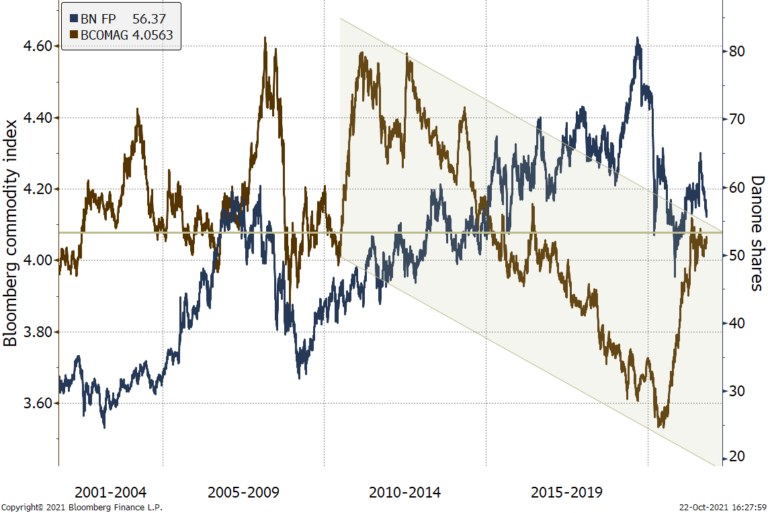

Largest European food producers (Danone, Nestle, Unilever) have been under cost inflation pressure for month. The chart above displays Danone stocks. It is easy to notice that sustainable uptrend is only possible when commodities are going down. Unlike the broad market, Danone and Unilever shares are still significantly lower than before coronavirus outbreak. The same pattern can be seen in 2003, 2011 and 2006.

Chart I. Bloomberg agriculture commodities index & Danone shares

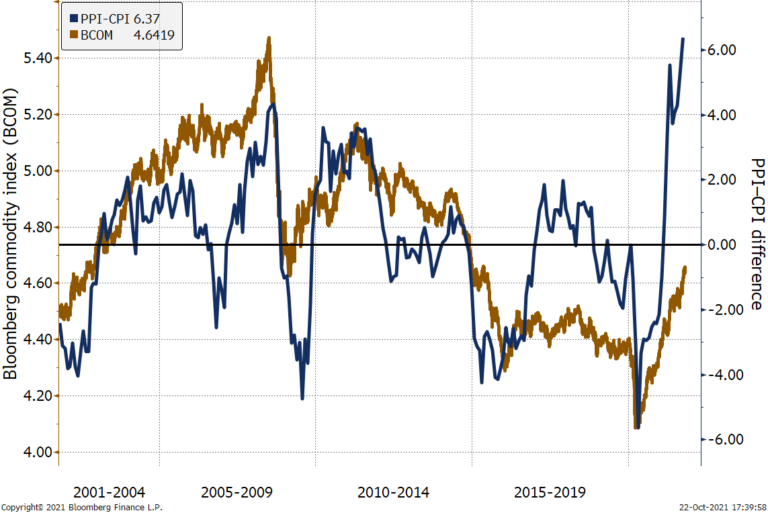

Chart II. PPI-CPI difference & Bloomberg commodity index

The fundamental explanation is that it is not always that producers can transfer production costs to consumers. This is exactly what has been discussed by analysts over the recent months.

Commodity cycles, in turn, are closely related to inflation cycles. The Chart above reveals the difference between Producers Price Index and Consumers Price index. High producers’ prices push commodities up. If PPI is growing faster than CPI, food producers are under pressure not being able to pass higher costs over.

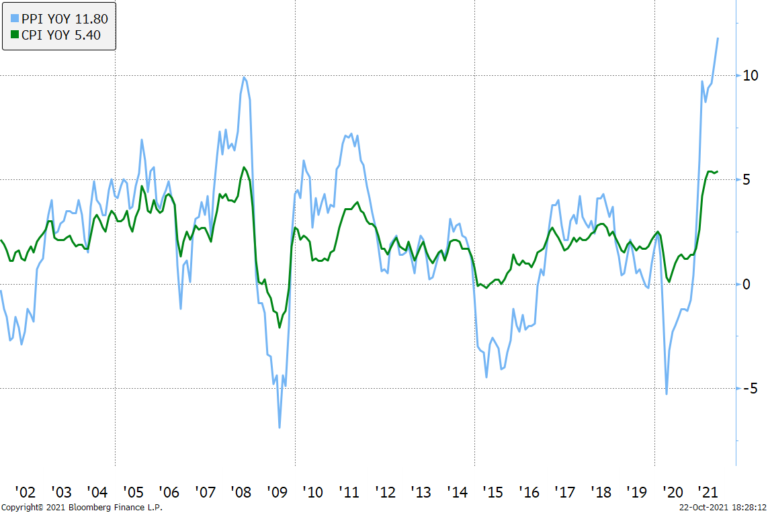

The Chart III compares CPI & PPI. These two inflation measures correlate with PPI being more volatile. When the inflation cycle turns down (which is a matter of time, we believe) PPI falls faster, putting pressure on commodities. During this cycle food producers start benefiting from high selling prices and lowering costs.

Interestingly, the agriculture commodity sub-index (Chart I) is just below its upper bound of the trend channel. This is not sufficient to go short, but an excuse to think seriously about staying long.

Both Danone and Unilever are near their historical support levels. The equity market often starts pricing things in advance. It is quite probable that in several months the companies’ representatives will be talking about managing the cost price inflation and lower commodity prices expectations. Even if Q4 2021 & Q1 2022 are not so good, investors will look at the future. So, the perception of this sector can be much better.

Chart III. US PPI &-CPI

Technical picture in commodities shows that the change of the paradigm can happen quite soon. Even if it is not the case, we should bear in mind that the fundamental reason for rallying commodities is the huge money injection. The bottlenecks in transportation is a temporary factor. This leads us to a conclusion that CPI will soon catch up with PPI and, as we can observe on the Chart III, it will outpace PPI.

Another point is that the equity market in whole is quite expensive. The risk of correction is high. We highlighted this in our review dedicated to comparison between the equity market conditions as of 2000 and now. Even if this time is different at some point investors can start take this risk seriously. Bond market and gold are poor save havens now. Consumers and utilities are classically defensive assets. Having fundamental value and being not expensive, stocks of such companies are generally less volatile. This can make investors pay attention to these sectors. Defensive stocks have been correcting over the past months. Food retailers experienced not only bad perception towards defensive sectors but cost inflation story on top of that. Due to that the food retailers are the most undervalued stocks for the time being. One can hardly find anything cheap nowadays. It might be a very good point for increasing the share of food producers in equity portfolios.