Q3 financial reporting released by Verizon on the 24th of October mirrored a typical picture for large telecommunication companies: their revenues and profits are stable and well predictable. Verizon’s EPS came in 3% higher than expectations, AT&T beat expectations both in sales and profits.

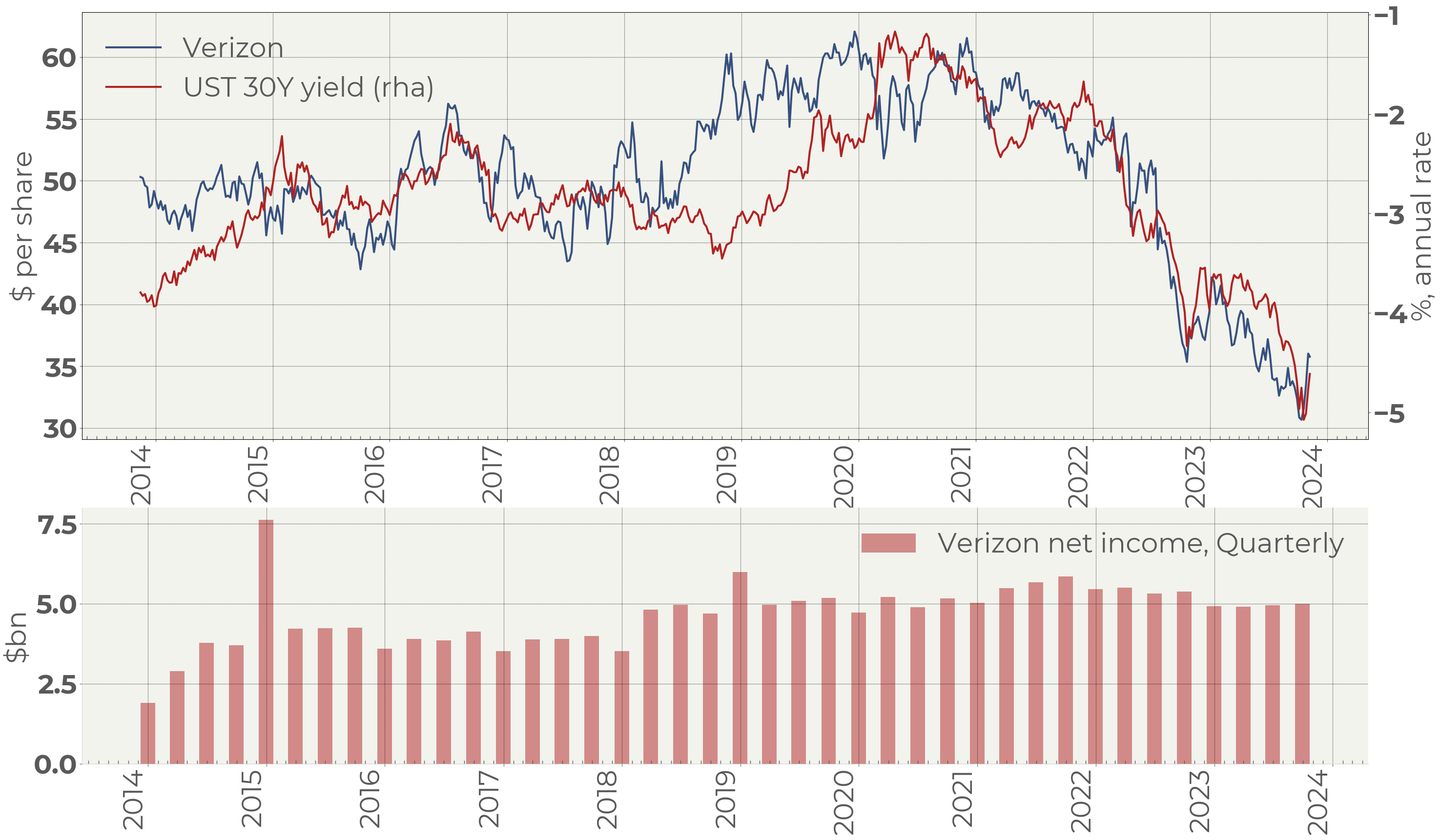

Nevertheless, Verizon’s stocks have been in depression over the past three years (Figure 1):

Figure 1. Verizon stock price, quarterly profit & 30Y US government bonds’ yield

The comparison of Verizon stock price to the long US government bond yield (inverted scale) leads to a conclusion that the main driver for such stocks is rates. Indeed, large companies of the Consumer Staple, Utility and Telecommunication sectors can be treated as quasi-bond investments. When the government bond yield reaches the level of IRR of companies, the question emerges why investors should take the equity risk while they can get the same return with much less risk.

No doubt, we can’t consider Telcos defensive. Raising rates not only changes the perspective of valuation but also negatively affects demand and hits profits though the liability side of the balance sheets.

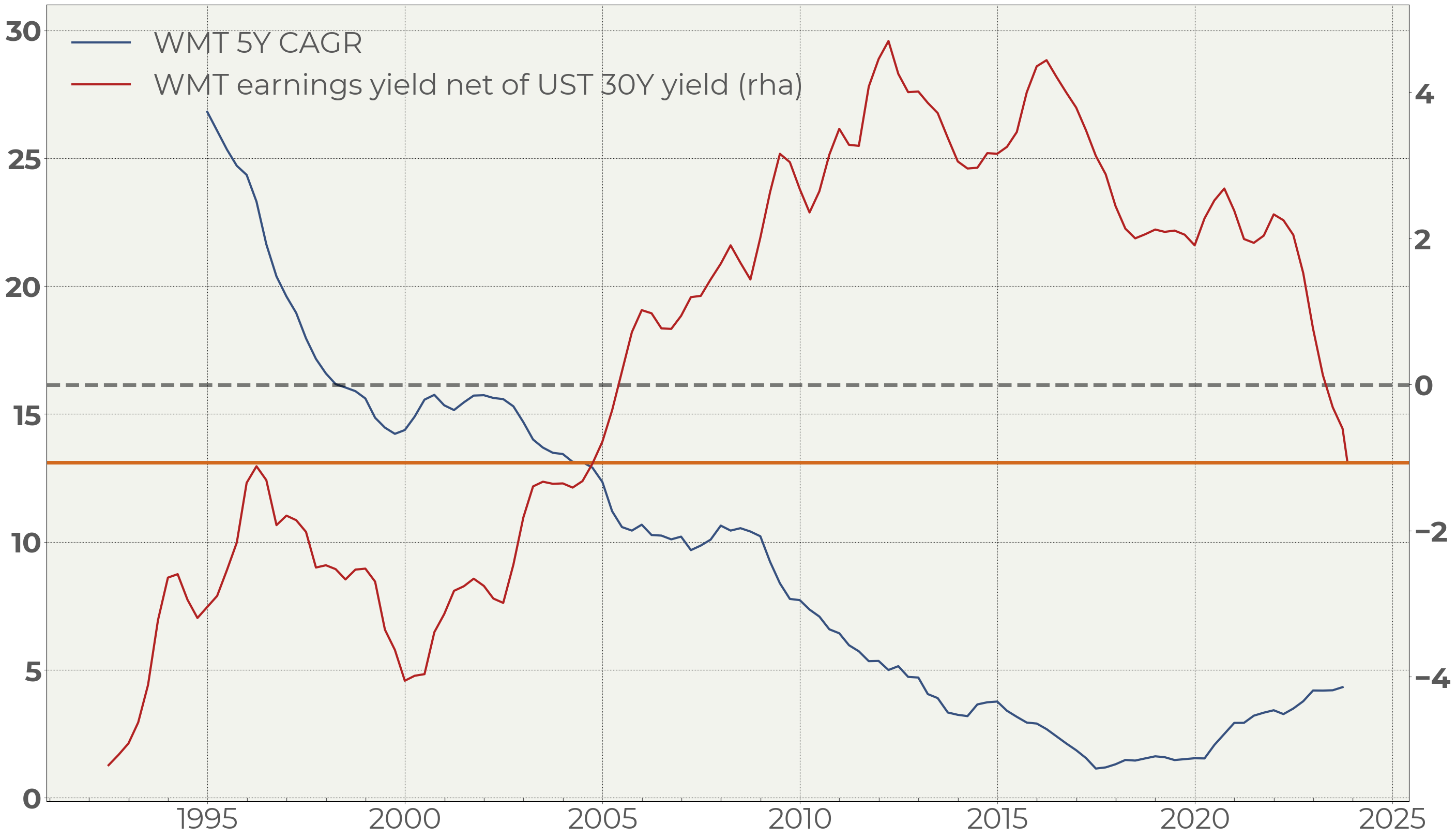

Walmart is an example of a defensive company that does not suffer from high rates directly. In contrast to Telcos its stock is near the top with a P/E ratio of around 30.

Walmart is a very good company but how interesting is it with a return lower than the government bonds’ yield?

Figure 2. Walmart earnings yield (net income-to-market capitalization ratio) net of US 30Y government bonds yield vs Walmart 5Y CAGR (revenue growth)

As Figure 2 shows, the return on investment in Walmart equity has reached the level typical of before 2005 period. Back then, however, Walmart used to be a fast-growing company with the CAGR circa 15% YoY.

The behavior of Walmart and Verizon highlights the difference between investors’ perception of more and less defensive stocks. Less defensive sectors such as Telcos are fully subject to the rates growth. At the same time the most defensive sectors such as consumer staples completely ignore that.

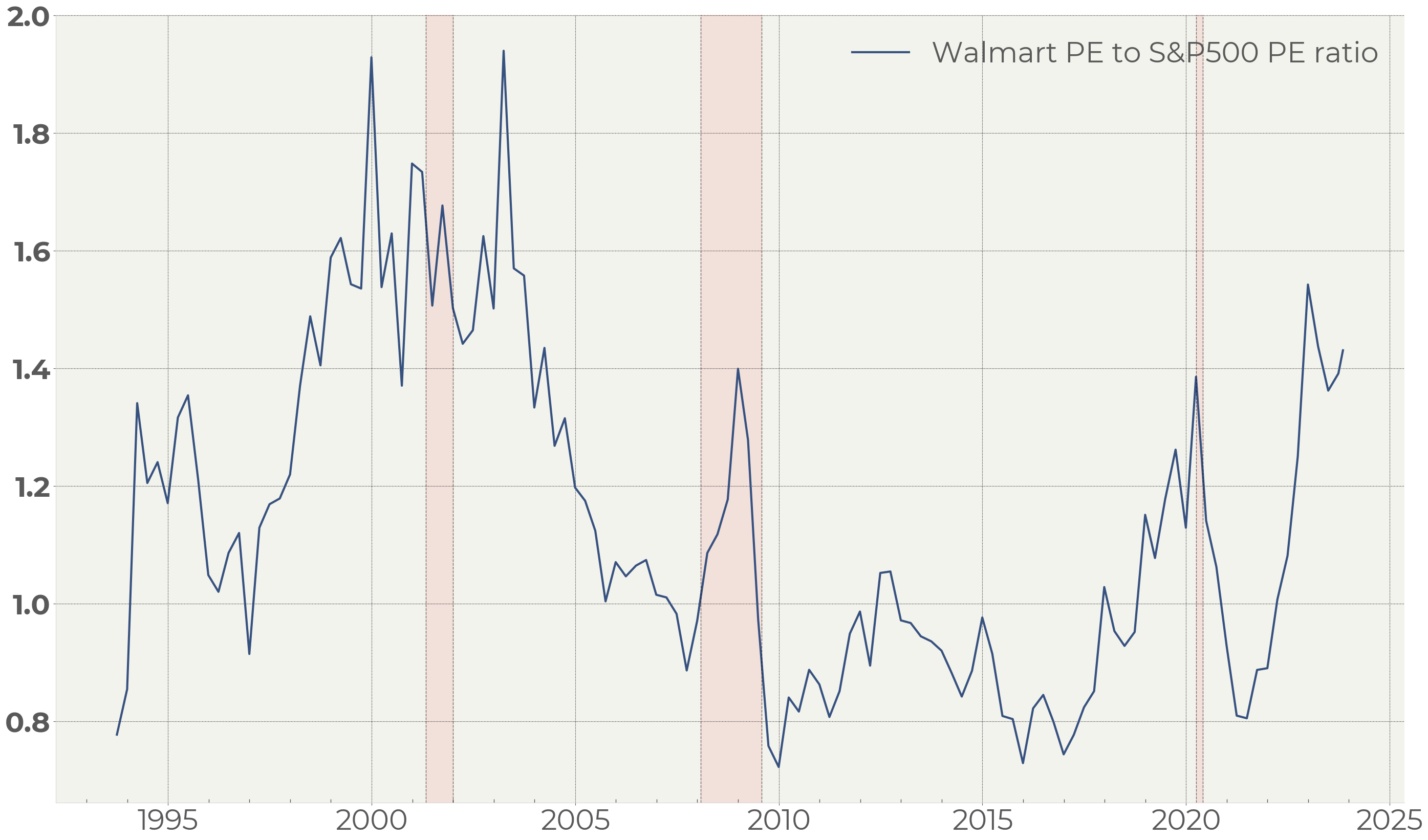

Another way to measure the expensiveness of Walmart is comparing its P/E ratio to one of S&P 500 index:

Figure 3. Walmart PE-to-S&P500 PE ratio

Periods when Walmart was overvalued compared to the broader market reflect the investors’ intention to be defensive. These periods, as Figure 3 shows, correspond to recessions.

Looking at Walmart shares from this perspective not only do we see that its shares are overvalued but we can also use its valuation (in a broader sense – valuation of consumer staples) as one of the recession indicators.