The investors’ reaction on a new “Omicron” strain’s looks controversial.

Traditionally defensive stocks such as Consumer Staples or Utilities are amongst worst losers, while traditionally volatile IT stocks are surprisingly resilient.

This can be explained by what had happened to those shares before “Omicron”. COVID-19 happened to be a price booster for IT stocks: remote working process, teleconferencing triggered IT companies’ profits surge. On the other hand, inflationary expectations and supply chain disruptions caused negative pressure on food retailers’ and producers’ margins. The lesson was learned: in the 2H 2021 investors preferred IT over consumers. Higher business growth rate, better stocks dynamics and improved fundamentals made IT names remarkably popular with investors. The flip side is stocks’ valuations. For the time being, once any growth rate higher than 10% can be detected, investors are ready to pay a lot, pricing in the next five- or even more year growth.

According to common logic overvalued stocks are more sensible to negative sentiment. Omicron is a definite negative factor. The trick of current situation is that investors already know that the virus affects negatively classically defensive stocks and positively IT and other growth stocks. This sent “defensive” stocks significantly lower, making them losers.

Such investors’ reaction is fundamentally controversial. Interestingly, the reason of pressure on consumers and other defensives is high commodity prices. Commodity market has fallen on “Omicron”, though. Selling value can be justified if we assume that high commodity prices are for long with food and other producers not being able to compensate that on customers’ expense. Betting on high commodities contradicts with slumping commodity market. As to passing the cost inflation on customers, we consider it is a matter of time (we have already discussed the matter in our short notice on Food Producers).

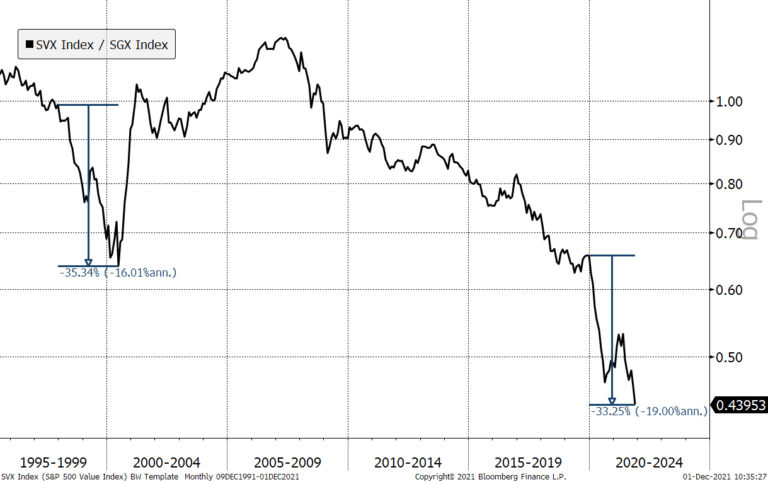

Chart 1. Value-to-Growth S&P 500 sub-indexes ratio.

Chart 1 shows the Value-to-Growth ratio. Falling Value is a sign of bull market. In other words, if investors prefer to take high risk and buy expensive stocks in case of negative events, the bull market persists. That leads to a controversial conclusion: pandemic fear is a supporting factor for bull market mood. This means that the local recovery in growth names is highly possible. However, it might be short-lived. Growth can turn down just because of high valuations, with no fundamental driver. If a real market correction can happen now, it will not happen on pandemic fears.

Technically the pattern look like one in 2000, when growth stocks were sent high right after 1998 Emerging Markets crisis. As we can study from the Chart 1, the Value-to-Growth ratio had fallen by 35% by 2000. Now it is down 33% already with a high chance to decrease further on Omicron market recovery. We think that the valuation risk will be dominating after the market stabilizes. For that reason we would stick to value stocks in the nearest future.

Chart 2. EURO STOXX Consumer Staples index

European Consumer Staples looks technically interesting — the respective EURO STOXX index has gone down sharply close to its support level (Chart 2). Food producers looks even cheaper due to the cost inflation pressure (Chart 3). We have already highlighted the Food Producers sector pointing that the cost inflation factor is temporary.

Chart 3. Russel 3000 Food Producers index

The attitude towards Food Producers can change with signs of CPI dominancy over PPI. The PPI is generally more volatile, so first spikes of inflation often come with PPI prevailing over CPI. It never last long, however, CPI always tends to catch up with producers prices. This can change investors’ perception and force them to reallocate their assets in favor of value stocks. The value, in turn, will look fundamentally stronger with CPI going up. It is not guaranteed that the value stocks cannot be cheaper. The technical level is interesting, though, so this makes sense to increase the value stocks portfolio part right now.