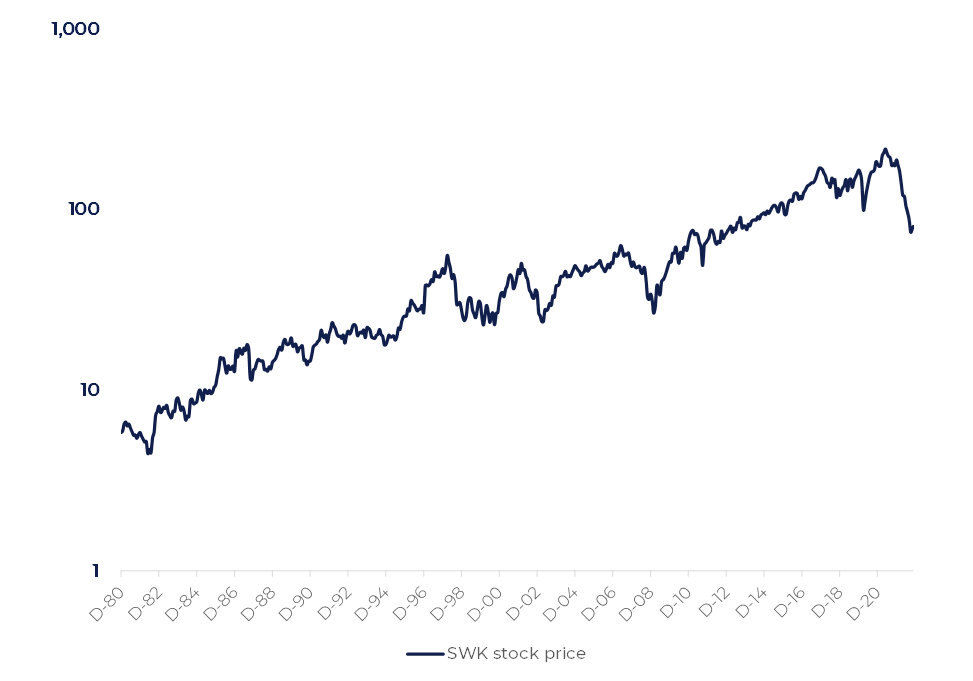

In 2022, SWK experienced the perfect storm which has driven the company’s stock price more than 60% down from its top in July 2021. This happened due to a combination of factors, some are still valid, some not. From a historical perspective this fall is the strongest over the whole forty-years history of the stock’s public trading. It looks like the SWK stocks have a huge upside potential in case the situation stabilizes.

Background

Figure 1 represents the SWK stock’s behavior throughout the whole trading history. Before now there were three big downtrends:

- In 1998 on the back of EM crises

- In 2002 SWK stocks dropped due to the 2001 economic recession

- In 2008 due to GFC.

In all three cases the decline did not exceed 60%. In 2022 the stock dropped by 65%. This brings us to a question of how much is priced in and what should happen to send the stock lower?

Figure 1. SWK stock price, log scale

Stanley Black and Decker produces tools for DIY purposes and industrial construction. Tools & Outdoor segment dominates with 82% share in the company’s sales.

Lifting COVID-19 restrictions brought about the surge in the company’s sales. Now the demand is cooling down and does not look resilient going forward:

- Consumers’ spending on discretionary goods are under pressure due to high energy prices and increased lending rates.

- Consumption of repair tools correlates with the real estate market which is heavily influenced by the high mortgage rates.

- The upcoming recession is still possible. Recessions are bad for both discretionary goods and the real estate.

- Except weak demand the company is suffering from high input costs because of inflated commodity prices.

- Strong dollar does not help either since the production capacities are concentrated in the US.

- The Debt/EBITDA ratio is at 5 which looks high in the soaring rates environment.

Poor execution and traditionally high operating costs are often mentioned as the company’s weaknesses.

The stocks are now in the penalty box. Even for the expected 2002 net income at $700m the market cap of 12bn does not look expensive. For $1+ bn net income which has been the case since 2016 it seems super cheap.

Fundamental picture

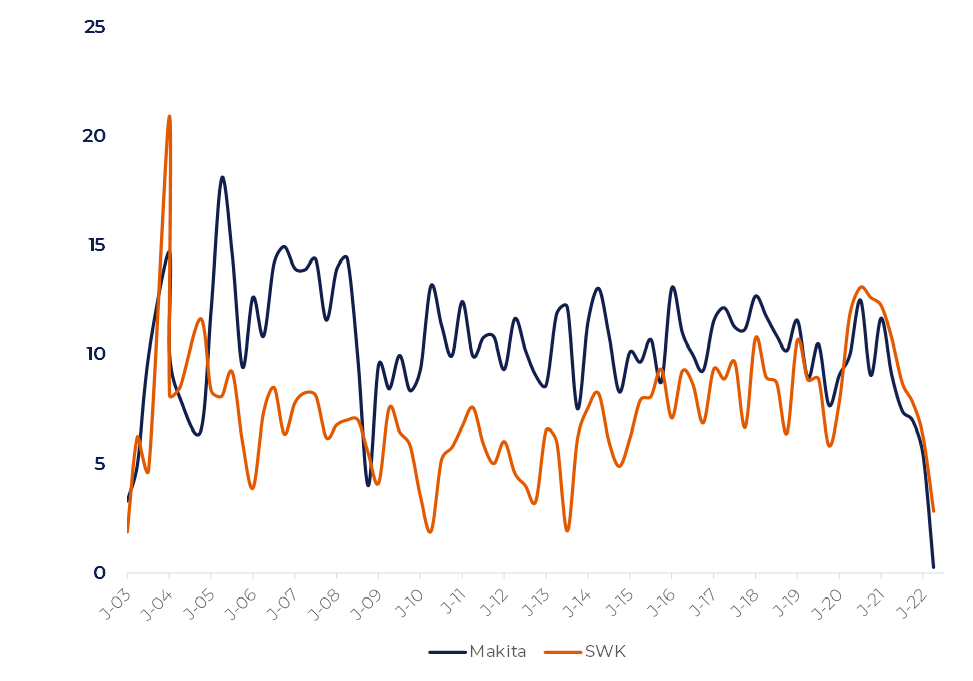

Figure 2 compares the net income margin of two tools producers: Makita and SWK. The patterns are quite similar. That means that the underlying drivers of poor performance are more global than distinctive for the companies.

Figure 2. Net Profit margin. Makita and SWK comparison

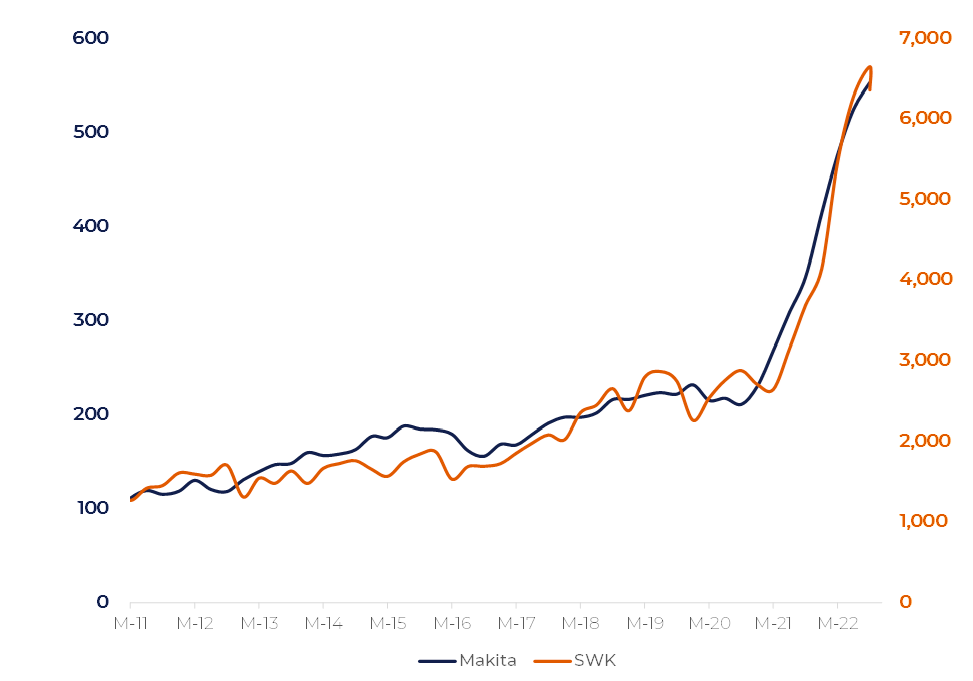

On Figure 3 one can see that both companies experience one common issue: substantial growth of inventories. The management mentioned on Q3 reporting call that reducing inventory is a top priority. It will negatively impact gross margins. SWK’s inventory reduction has already begun and will last until 2H 2023 at least.

Figure 3. Makita and SWK Inventories

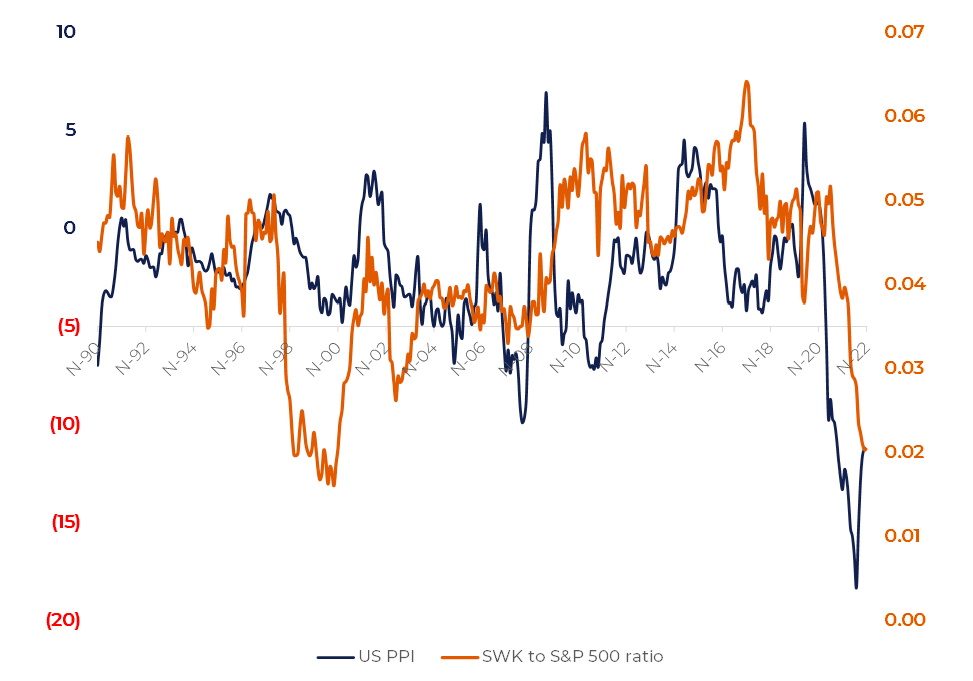

Figure 4. SWK-to-S&P 500 ratio vs US PPI (in reverse order)

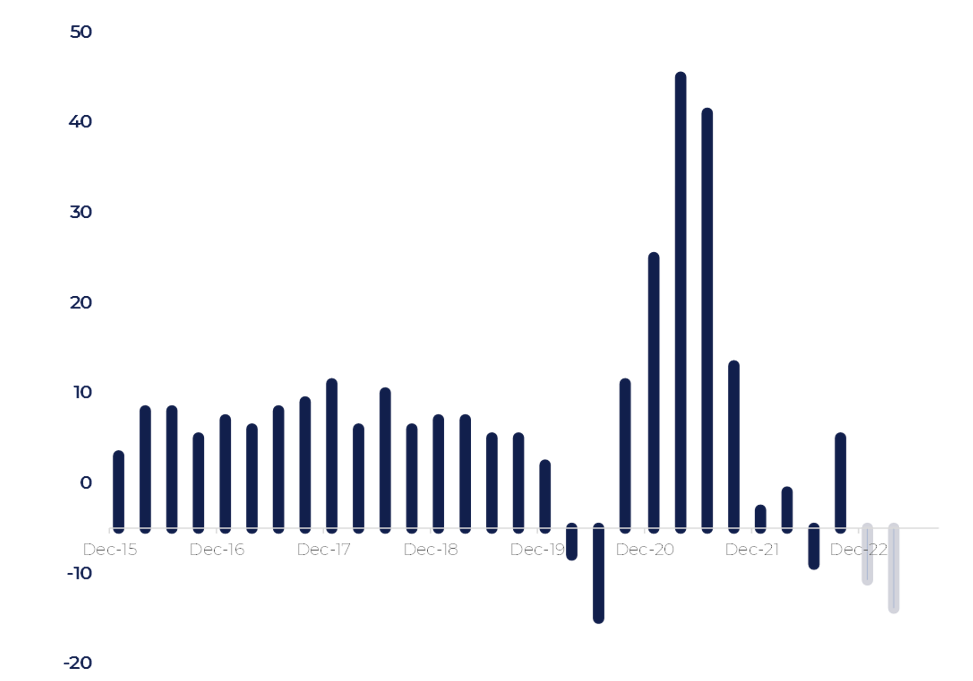

Figure 5. Organic Growth, Tools & Outdoor segment. Quarterly data

COVID-19 outbreak hit the SWK’s 2020 Q1&Q2 sales (Figure 5). Then the topline rebounded and reached 45% in Q1 2021. On the back of strong sales figures and release of the pandemic restrictions the company decided to acquire two outdoor equipment producers: Excel and MTD with the latter representing 80% of total M&A spendings. MTD was acquired for $1.6 billion with Value/Sales being at 0.83 and Value/EBITDA at 10.14. It is worth keeping in mind that the current valuation of SWK is 0.73 in Value/Sales terms.

Besides purchasing the two companies SWK made significant investments in inventory “to help meet the outside demand in the Tools business”[1].

Now it is clear that all those investments were made in the overheated environment. During Q1 2022 earnings call the management mentioned chip shortages and supply chain constraints as the main reason limiting sales. In Q2 it turned out that the demand had dramatically weakened. Actually, consumers’ demand sharply dropped in Q4 2021. In the next, Q1 2022, the company’s profits were hit by rocketed commodities. According to the Q1 2022 earnings call the inflationary impact was a little more than $400 million.

During its Q2 conference call SWK’s managements sounded even more dramatically. According to the CEO Donald Allan “The operating environment clearly has dramatically changed in the last month, especially as we really evolved into the last stages of the quarter or June”.

The US inflation also reached its maximum in Q2 2022, negatively affecting the company’s profits.

However, it is likely that Q2 can be a climax of bad stories for Stanley.

Figure 4 demonstrates that the inflation generally has a negative impact on SWK. Although, the reverse is also true: periods of falling inflation are more often positive for the company. It is worth noting that the stock price reaction usually lags the change in inflation trend. A positive reaction can come 6-9 months after the June CPI peak (Figure 4).

The influence of the recessions can be learnt from the 2001 & 2008 patterns.

It looks strange but in 2001 SWK was in its uptrend. It is truth that the 2001 recession can hardly be applied to the current situation. It is known that the epicenter of troubles was in overheated manufacturing capacities and the IT sector. The US Federal Reserve (‘Fed’) reduced the key rate sharply which stimulated construction and related businesses. Construction was the main driver of quitting recession in 2001.

Unlike 2001, GFC 2008 was closely related to the crash in construction. The 2009 SWK revenue dropped from $4.4 billion in 2008 to $3.7 billion in 2009. The gross profit fell from $1.7 billion to $1.5 billion. As one can see, the influence of the crisis on profits was way less substantial than on sales. The key reasons for that are falling inflation and a downtrend in commodity prices.

It is likely that the perception of SWK is based on the assumption that the company is going to be hit twice: by the cost inflation (which has already happened) and by the lack of demand (which is expected). However, we should keep in mind that the recession is a powerful anti-inflation tool, so it will come along (if it will) with the cost deflation.

The rest depends on a depth of the construction crisis we are expecting. Still, it is not clear whether we are going to see a soft-landing or not. If not, the question remains how tough the hard landing will be. In our view, there is no reason to expect anything like what we experienced in 2008.

Credit Quality and Currency Risk

We can’t avoid taking raising rates into account. In both 2001 & 2008 the Fed responded to the worsening economic environment by sharp decreases of the key rate. Now the situation is opposite.

The SWK net debt is about $8 billion. The debt increased in 2020-2021 because of the aggressive M&A strategy. Even low expectations of $1.6 billion of EBITDA lead us towards 5x Debt/EBITDA which looks OK. The company is A-rated with S&P and (A-)-rated with Fitch. Fitch, unlike S&P, has changed its outlook to “negative”. It happened on 28th September and one of negative factors sending the stock price below 80.

The potential downgrade from Fitch can be another negative surprise going forward. However, from a fundamental price stock perspective it does not change much. For equity investors it is more important that the company will be capable of raising debt with a comparatively small premium to US treasuries. SWK will need to refinance $1 billion in 2025-2026. The rates will likely return to normality by that time.

So, the refinancing risk is very small.

The negative influence of expensive dollar is estimated by analysts at (-2.5%) on the topline[2]. Regression analysis for 2009-2022 shows that 1% of USD appreciation on average slashes the SWK gross margin by 0.2%. The net income margin follows suit. However, we must be cautious to jump to the conclusion about the FX impact. It is known that the dollar generally strengthens in turbulent times. By the way, the S&P 500 index also weakens by ~0.2% with one percent of the dollar appreciation. Therefore, the contraction of SWK margin is more likely a reaction to the worsening economic situation rather than the influence of FX.

The 60% of Stanley’s producing capacities are in the US with 60% of sales coming from the US. That means that FX only affects the topline. Every 10% of the dollar appreciation takes out 10% of foreign sales which makes 4% of the total revenue. The analysts’ estimation of the FX impact at (-2.5%) corresponds to 6.25% of the dollar appreciation in 2022 which is close to what we see in the FX market.

Anyway, both FX and credit risks are small and can be ignored amid 60% of the stock decline.

The long-term fundamental value of SWK

Stanley Black and Decker is a typical example of a mature company dominating in its market segment. For this reason, the organic growth seems to be limited, so the growth strategy can only rely on the M&A. Since 2010 the company has spent $7.3 billion on M&A[3]. This represents circa 5% of total sales for this period. The recent large case with MTD shows that SWK is ready to buy companies with EBITDA margin at high single digits level which is 7-10% lower than SWK has[4]. The restructuring of MTD aiming to improve its margins will take 4 years, according to the SWK’s estimates. This means that Stanley will be losing up to ~5% per annum for the next four years, paying in total 15-20% of its annual revenues for subsidiary restructuring.

Given that the average annual historical acquisition cost for Stanley stands at 5% of revenue with the restructuring cost for acquisitions is 20% of their value, the total acquisition losses for Stanley make (5%*20%) = 1% of its annual revenue.

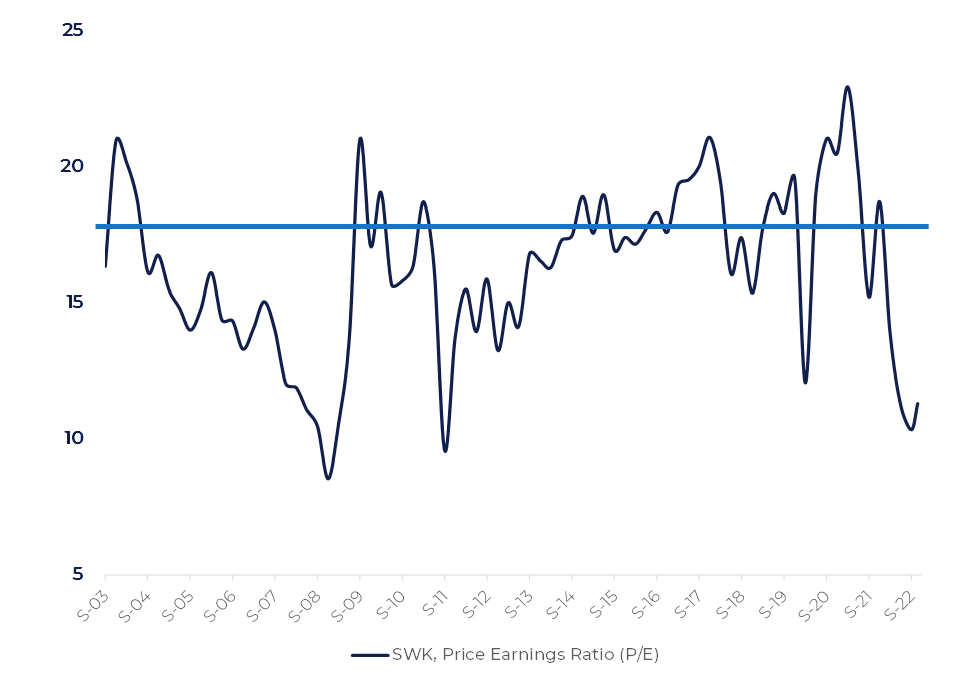

This is nothing but the payment for growth and should already be reflected in lower income margin. Aggressive M&A approach makes out of SWK a holding to a certain extent. The P/E metrics for holdings should be discounted. Historically it stays at 17.5x which seems reasonable (Figure 6):

Figure 6

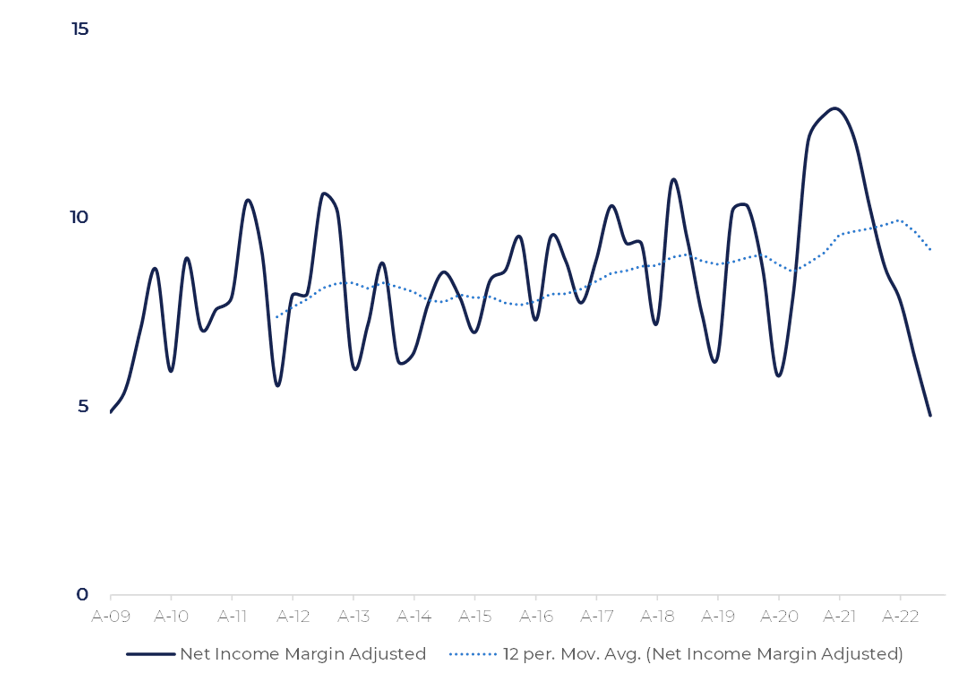

The net income margin has been in an uptrend over years and can be conservatively estimated at 8.5% (Figure 7):

Figure 7. SWK, Net Income Margin and its 3-year Moving Average

We are taking 2019 revenue of $14.5 billion as a starting point for further calculations. The two companies bought in 2021 bring in circa $2.5 billion of revenues. Hence, the total figure stands at $17 billion as of 2019 (pro-forma).

The total inflation impact on goods price is going to be circa 20% by the end of 2023[5]. This gives us an estimation of SWK sales at $20.4 billion at the end of 2023. We do not consider the disposal of the security business assuming that all subsequent M&A activity is valuation neutral.

With the net income margin at 8.5% and P/E at 17.5 we get the equity value at $30.3 billion.

The current market capitalization of SWK is $12 billion.

Summary

The upside potential of SWK stocks is huge: circa 2.5 times. This upside can be fully taken when the macro environment and the real estate market condition stabilizes.

The most important macro factors for the company are:

- The decline of inflation (positive factor)

- Entering recession and worsening conditions in construction (negative factor)

FX risk and high rates are secondary and can be ignored amid two factors set out above.

The decline in margins is primarily connected to the surge of inflation which affects the company’s costs mush more than the sales. Since August-September 2022, the lack of demand has become the main negative driver.

We assume that SWK stocks turned out to be under pressure from both factors: high inflation and the recession expectations. It seems to be underestimated that the deeper the economy slowdown will be the faster prices will be falling.

We think that 1H 2023 will be the period when these opposite drivers (inflation and slowdown) will affect the company resulting in a series of positive and negative surprises with cumulative neutral result. A typical recession lasts for 6-12 months with the mid-point being the best moment for buying stocks. Hence, at some point in 2023 the investors’ perception of Stanley will likely turn positive.

Given the stocks’ 2.5 upside potential and how much is already priced in, the downside from the recent bottoms seems to be limited.

The key risks are:

- Poor execution of M&A deals

- Situation when the economy slowdown is accompanied by high inflation (for example, negative development of the Russia-Ukraine war)

[1] SWK Q1 2022 Earnings Call

[2] As of 25th of November 2022

[3] This figure does account for the sale of several security business divisions sold in 2022 for $4.1 billion.

[4] Stanley Black & Decker To Acquire Remaining 80% Stake In MTD Holdings announcement. “Together Stanley Black & Decker and MTD have a compelling pathway to introduce new and innovative products for professional and residential outdoor equipment customers. MTD has made significant progress in improving its EBITDA margin from 4.5% in 2018 to high single digits over the last twelve months and there is runway for further EBITDA margin improvement to the mid-teens over the next four years as cost and revenue opportunities are realized.”

[5] Accumulated CPI since 2019 is 15% as of November 2022. The estimation for 2023 is made on the base of gradually slowing inflation back to 2% until December 2023.