Intentionally or not the Fed Chair Powell is stepping onto the path Ben Bernanke was exploring 17 years ago. We found it useful to look back and take a snapshot of the 2007 business environment and see the way investors and regulators assessed the situation.

After the Federal Open Market Committee (FOMC) meeting on September 18, 2007, the Fed reduced the target rate from 5.25% to 4.75%. Bernanke emphasized that the decision was made to "help forestall some of the adverse effects on the broader economy that might otherwise arise from the disruptions in financial markets" and to "promote moderate growth over time."

First, we must acknowledge that the fundamental backdrop for the September 2007 rate cut was different. Housing prices, which had surged between 2000 and 2005, had stalled. The value of many financial instruments tied to real estate declined. In June 2007, two Bear Stearns hedge funds backed by mortgage-backed securities (MBS) collapsed. By July and August, Lehman Brothers' shares had dropped 30%. LIBOR suddenly diverged from the Fed’s key rate, jumping 50 basis points from 5.3% to 5.8% in August-September.

So, Fed Chair Bernanke had enough reasons to justify the rate cut.

However, it would be a mistake of “hindsight bias” to assume that the upcoming financial crisis was obvious at the time. Investors tended to downplay the risks, believing they were manageable—much like how many are overlooking the almost 1% rise in unemployment now.

Here’s what the news looked like on September 18, 2007:

· Greenspan Says He Didn't Fuel Housing Bubble With Low Rates

· Oil Rises Above $82 for the First Time on Lower Interest Rates

· Microsoft Says Sprint Uses Software for Voice Search

· Pimco's Gross Says Fed Will Cut Rates to at Least 3.75 Percent

· Homebuilders Rise on Speculation Buyers Will Return

· Moran of Daiwa Sees `Inflation Consequences' on Fed Cut

· IBM Targets Wall Street for Supercomputer Servers

· Lehman Sees Crisis Easing as Smaller Rivals Falter

· Treasuries Lower on Profit Taking

· Apple Says iPhone to Be Sold in the U.K. With O2

· U.S. Stocks Gain After Fed Cuts Benchmark Rate by Half a Point

Life in the financial markets carried on. Investment firms were still recommending buying U.S. bank stocks after the rate cut. A recession was seen as possible but not imminent. On September 18, Fannie Mae’s chief economist David Berson said in an interview:

“The recession possibilities have certainly gone up in the last few months because of the housing downturn, the liquidity crisis, and slowing job growth. I would put the chance of a recession at 40 percent. The Fed action hasn't changed that.”

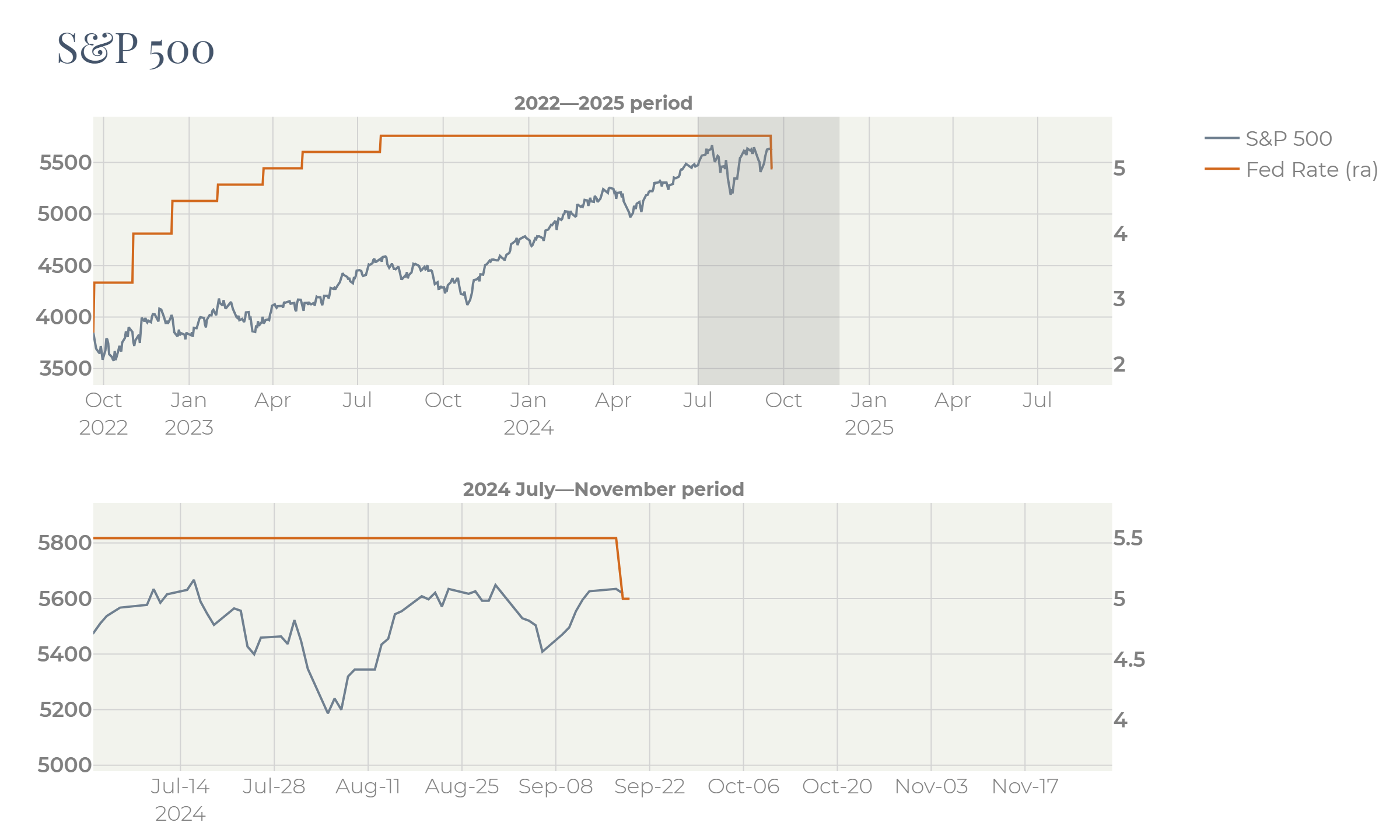

The housing market was just one part of a broader picture, which didn’t look catastrophic at all. Here, we offer a comparison between the macroeconomic situation of 2007 and what we observe today.

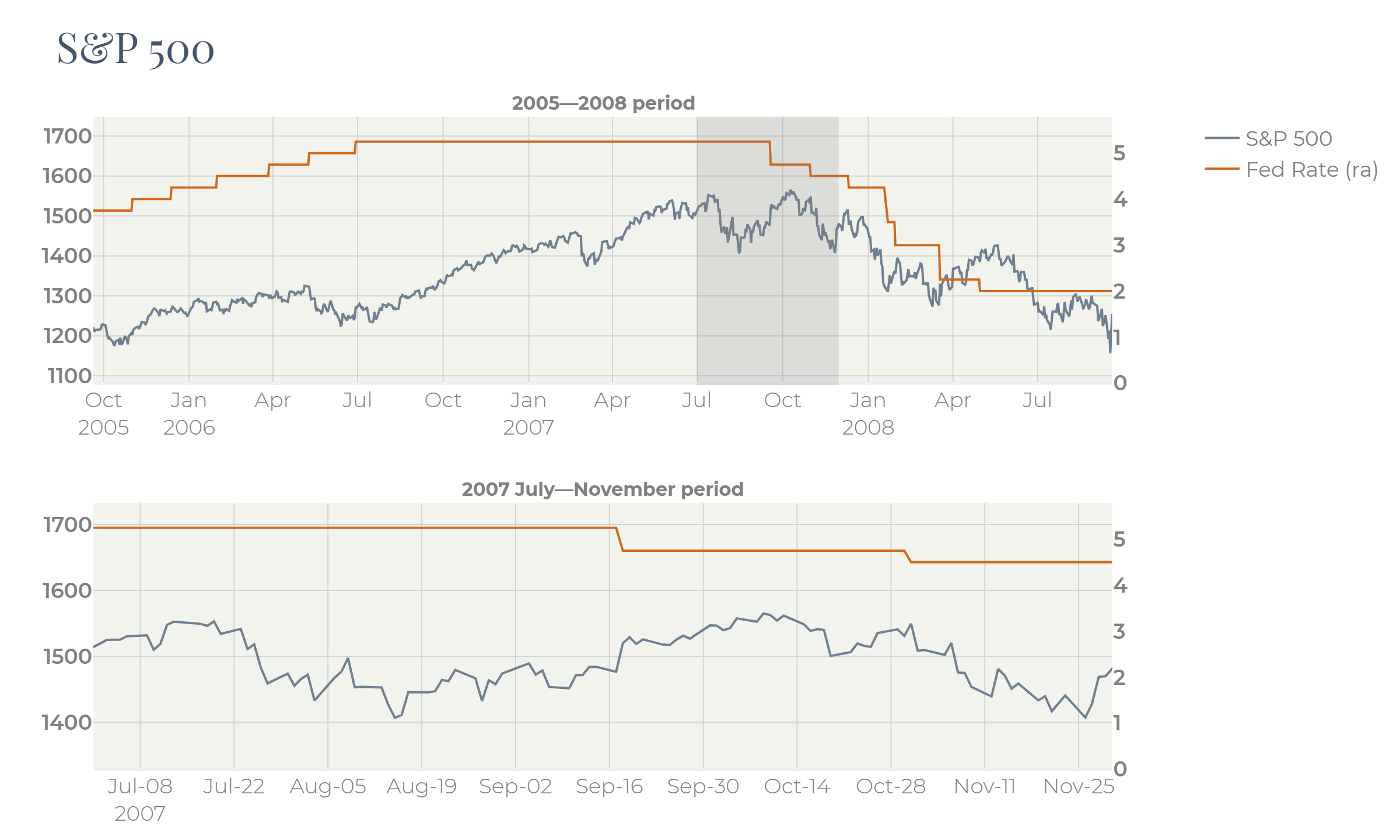

Investors did not expect the 50bp cut. This is clear from 1-month US Treasuries rates. So, the Fed decision was a surprise for the stock market. Optimism, though, appeared to be quite short-lived:

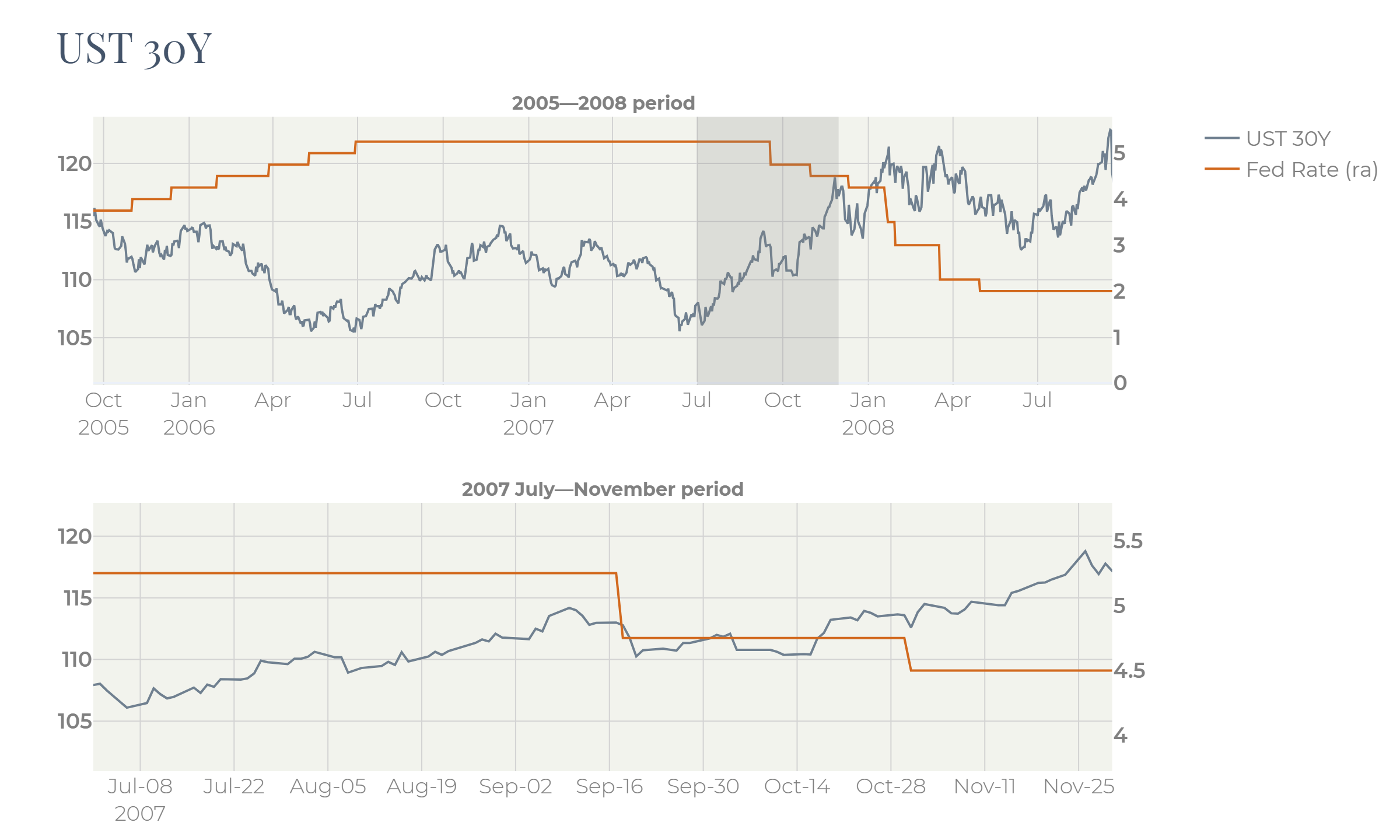

The US Treasury bonds, by contrast, corrected. Fixed Income had been under pressure for several years on the back of elevated rates. Bonds had risen on expectations before the Fed decision, but investors preferred immediate taking profit:

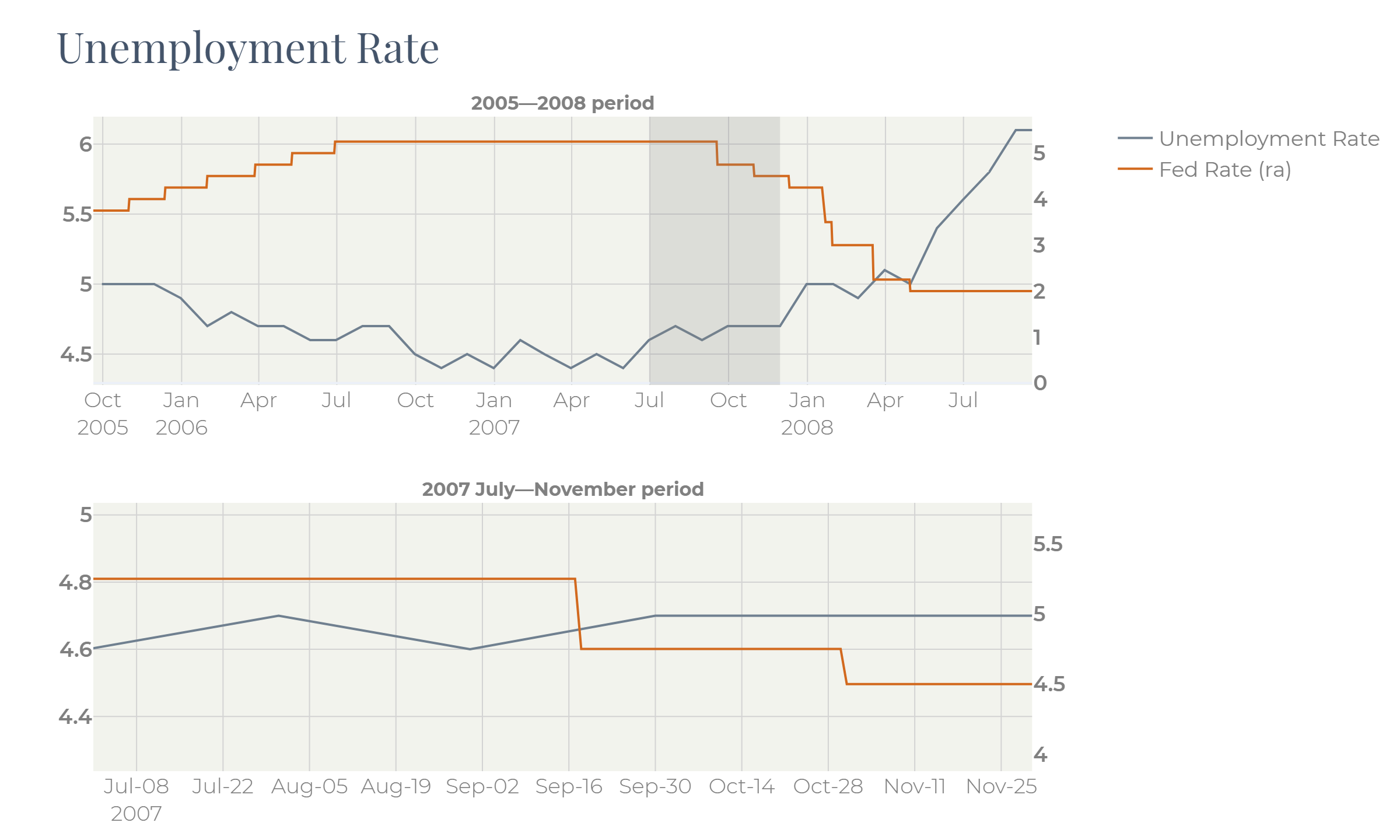

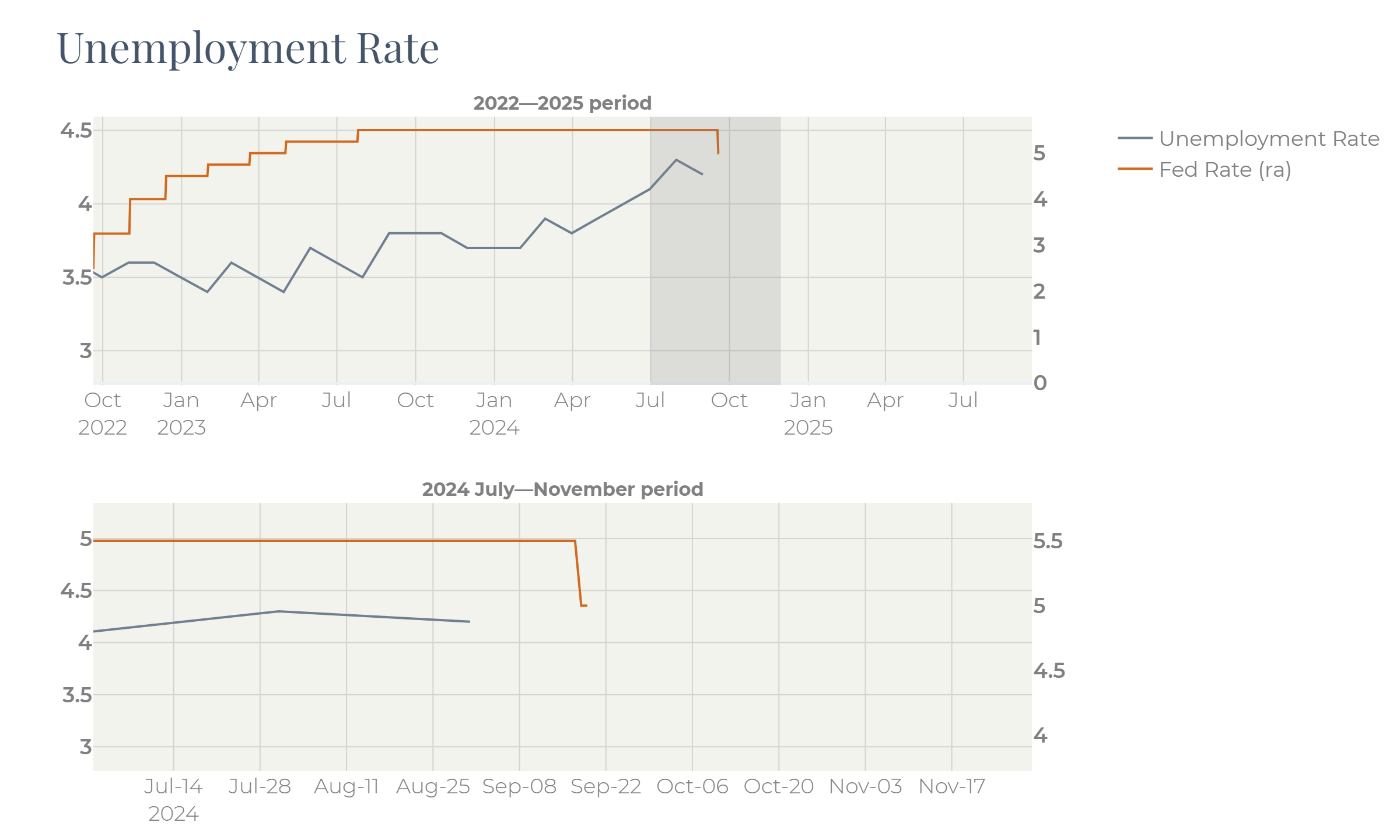

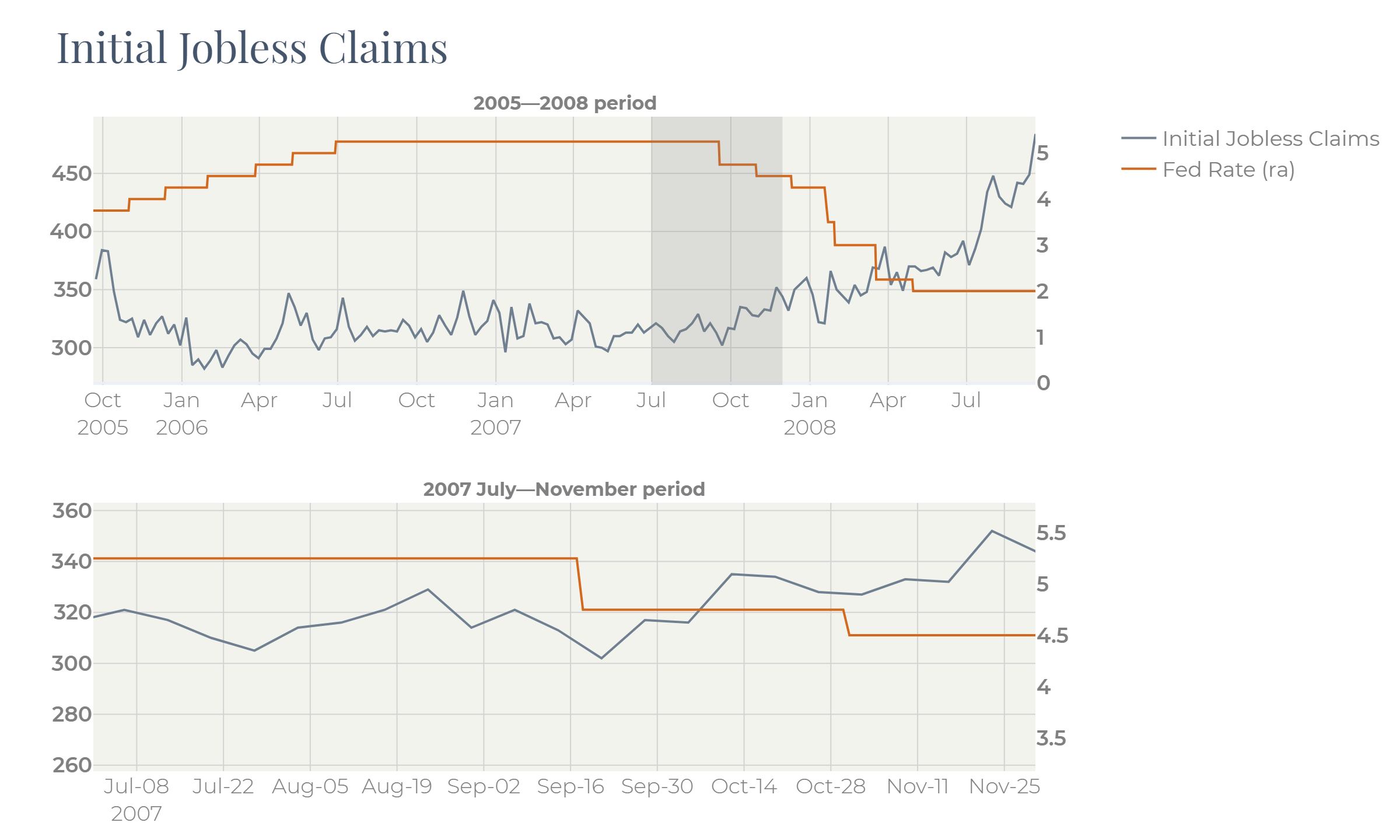

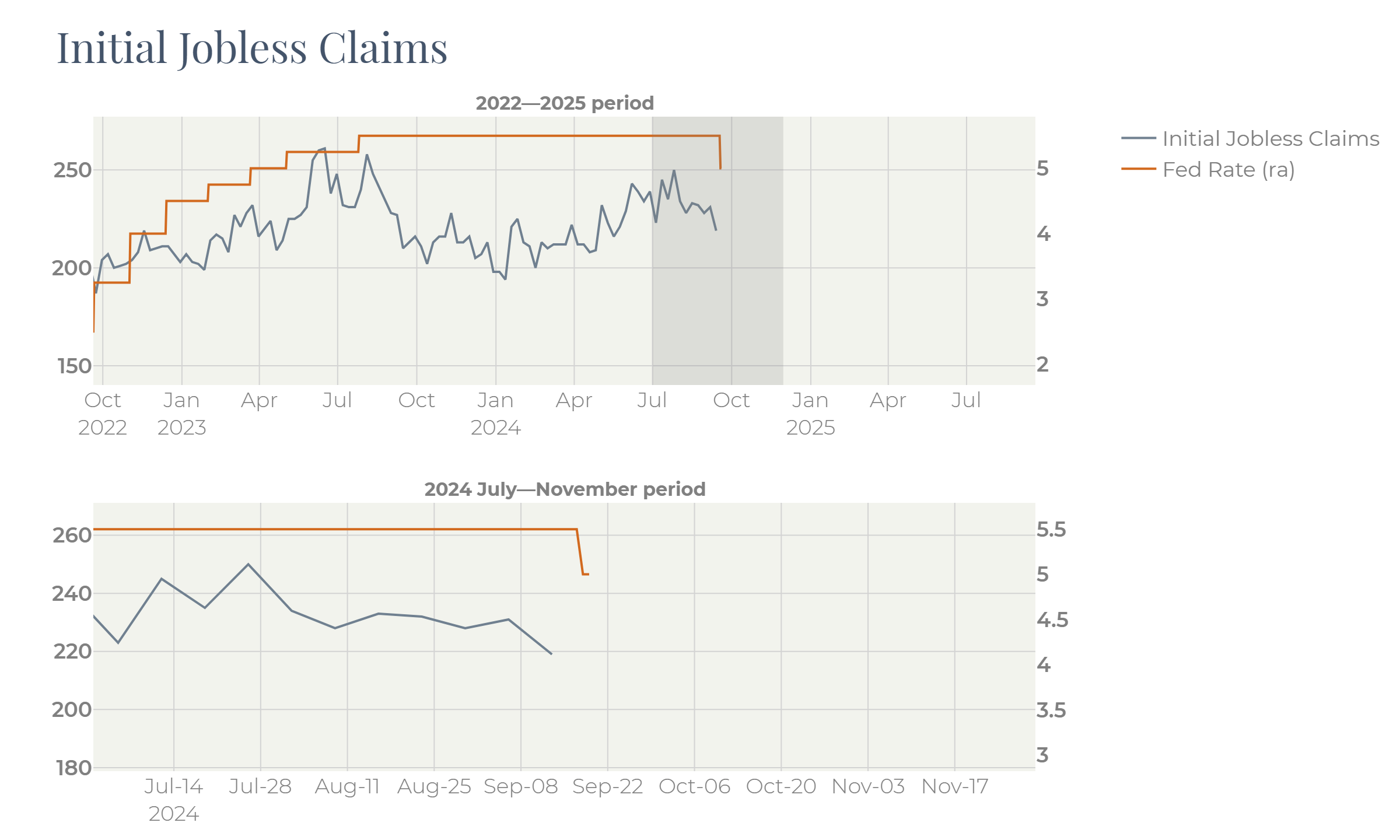

The labor market had shown the first signs of weakness with the unemployment rate having risen 0.3% from its recent historical low:

Growth in unemployment did not look disastrous and did not come along with the spike in jobless claims:

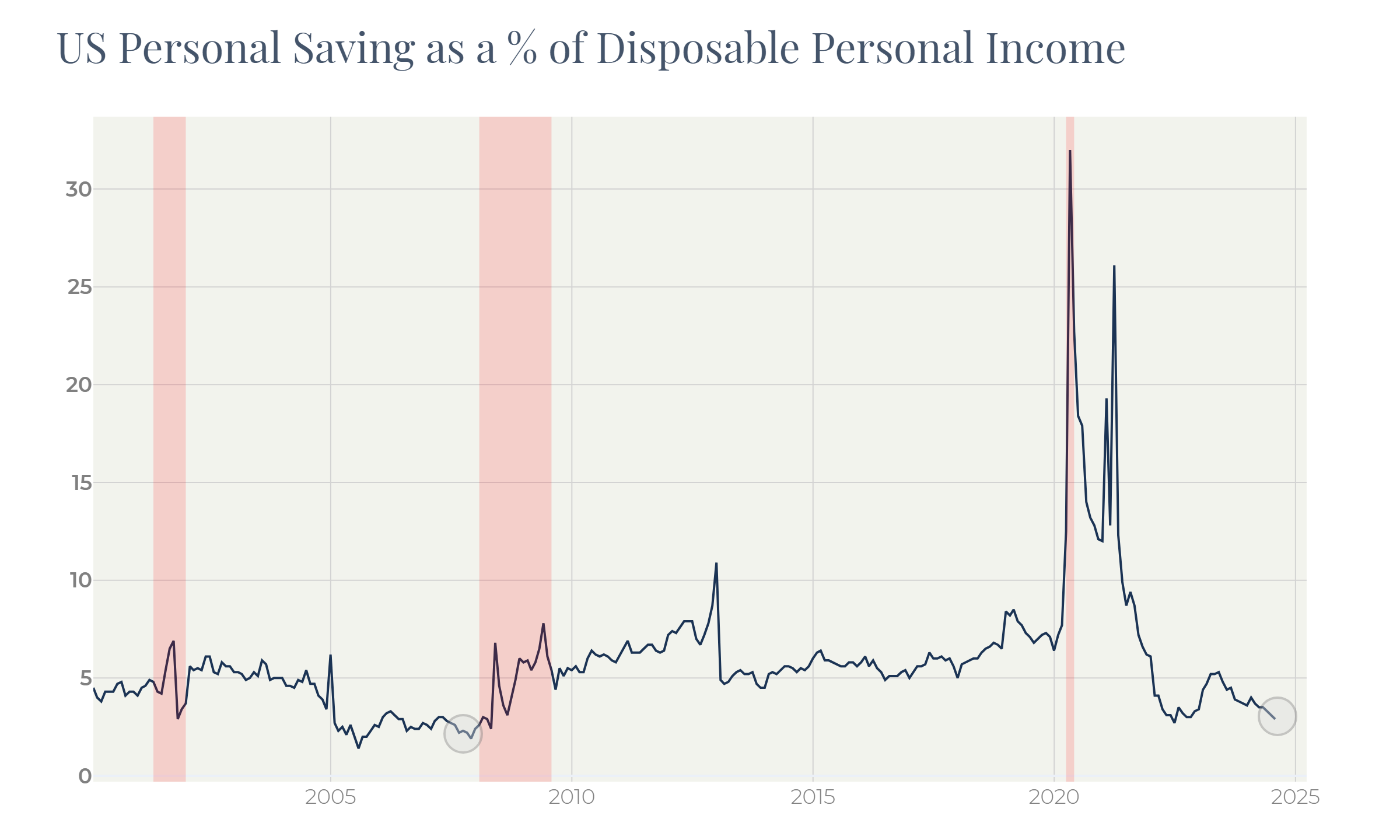

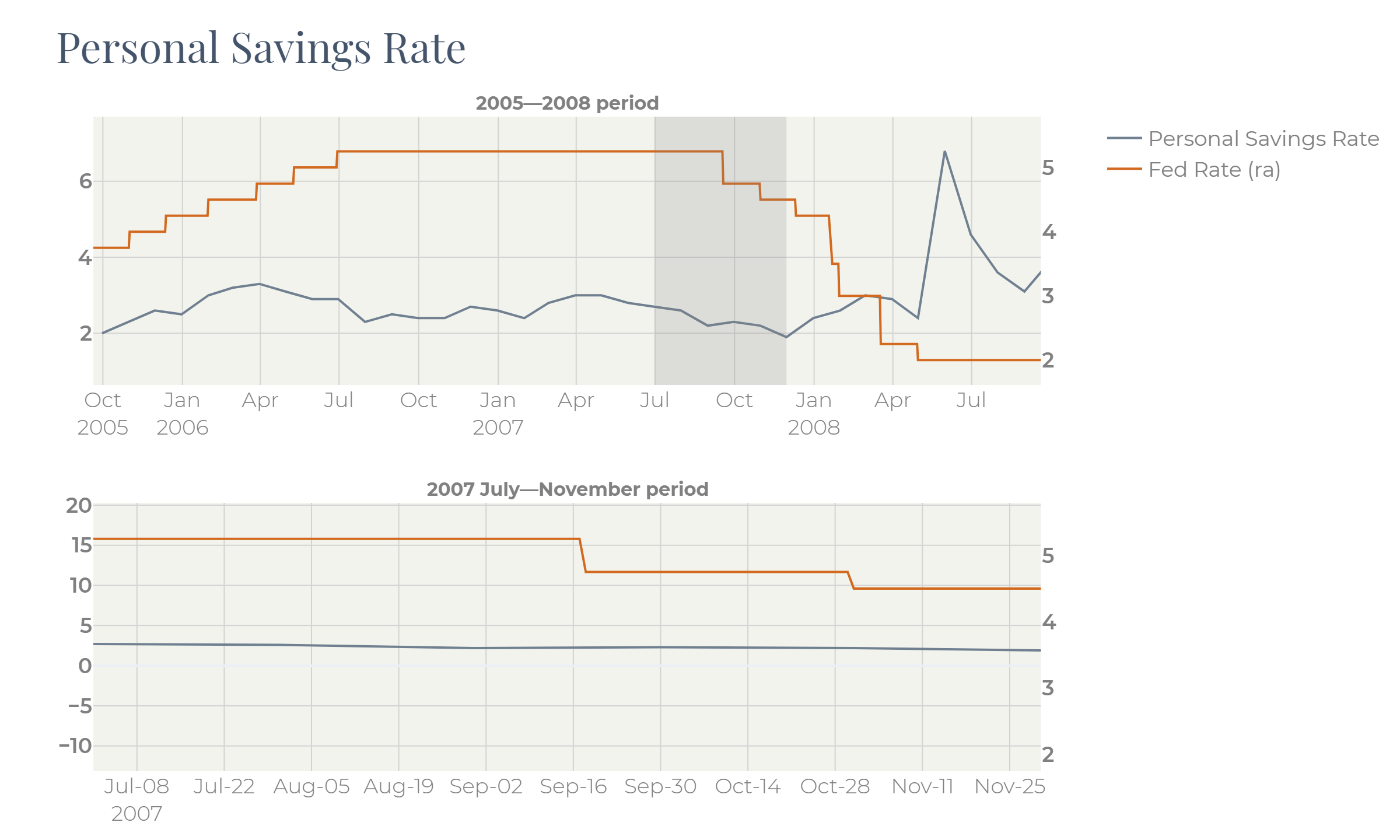

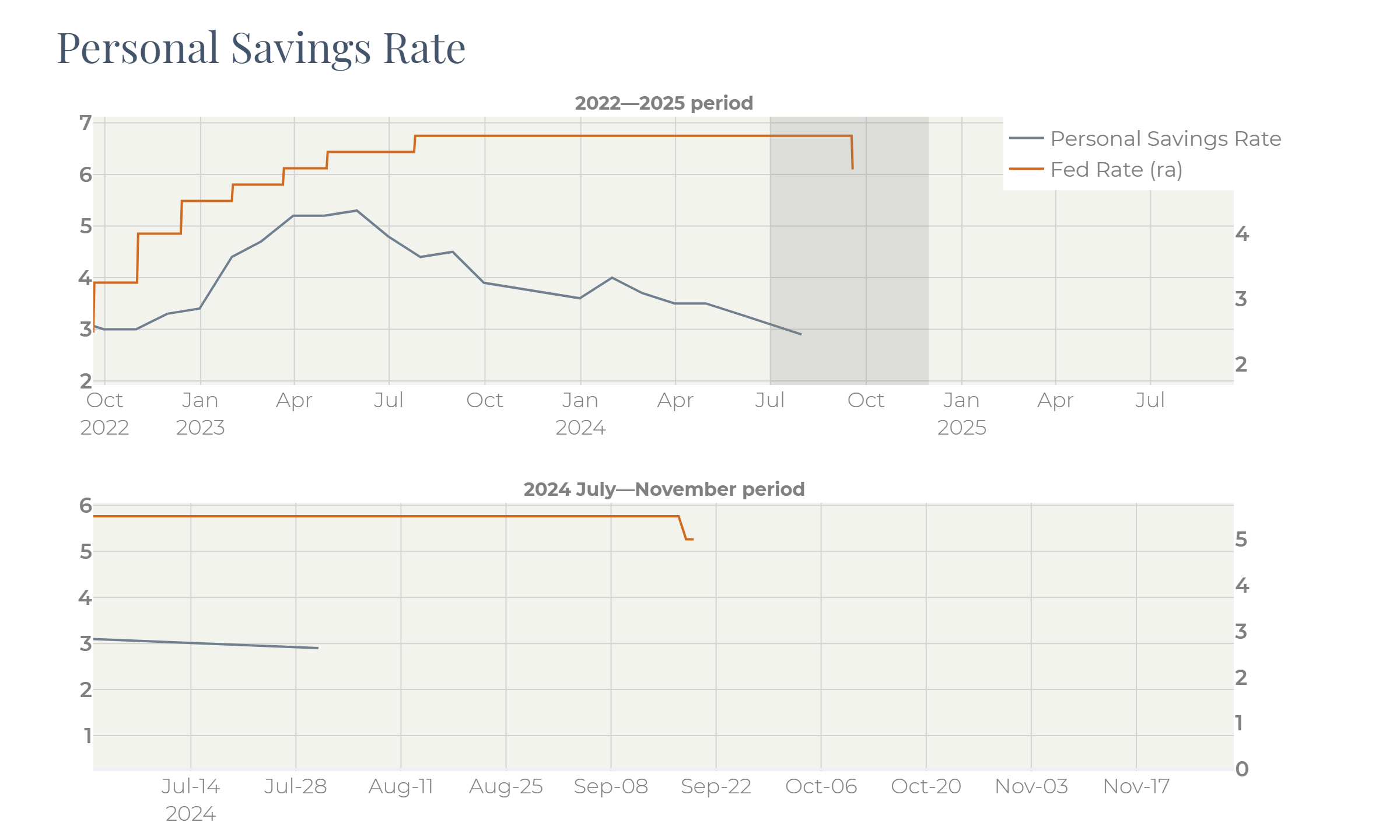

Consumer spending was on a very high level with the savings rate approaching its historical 2005 low:

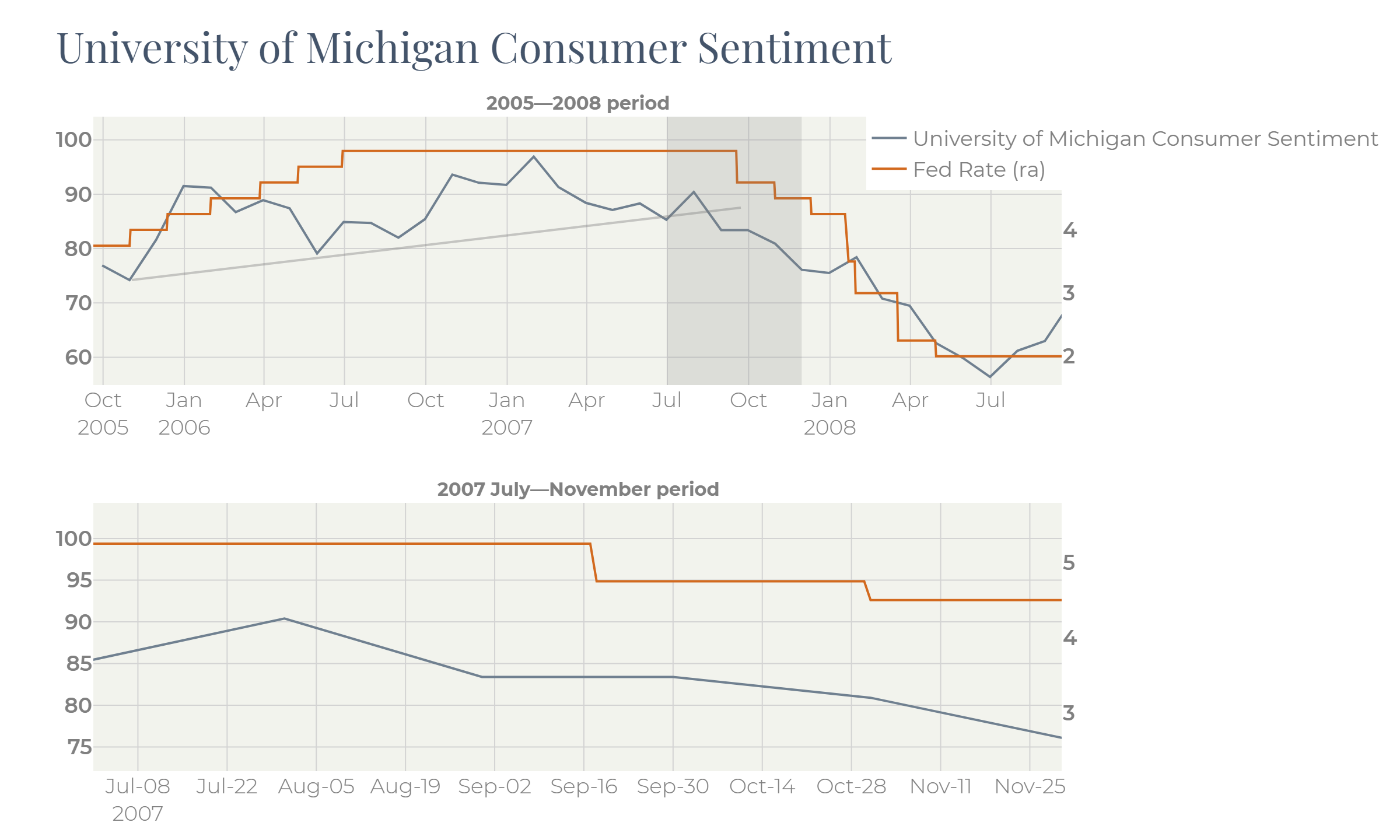

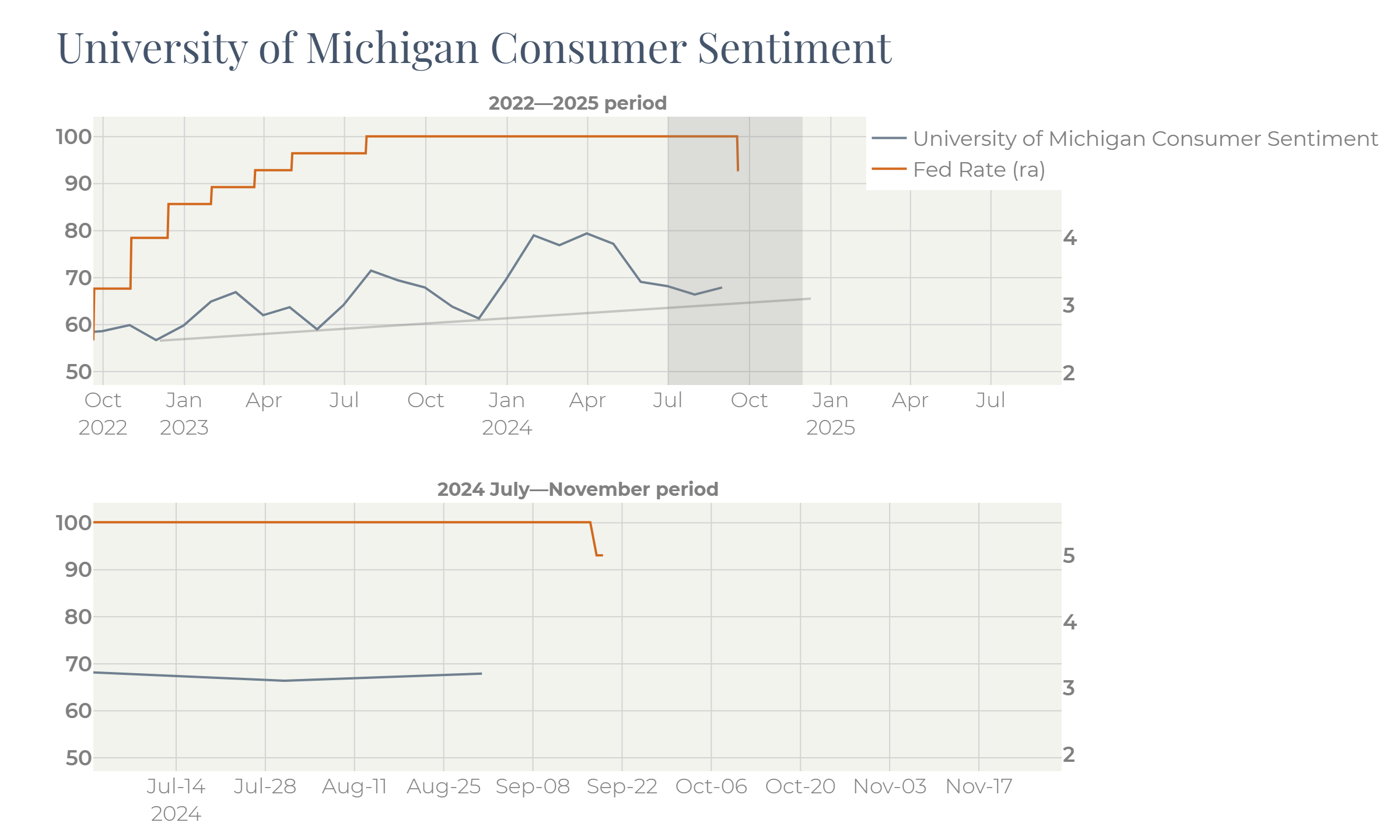

The Consumer Sentiment measured by Michigan University corrected prior to the rate cut but remained in the uptrend just like what one can observe now:

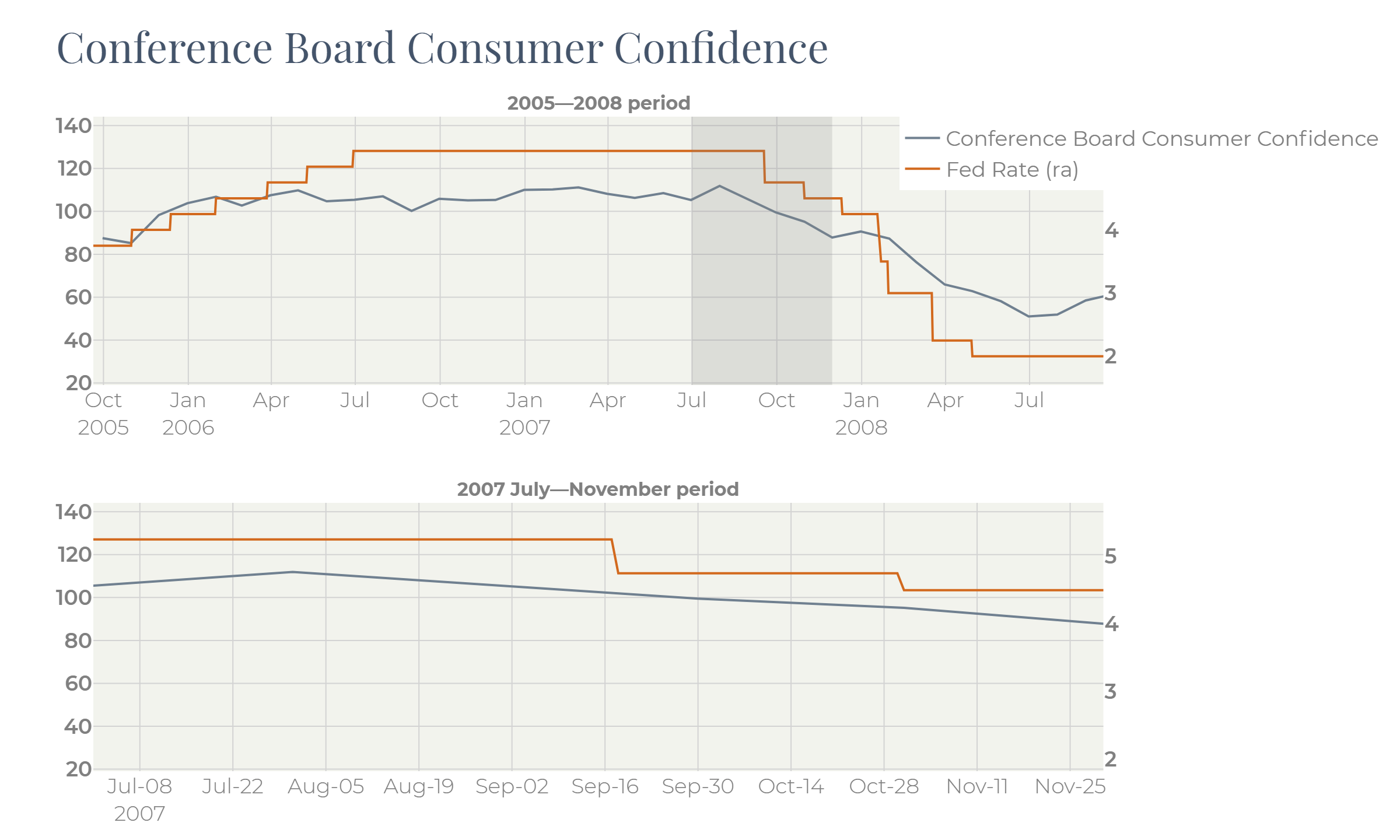

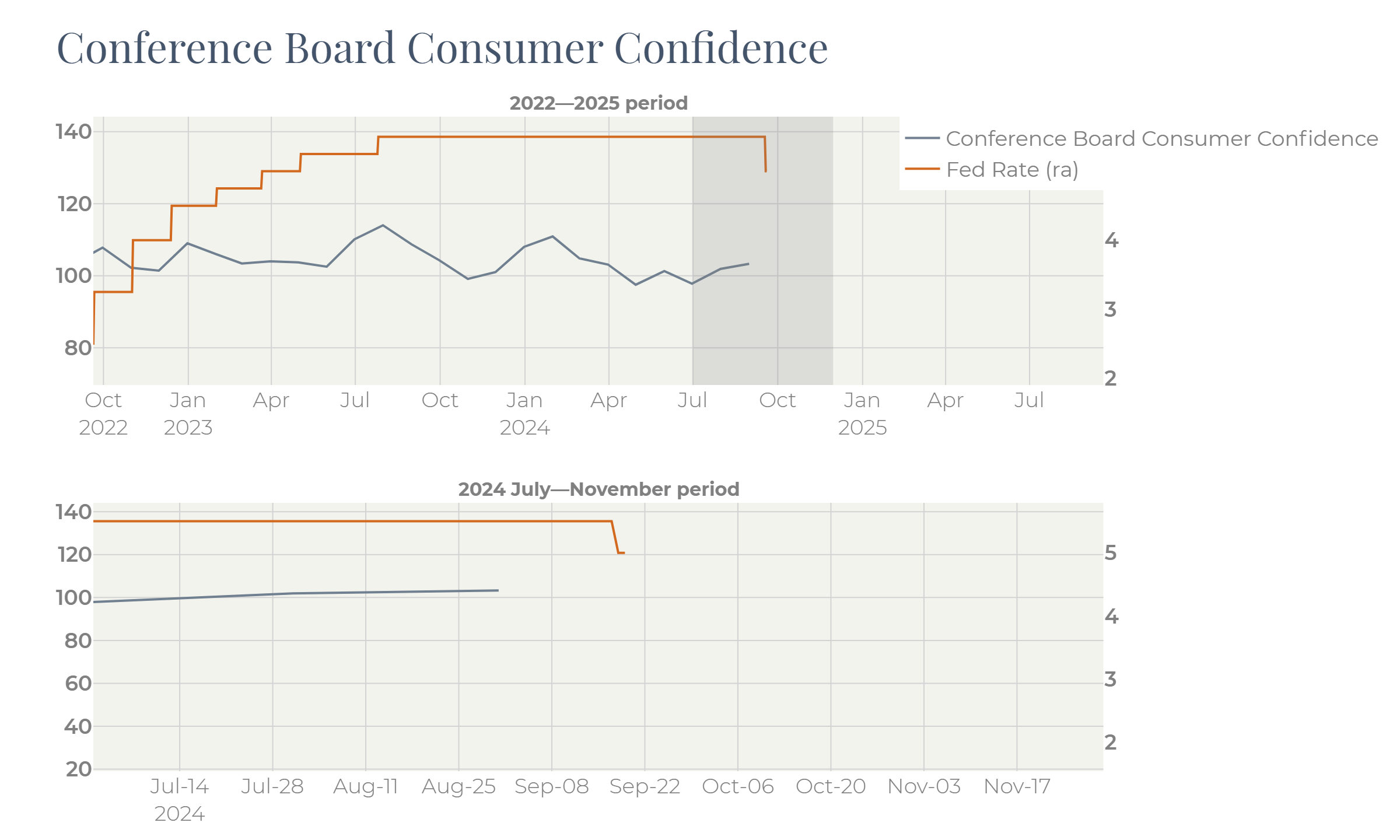

The Conference Board Consumer Confidence was just flat:

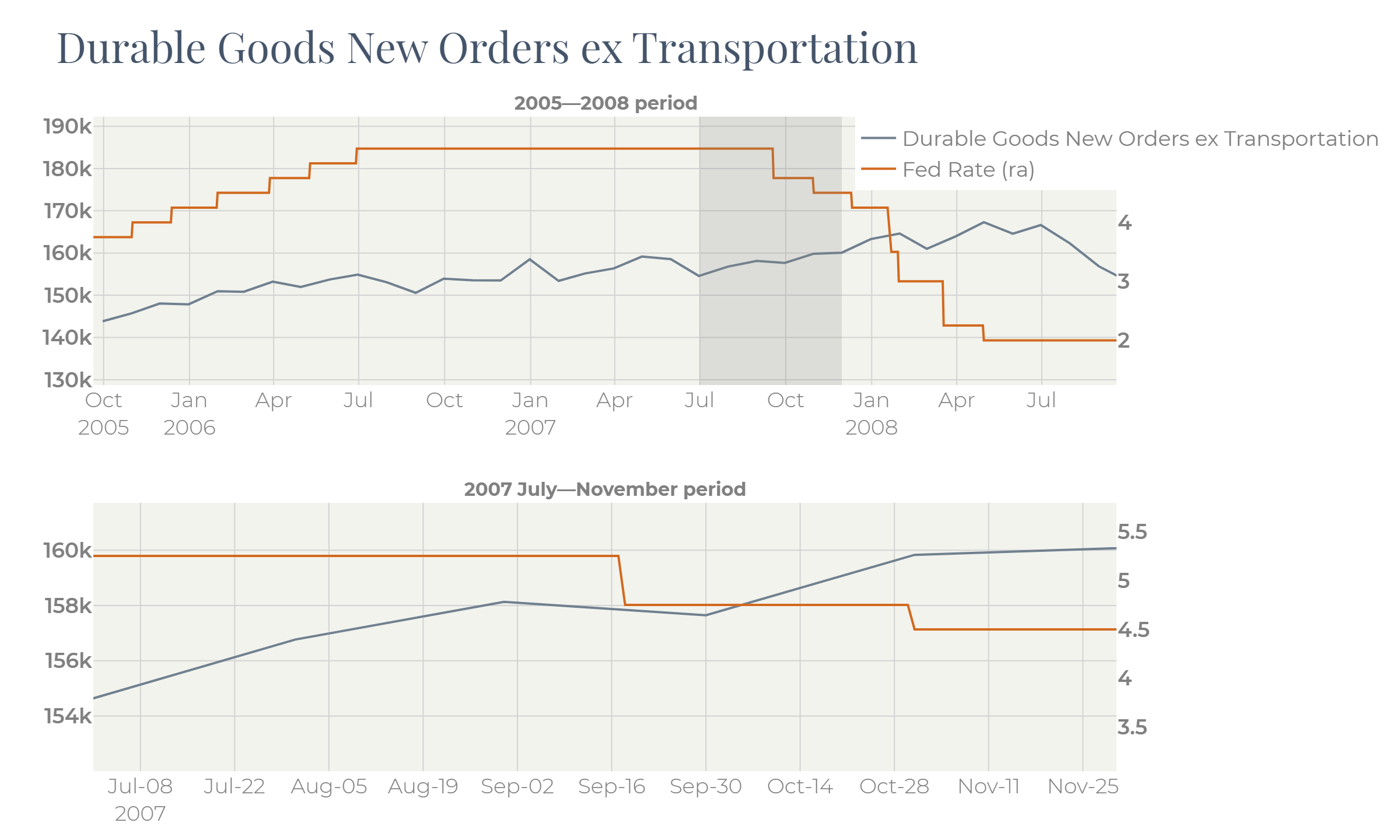

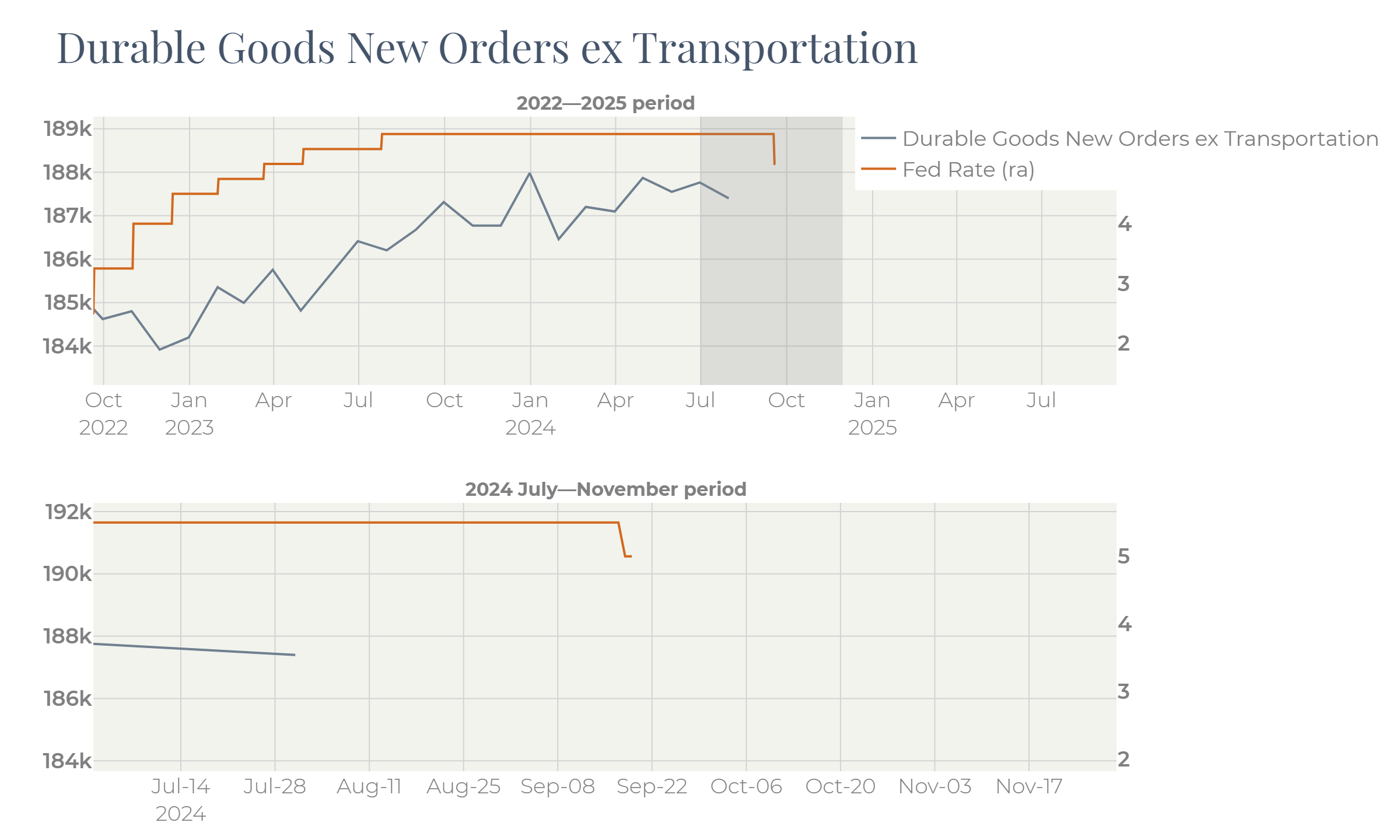

Consumer optimism supported Durable Goods orders:

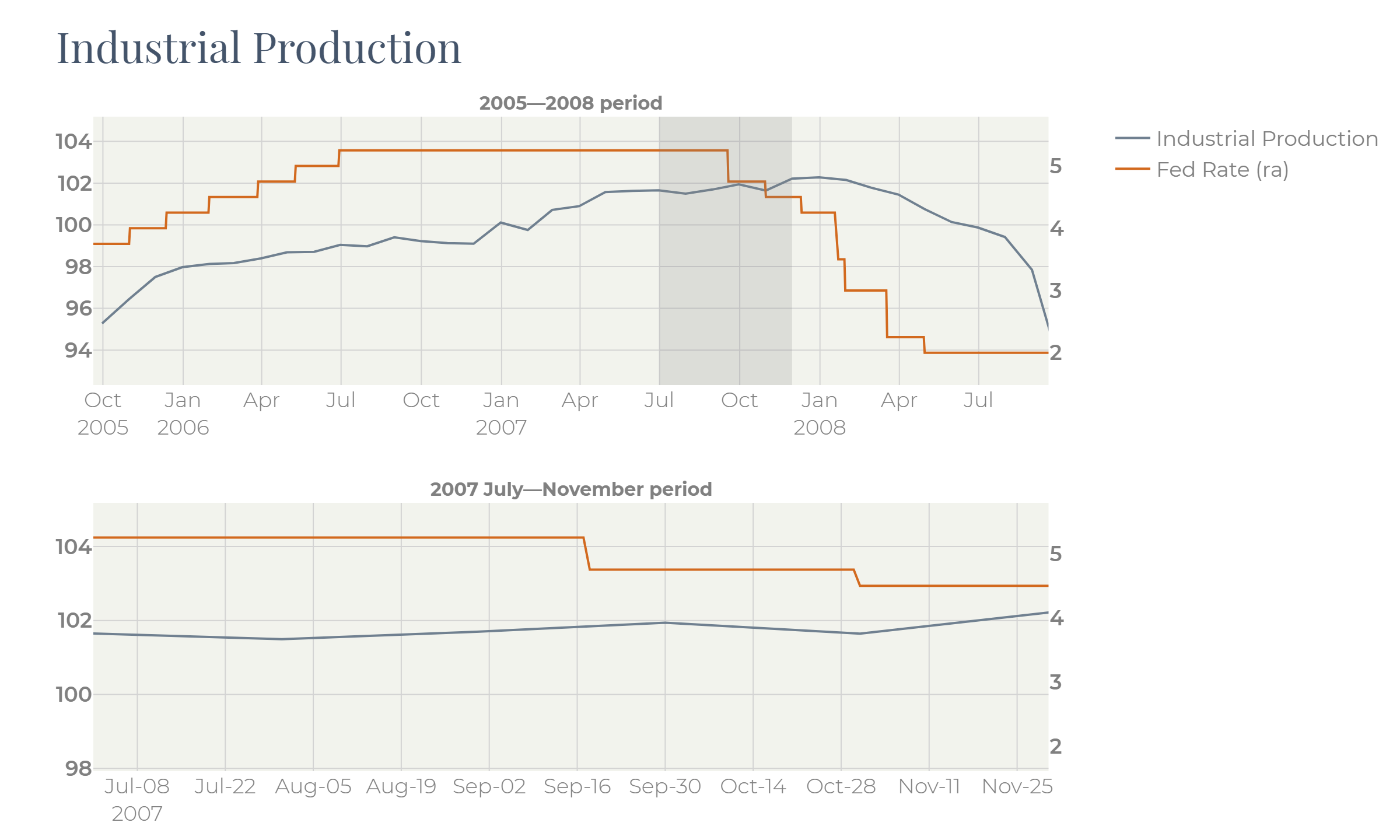

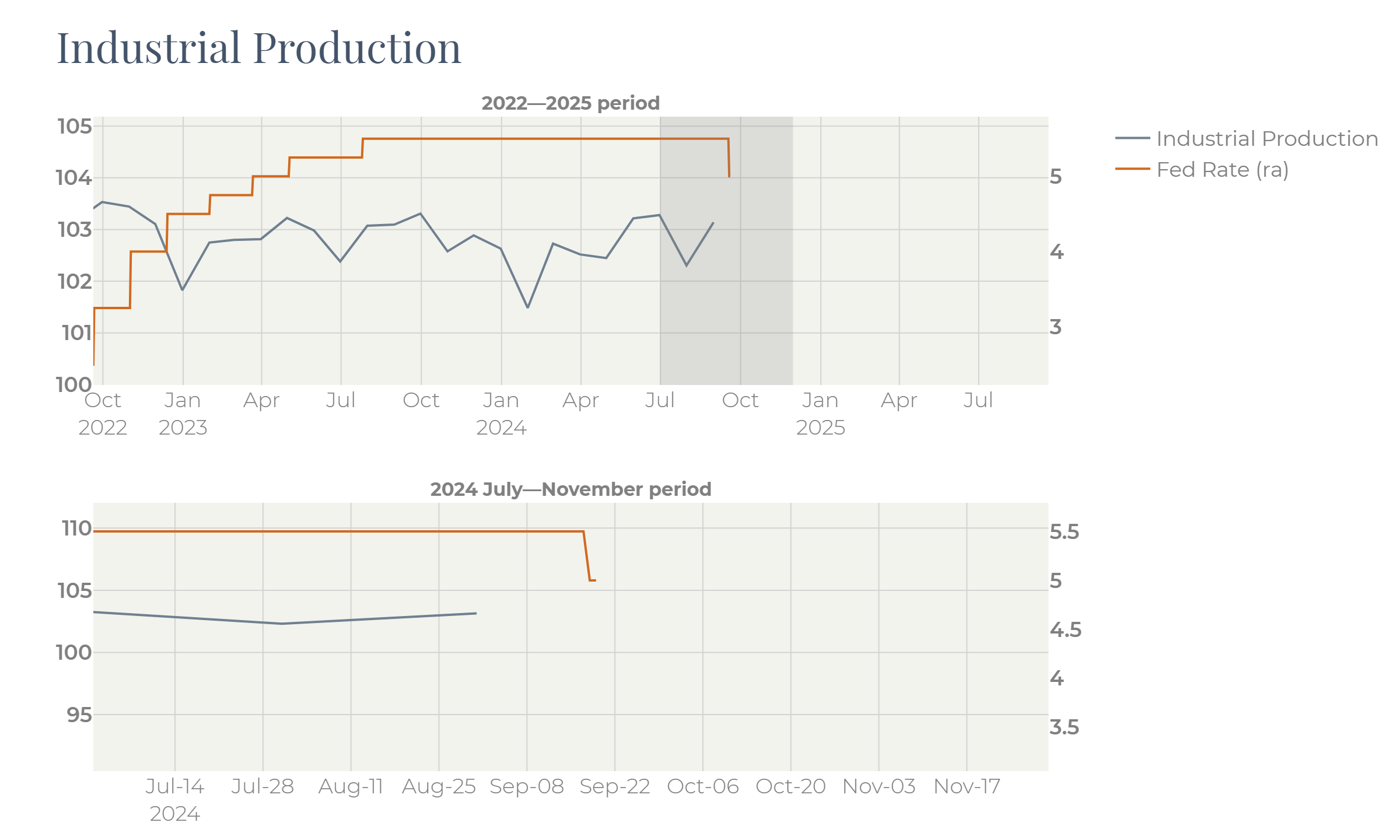

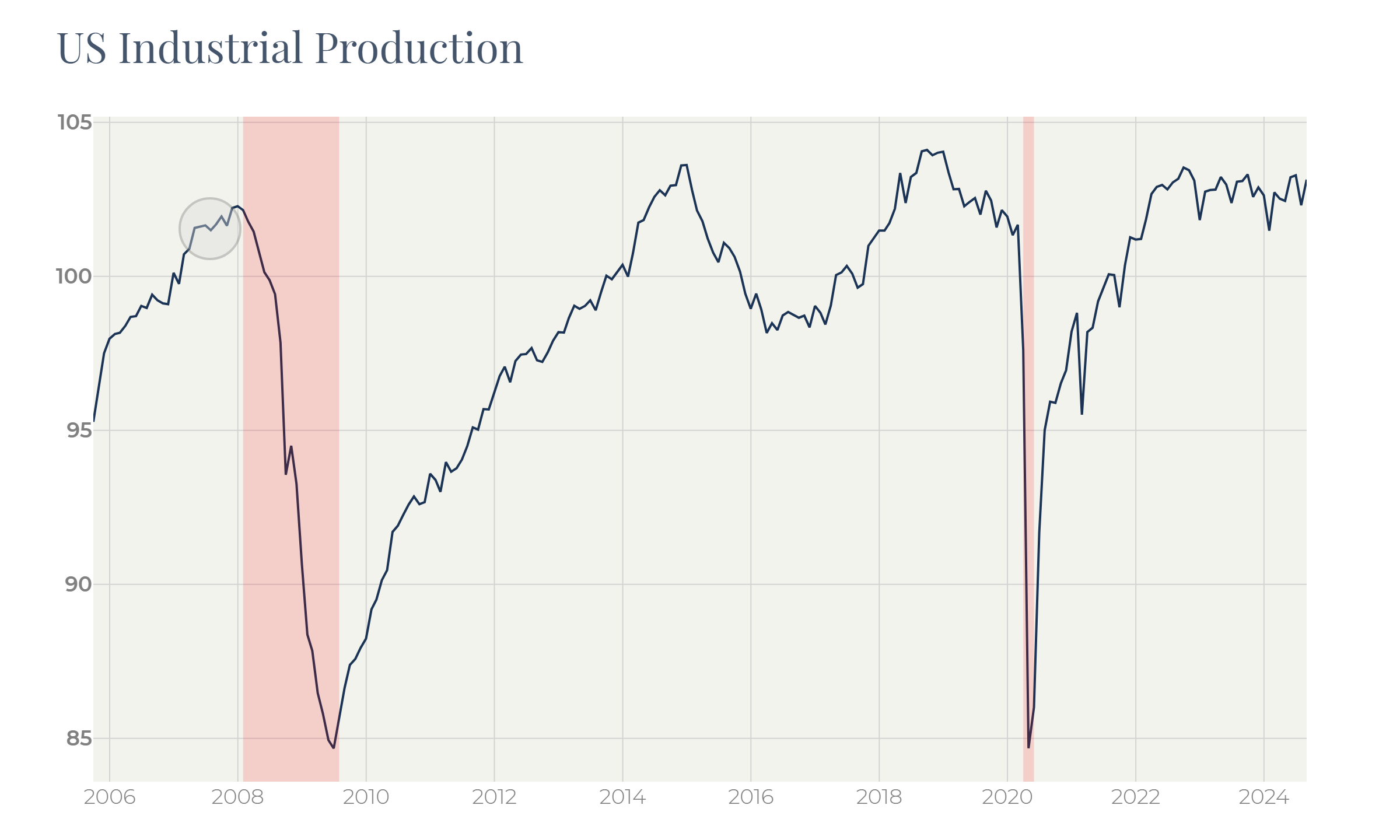

Industrial Production looked good as well:

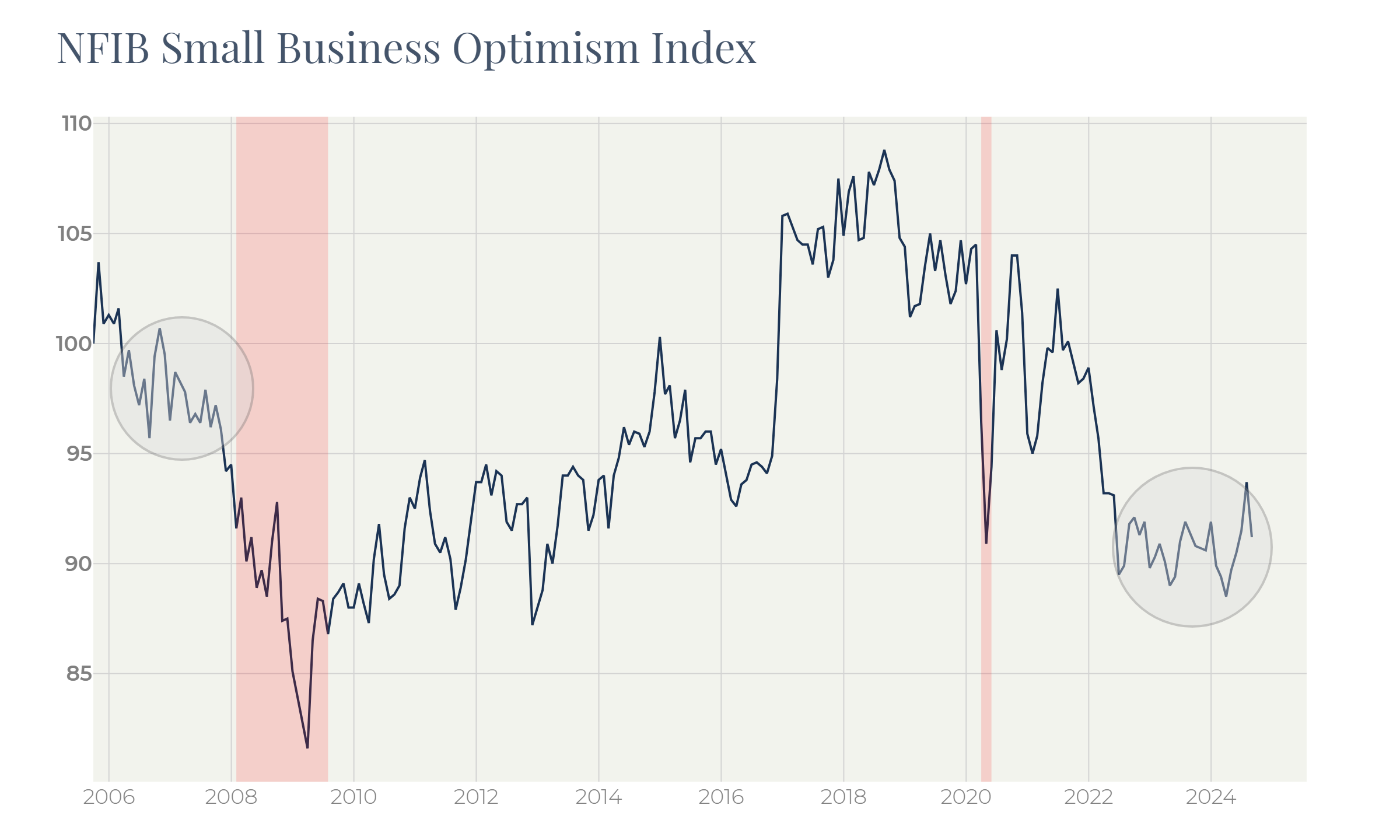

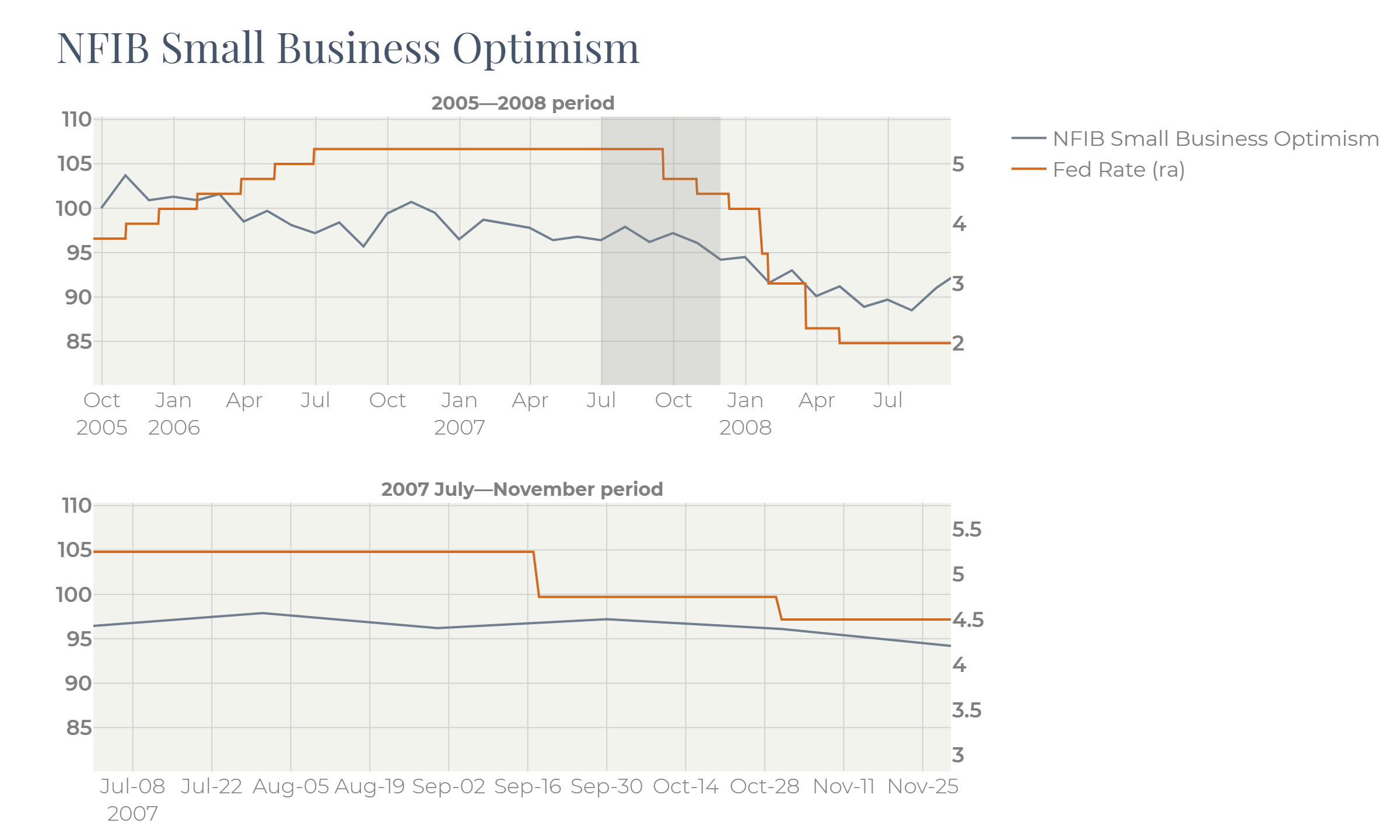

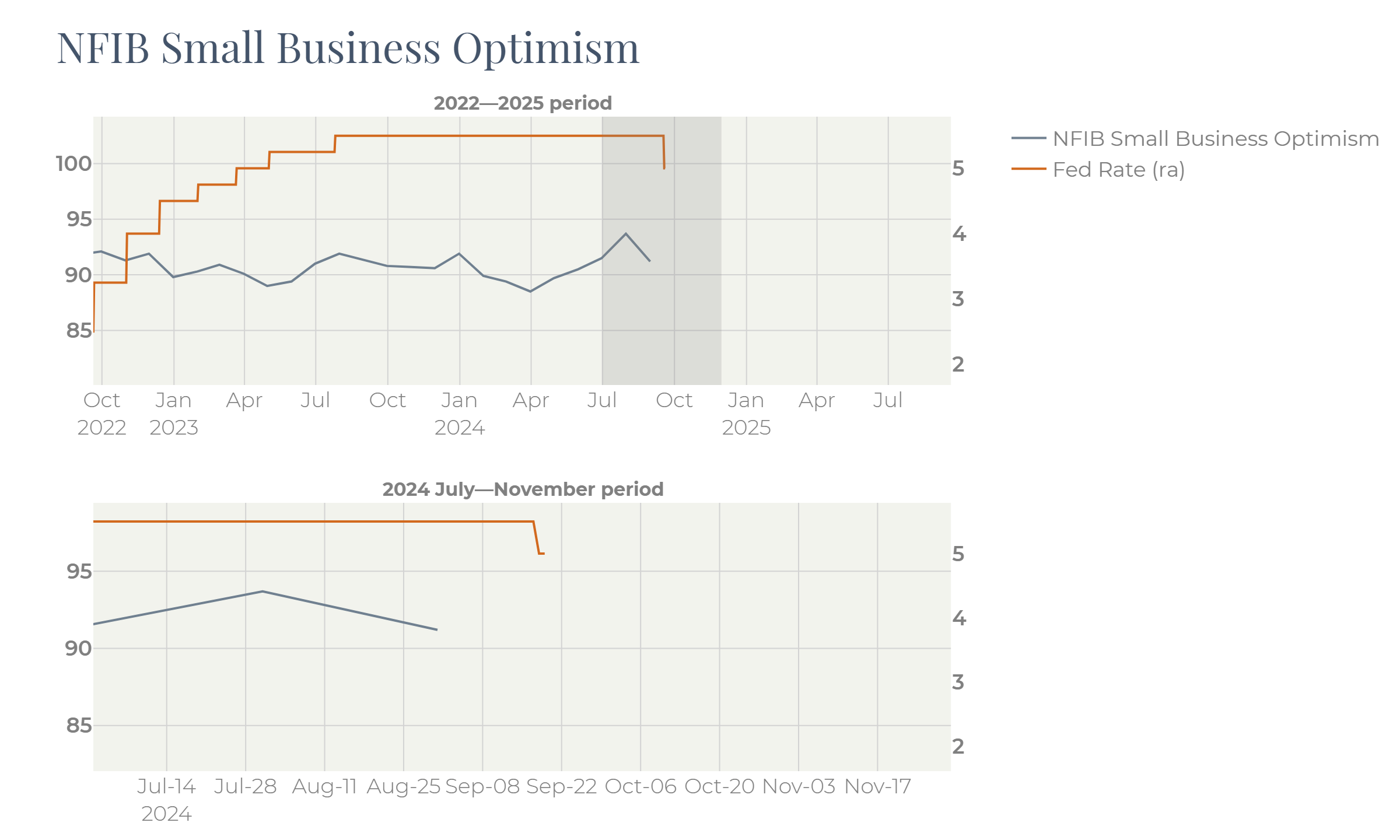

Small Business Optimism was fluctuating on a low level and did not signal neither rebound nor further sliding down:

Despite all the differences between the 2007 and 2024 patterns there are more similarities than one can think.

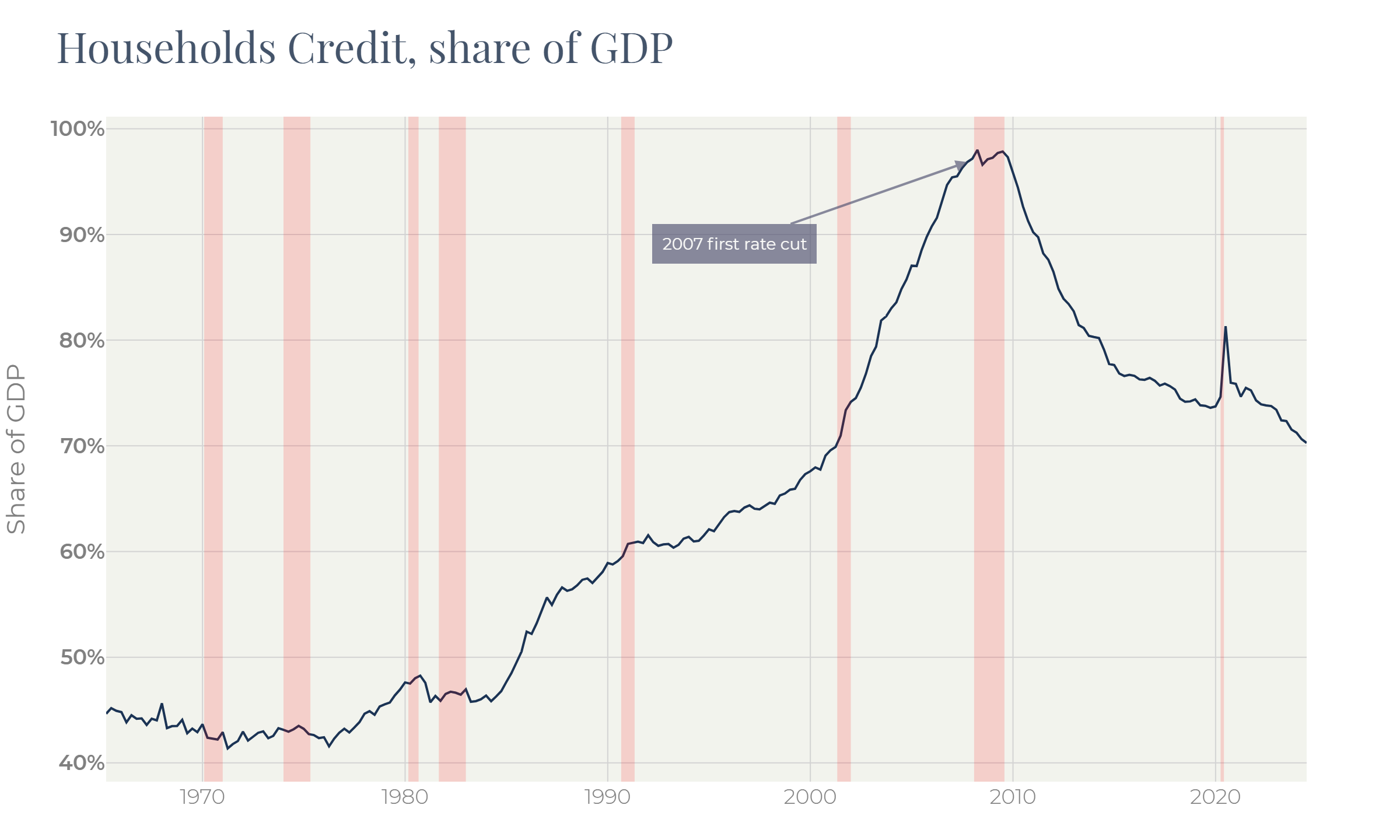

The 2007 crisis was a result of adaptation of the US economy to the significant consumer extra demand caused by the surge of the household’s credit:

The uptrend in the household’s credit could not last forever. In 2006 the US financial authorities began tightening loan requirements to avoid uncontrollable credit expansion. Thus, one source of consumer demand disappeared, this first affected the labor market and then pushed the economy into a recession.

So, the major issue was in the liability side of households’ balance sheet.

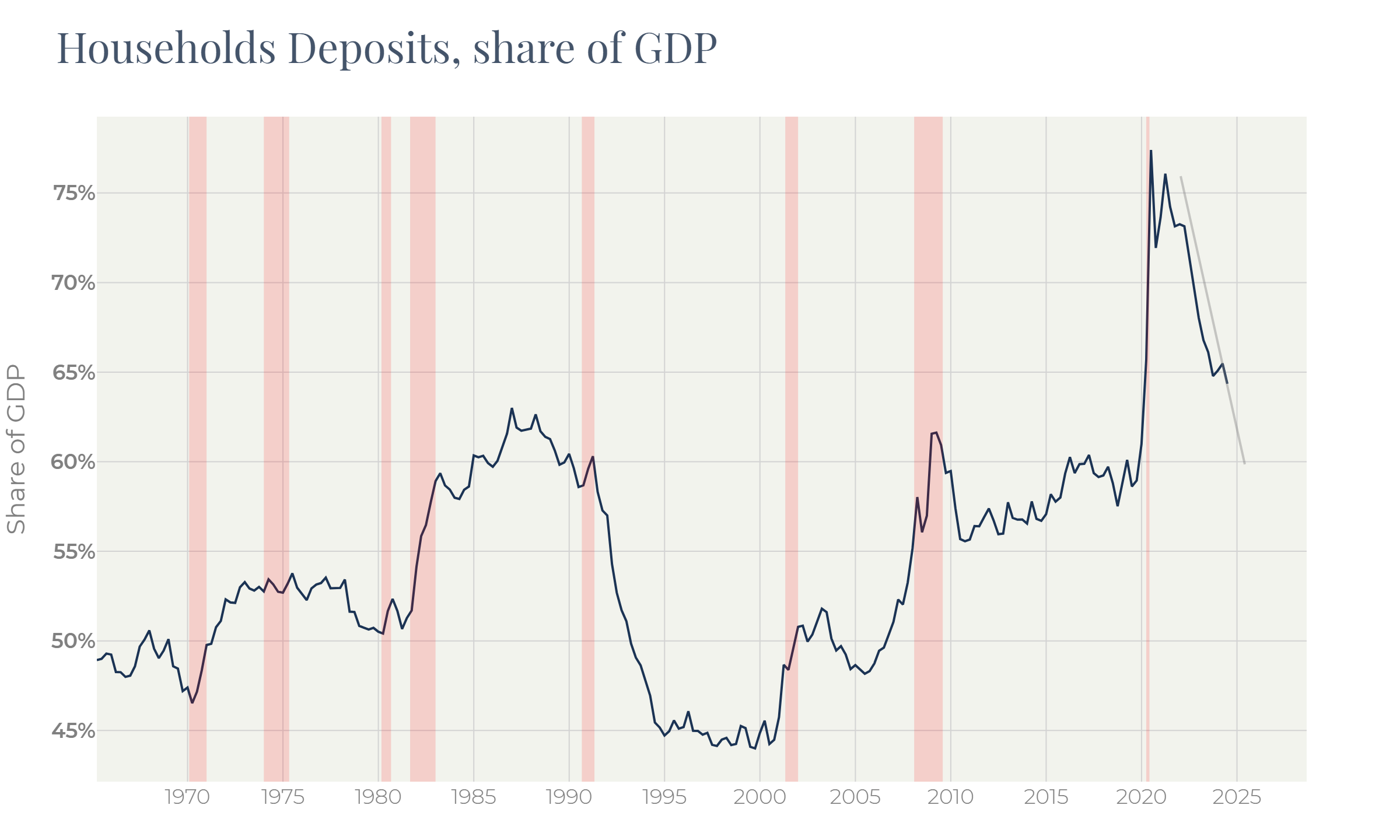

Now the major issue is in the assets side of households’ balance sheet. The massive anti-pandemic monetary issuance pushed households’ deposits up:

Now consumers do not need to take loans: they have money in their wallets already. Just like it was in 2007, it results in extra spending and a historically low savings rate. Like in 2007, the source of consumer funds is not unlimited. Based on the above figure, we have come close to the finish by now.

Summary

In both 2007 and 2024, the major risk to the U.S. economy was that the source of extra spending had reached its natural limits. In both years, the Fed decided to cut the key rate by more than expected. This decision aimed to offset the loss of extra demand in both cases. In this review, we show that the labor market was the first to be affected, while many other macroeconomic indicators did not signal alarm. We focus on Industrial Production, Durable Goods Orders, Consumer Sentiment, and Personal Savings. These figures reflect the strength of consumer demand but lagged in 2007. While we're not concluding that the 2007 pattern will repeat, ignoring it could be a serious mistake in the current situation.