The high-rate environment in theory should negatively affect the construction sector. Over the past two years we have observed the opposite picture: record housing starts, rocketing employment in the sector and house prices growing faster than inflation. Shelter inflation became a headache for the Fed being stubbornly high since 2021. However, this situation reflects sooner consequence of the surge in demand for houses in 2021 on the back of low rates and demand for rent on the back of excess in personal savings. This environment is under risk of oversupply of new houses started one—two years ago, impact from restrictive rates and gradually evaporating excessive savings.

Construction volumes and prices

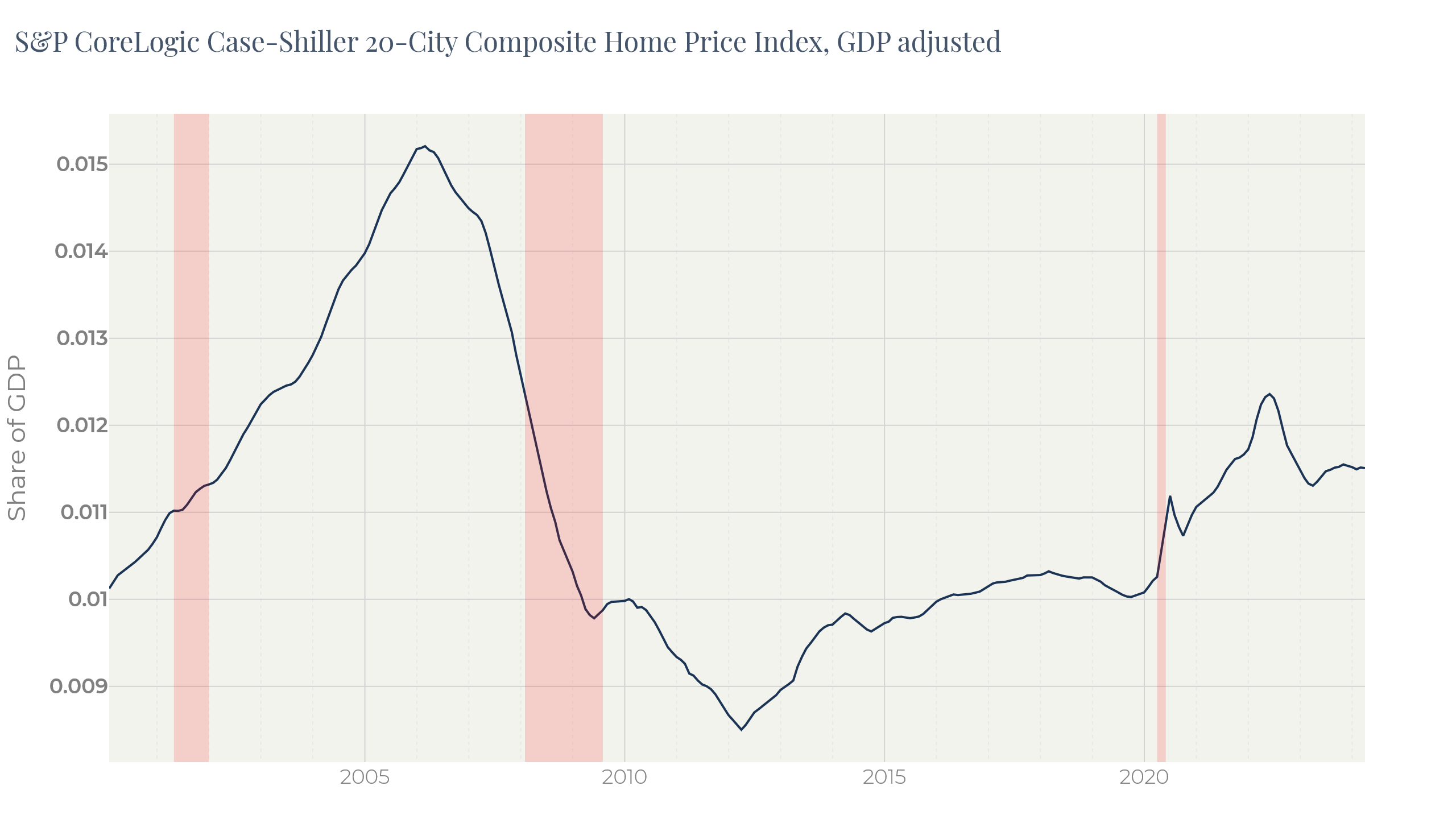

Figure 1

The factors that pushed house prices up are well known. These are low mortgage rates in 2020—2022, intention to invest in inflation-protecting assets on the back of record money issuance since WWII and supply chain disruptions accompanied by various pandemic restrictions, on the other hand.

As Figure 1 shows, house prices have grown 11% more than the GDP by now making a new house to be less affordable than before the pandemic.

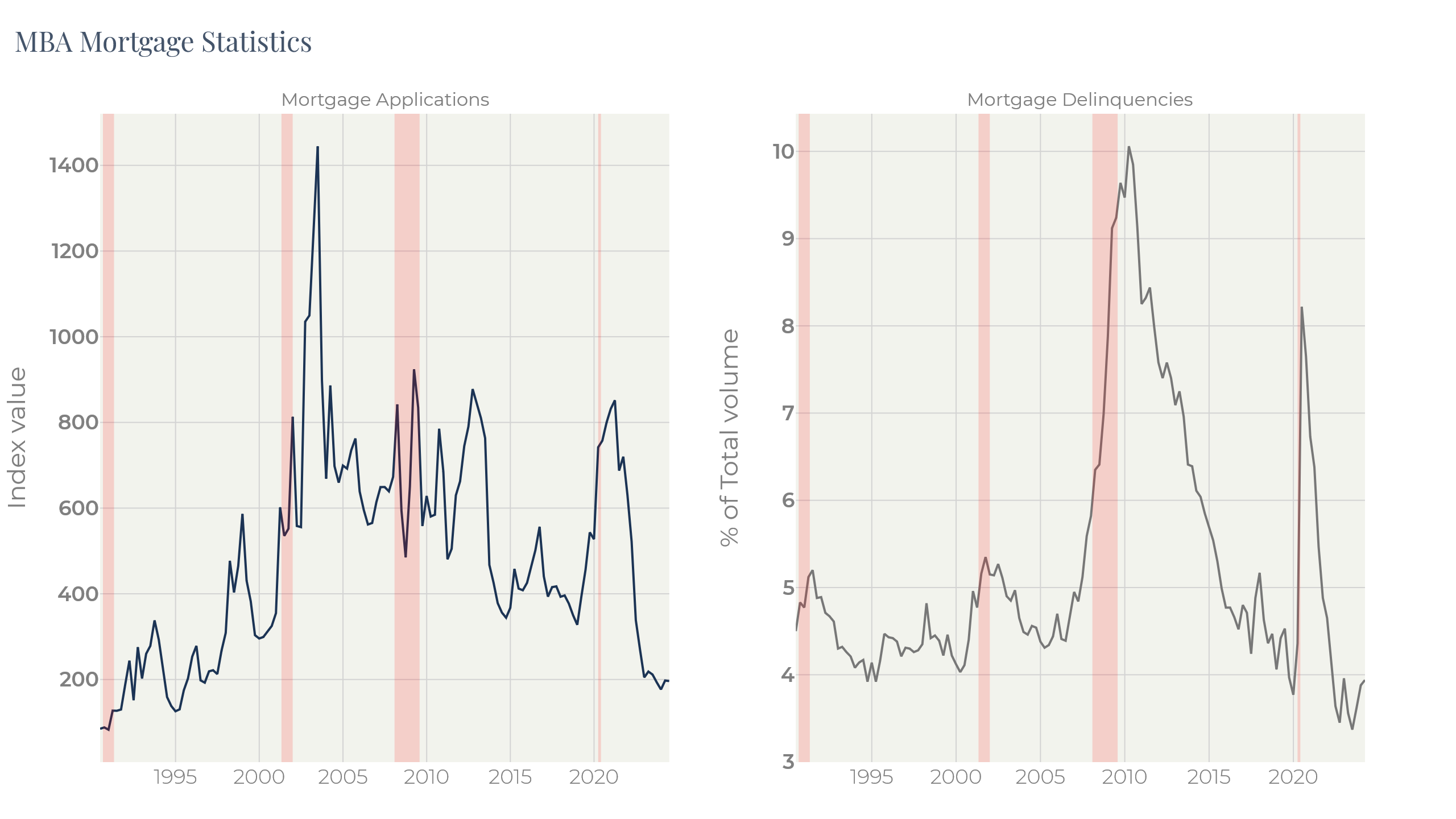

The start for this price move did happen even before the pandemic: the Federal Reserve lowered the key rate three times in H2 2019. This pushed Mortgage Applications up (Figure 2). During the pandemic a lot of mortgage loans were restructured so that low rates were fixed for long periods: the majority of mortgage loans in the US are fixed.

Fixed low rates and high wage inflation significantly improved balance sheets of households. This explains low rate of defaults in this segment:

Figure 2

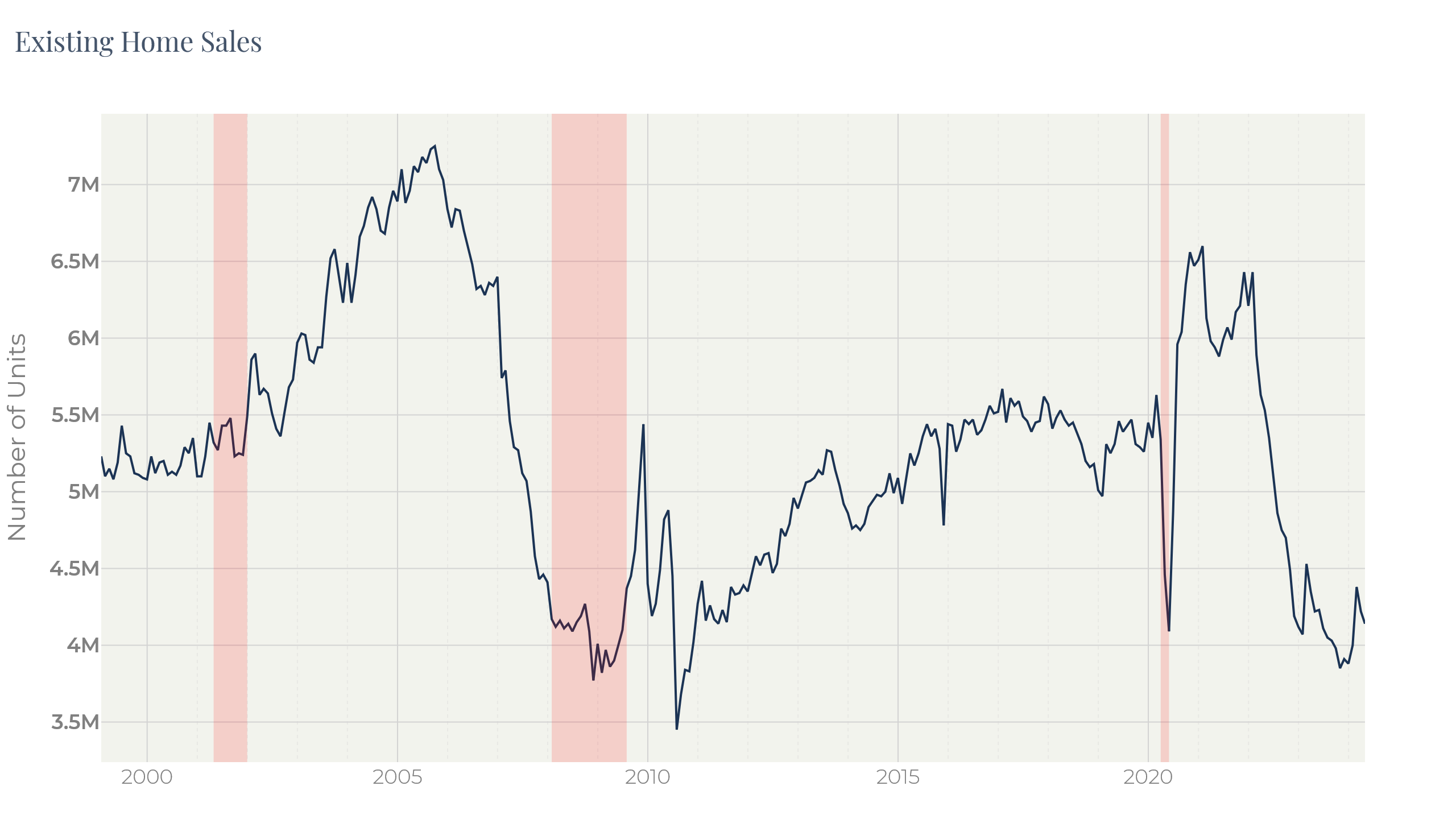

The frenzy in the real estate market lasted until 2022 Q1 when the Fed’s Chair Powell announced tightening of monetary policy. The mortgage applications plummeted, so did existing home sales:

Figure 3

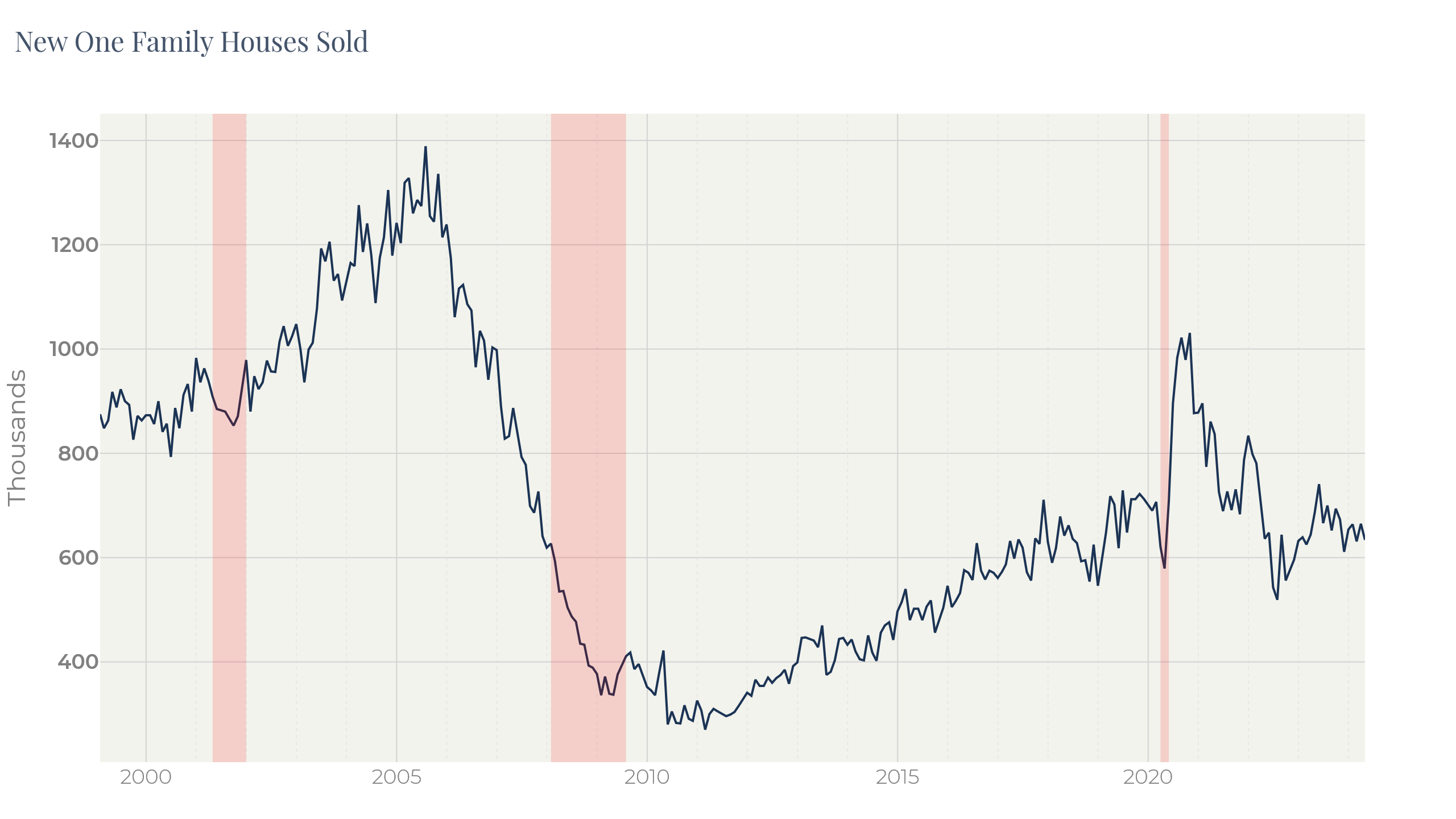

New home sales also fell, but less dramatically reflecting reluctance to give price discounts which is so typical of individuals’ behavior in the secondary market:

Figure 4

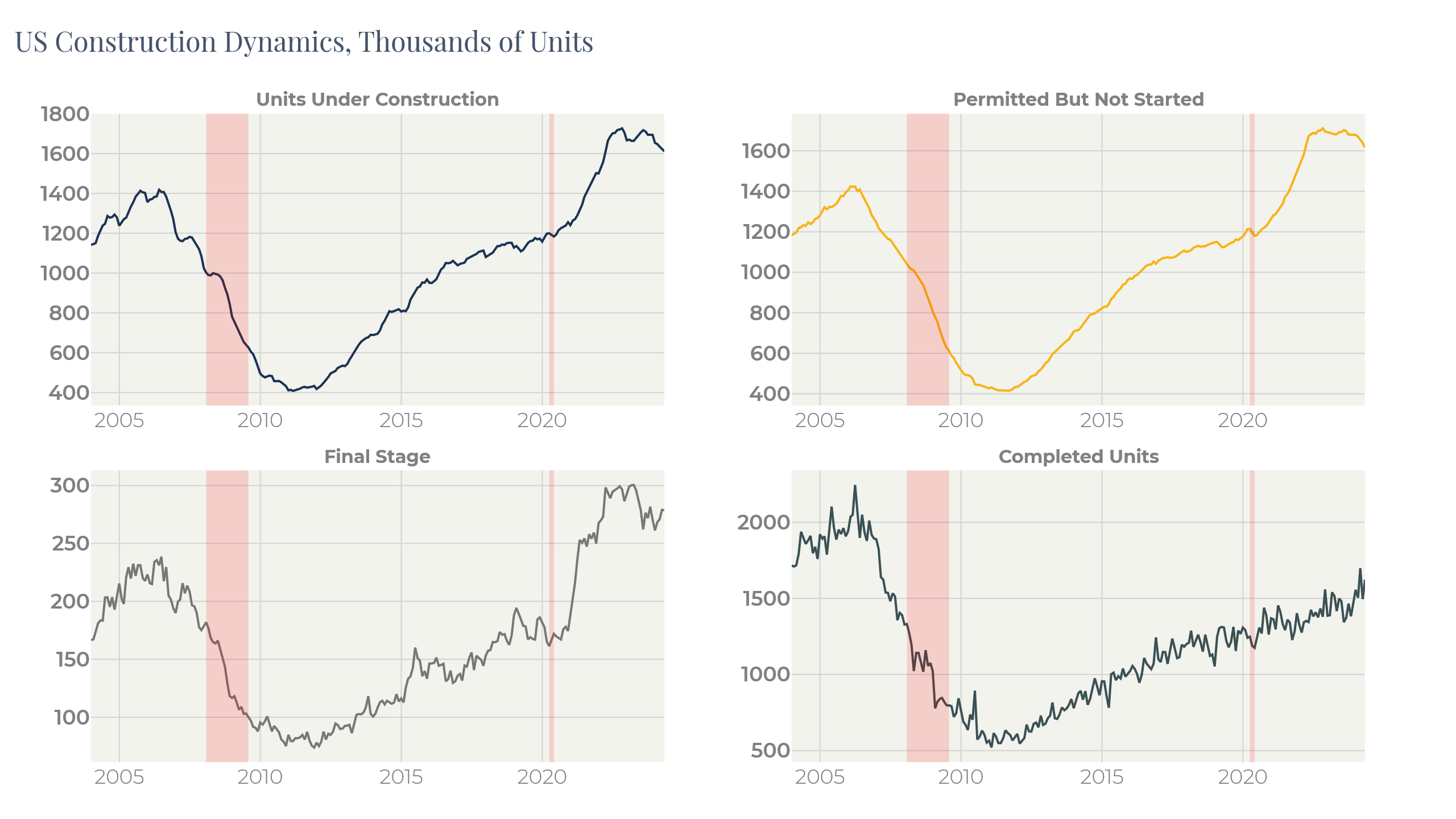

Figure 5 demonstrates the activity of the US developers after the anti-pandemic stimulus:

Figure 5

Construction volumes rocketed to record levels, quickly beating the previous 2007 high. Completed units, though, just started to grow, mirroring the natural lag between permissions and completions.

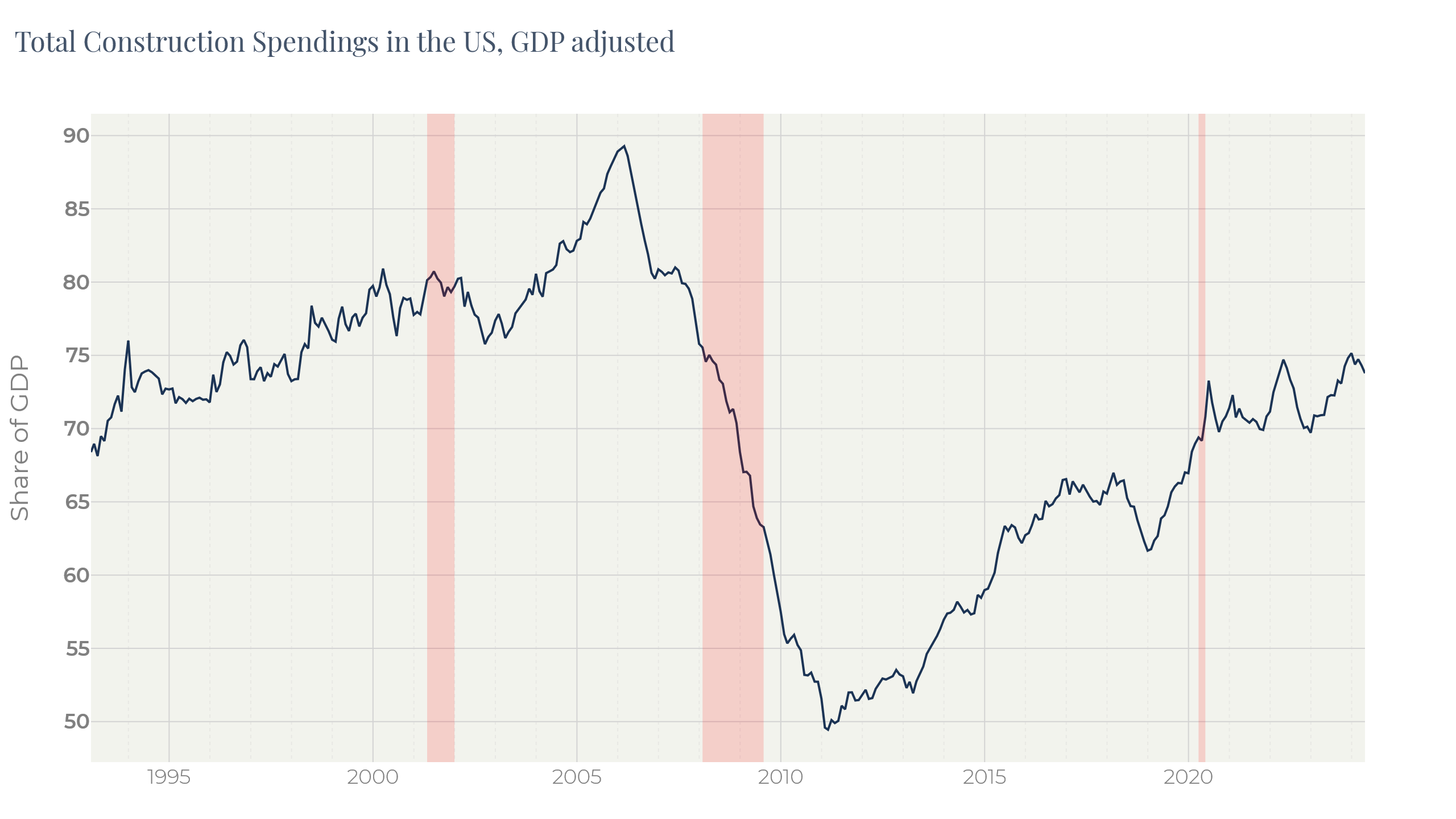

Rising completions together with the inflated prices resulted in total constructions spendings reaching the level of 2008 in terms of share of GDP:

Figure 6

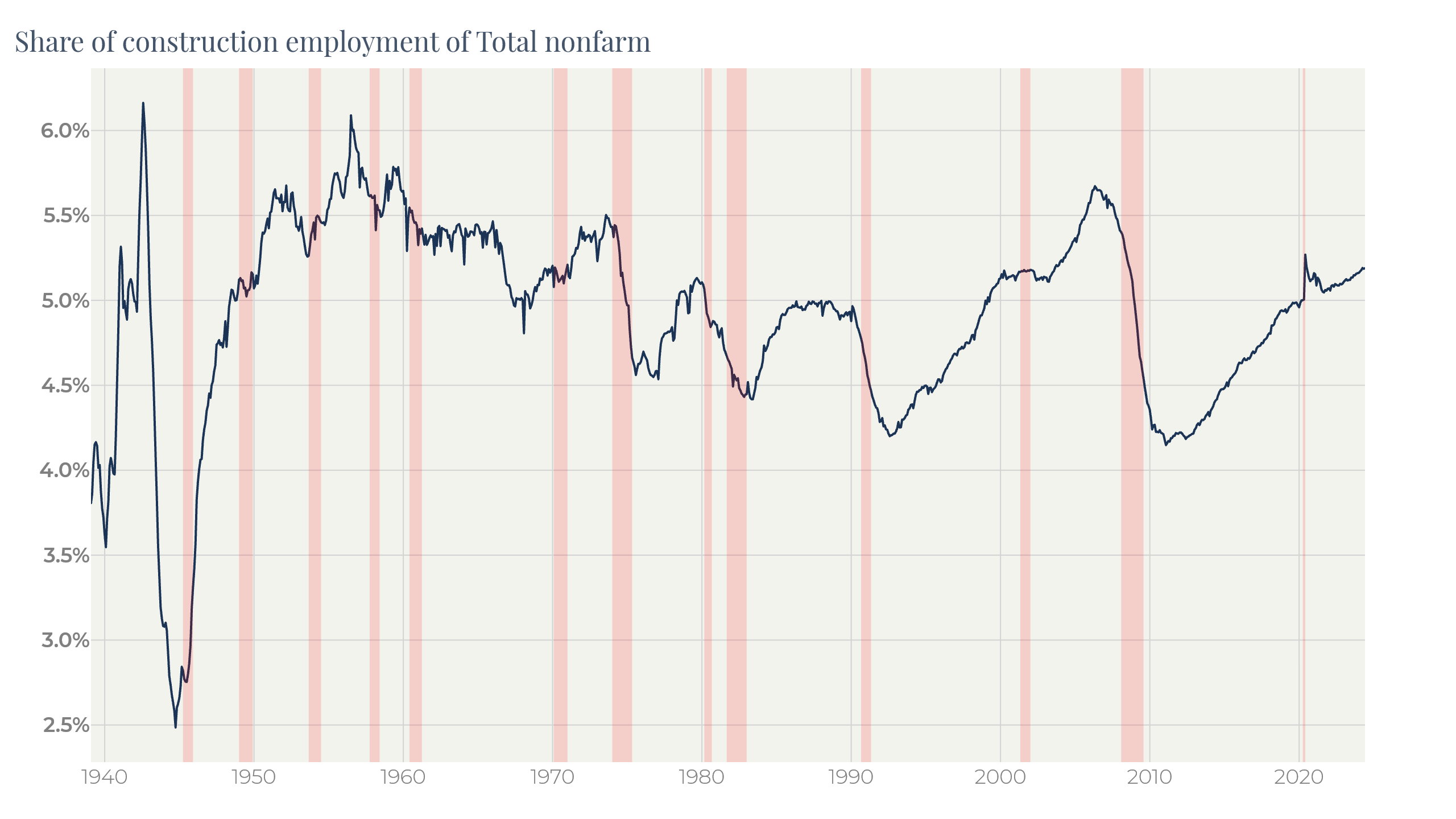

Share of construction employment has reached level typical of pre-GFC period:

Figure 7

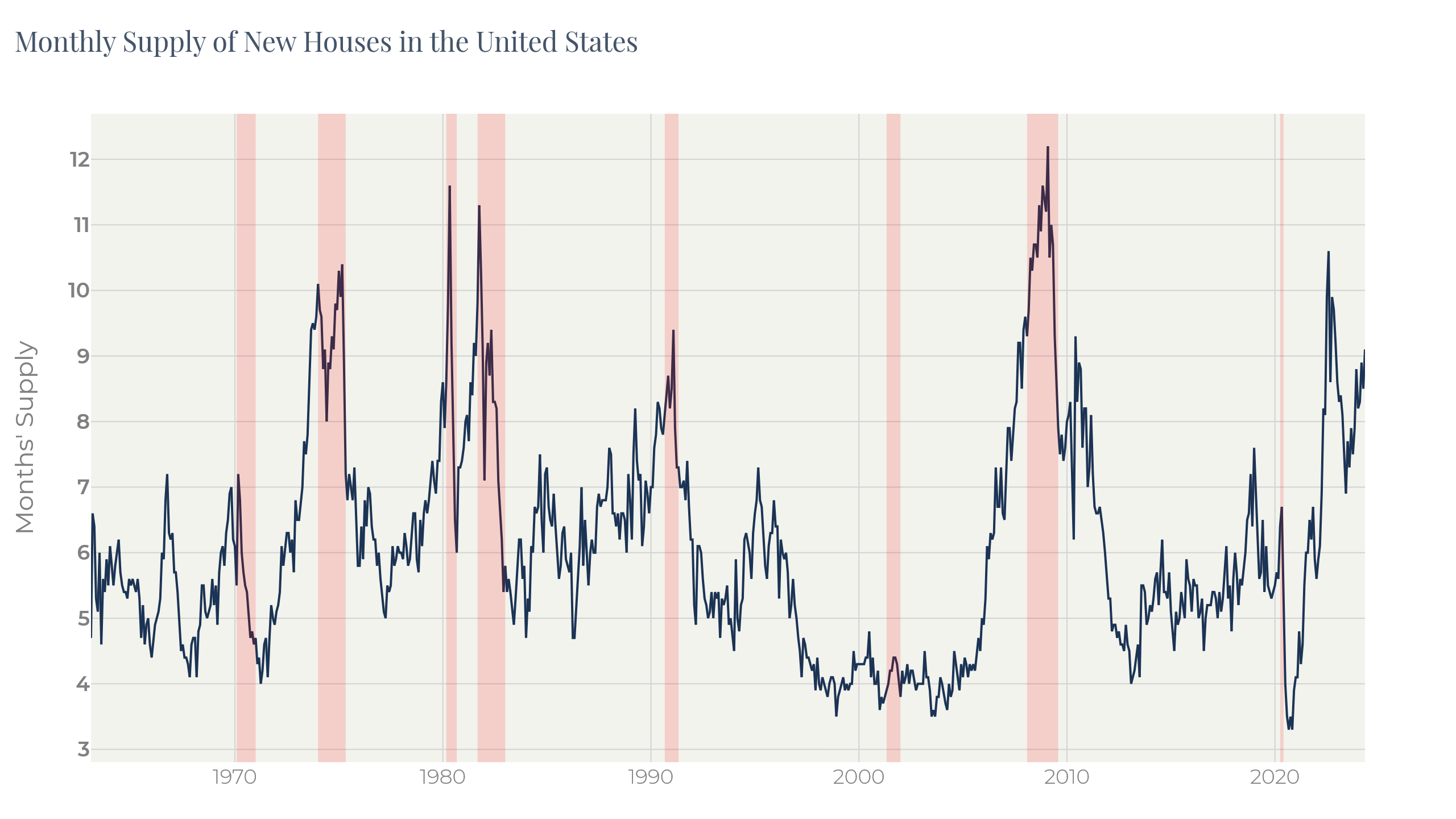

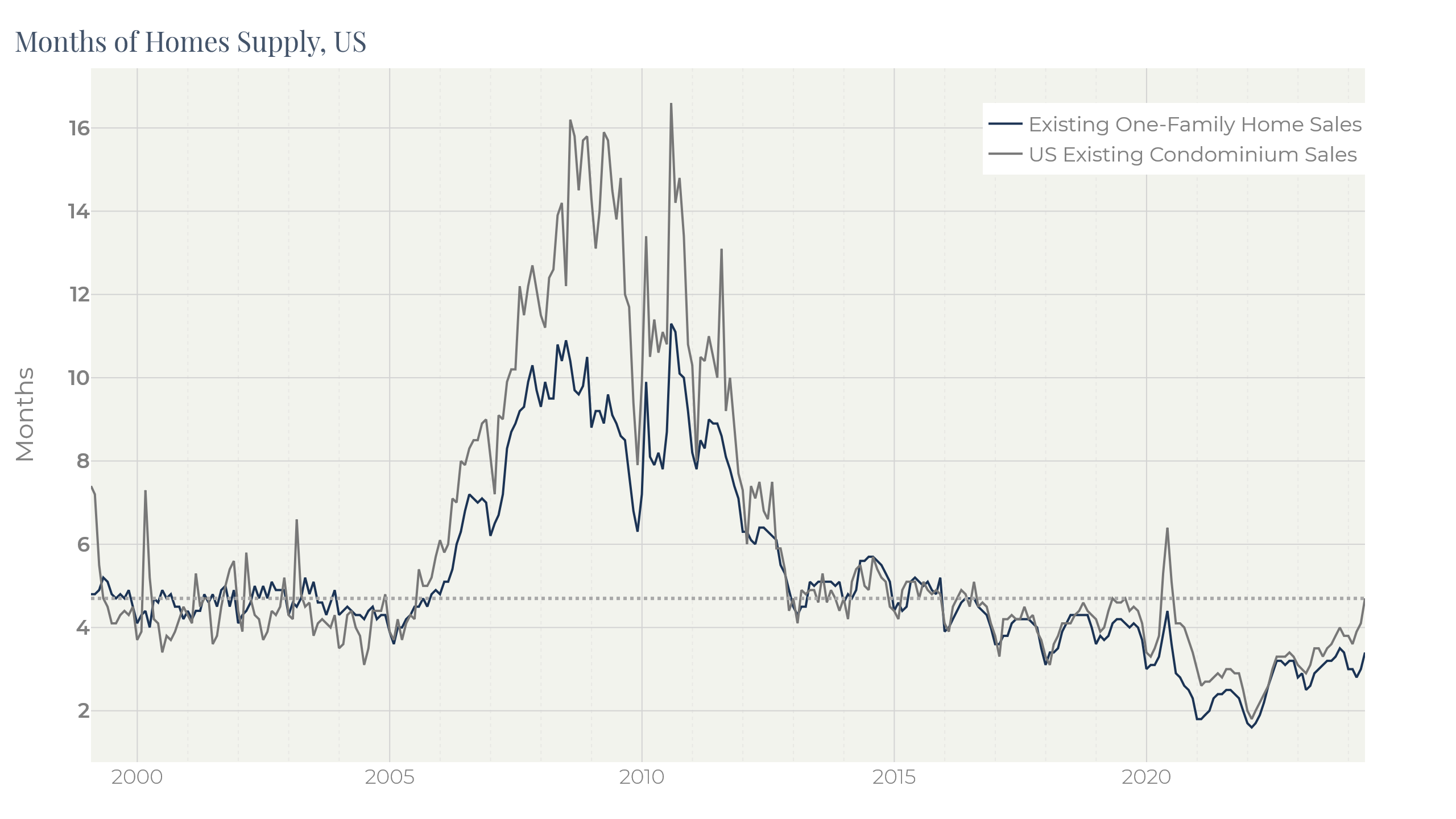

Rising completions and dimmed demand are creating an overhang of new houses, albeit quite low after sharp fall in housing inventories in 2021. Figure 8 displays the Monthly Supply of New Houses calculated by the U.S. Census Bureau as the ratio of houses for sale to houses sold:

Figure 8

Figure 9

The existing homes supply is also growing, especially in the Condominium segment. The high-rate environment accompanied by high corporate profits is very good for wealthy ones who can afford a detached house without taking a loan. By contrast, for those renting apartments or buying them with the loan leverage, the situation has become worse. It is not a surprise, therefore, that the multifamily segment is more sensitive to high rates (Figure 9, Figure 4, Figure 3).

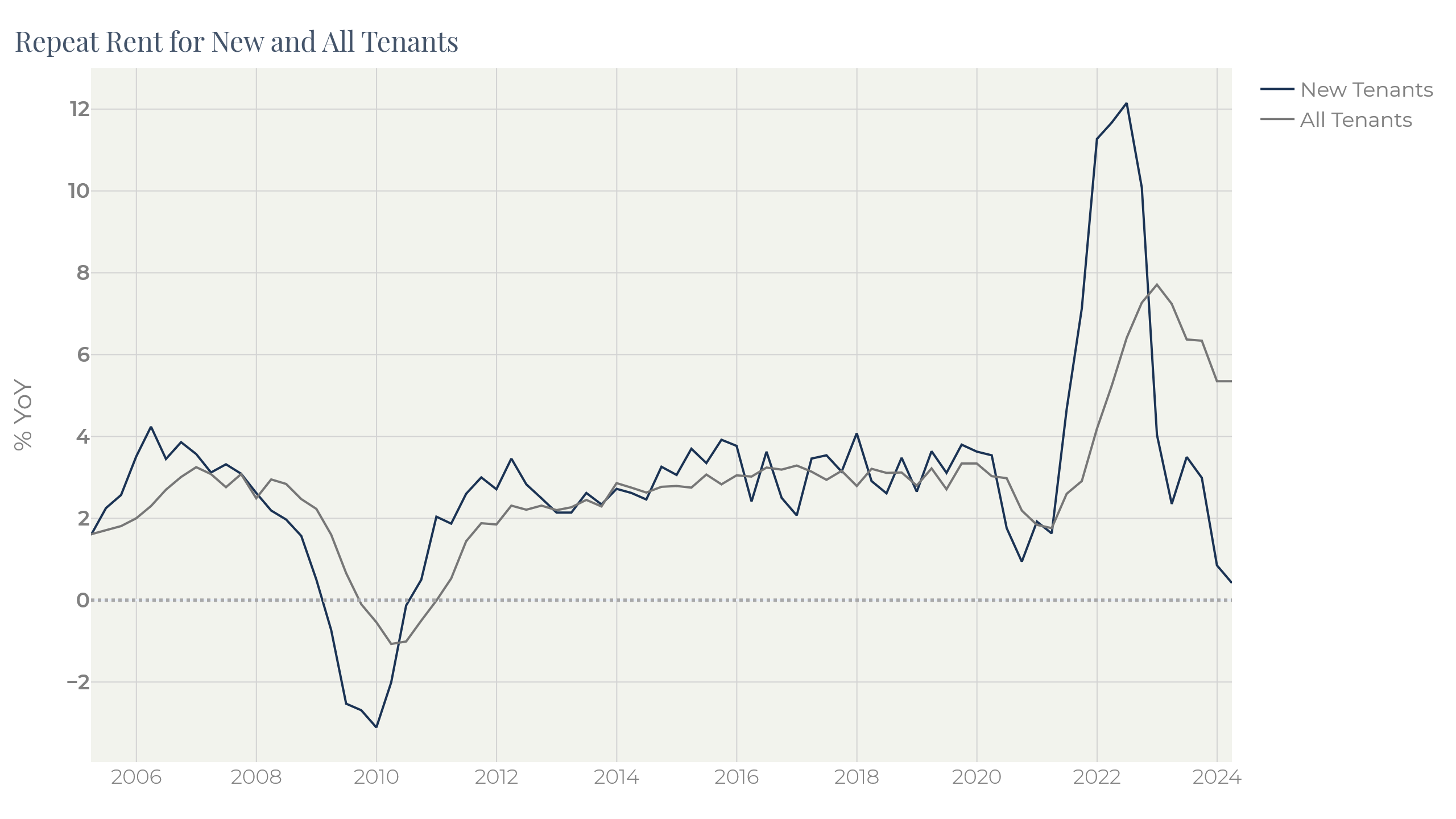

Lower-income individuals, though, became beneficiaries of the pandemic monetary emission through direct payments and the super-hot labor market in this segment. They accelerated the shelter market with their excessive savings. Q1 2024, though, presented a surprising slack in consumer demand which became pickier than earlier. Most probably, this is caused by melting savings, although this hypothesis yet needs to be verified.

In any case, we already can observe a sudden stop in new rents growth with prolongations being still above 5% (Figure 10):

Figure 10

Prolongations are stickier by nature, but this chart also signals that the COVID-19 extra savings are likely coming to an end.

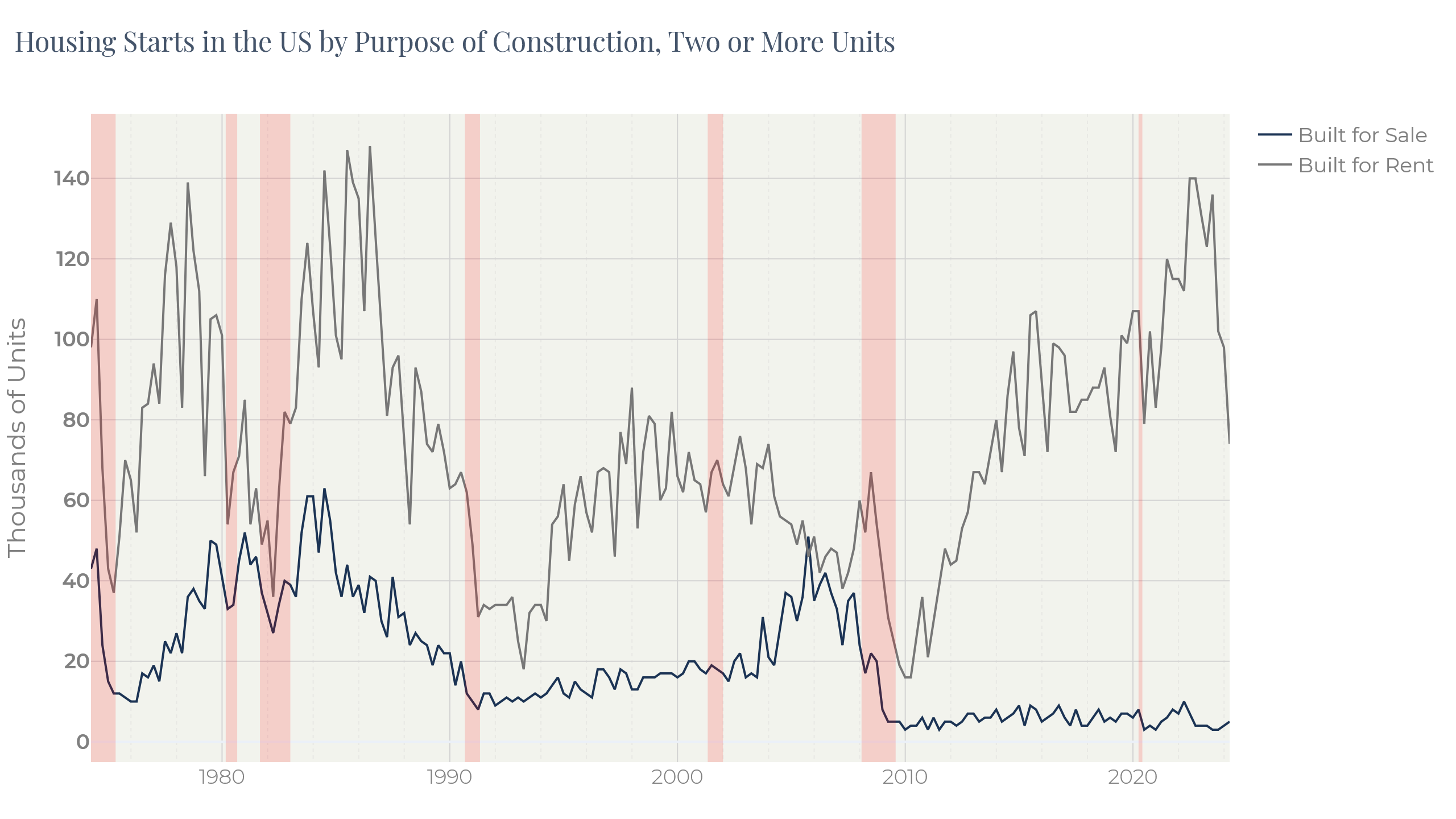

Developers reacted to this demand weakness sharply decreased construction of units built for rent (Figure 11):

Figure 11

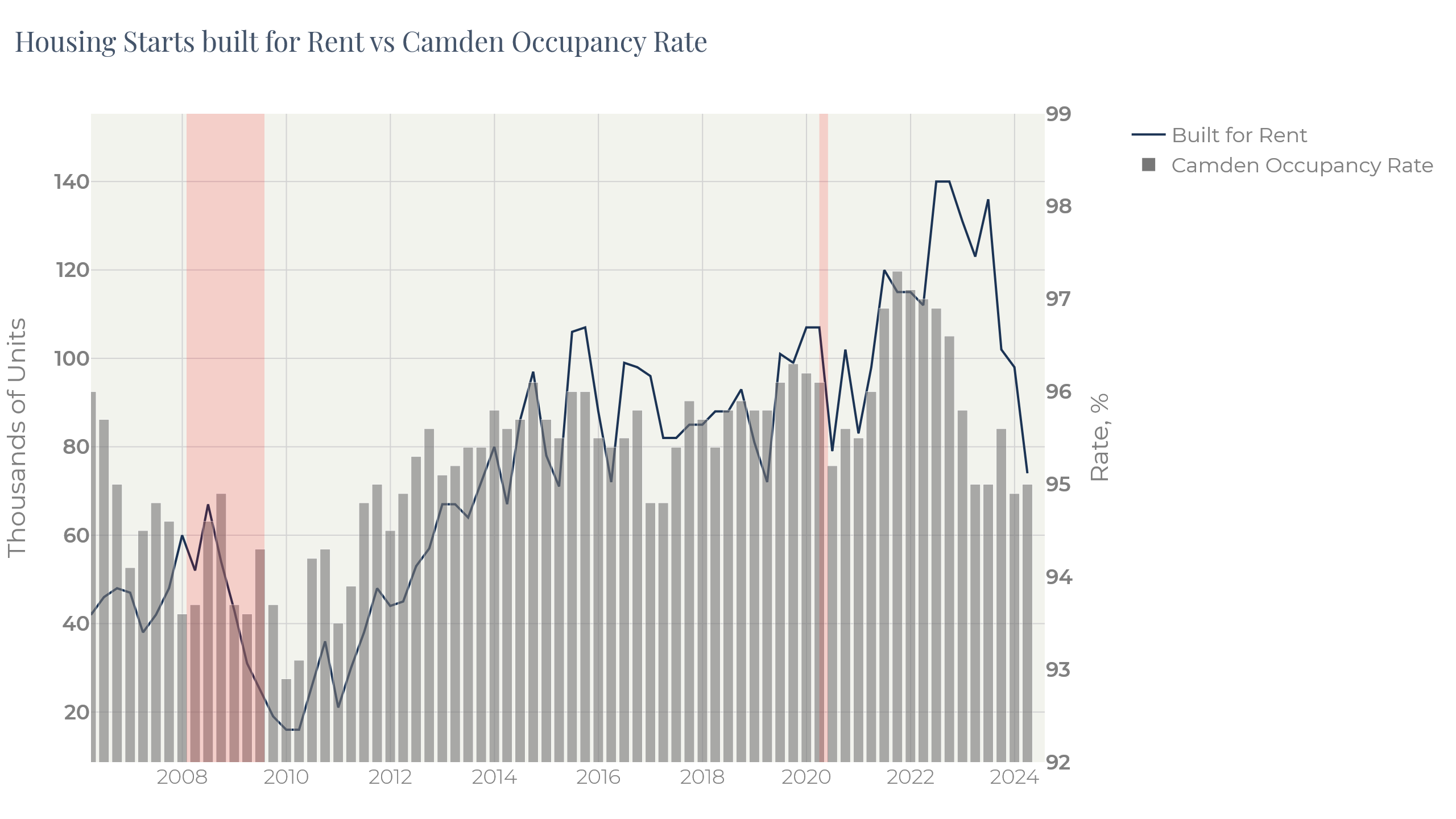

Weak consumer demand was highlighted by one of the largest US REITs Camden on their investors conference call on 2024 Q1 results:

Some delinquent renters did repay past due amounts, but more often, we simply received the benefit of having our real estate back, the opportunity to commence a lease with a resident who abides by their rental contract, and lower bad debt from having a new resident who actually pays. The accelerated move-outs of delinquent residents did put pressure on our physical occupancy, so we made a pricing strategy shift during the quarter, reducing rental rates at communities less than 95% occupied in order to maximize pricing power as we entered our peak leasing season. As a result of this shift, we experienced higher occupancy during the quarter, but that was entirely offset by lower rental rates1 .

Figure 12

Building materials and construction companies

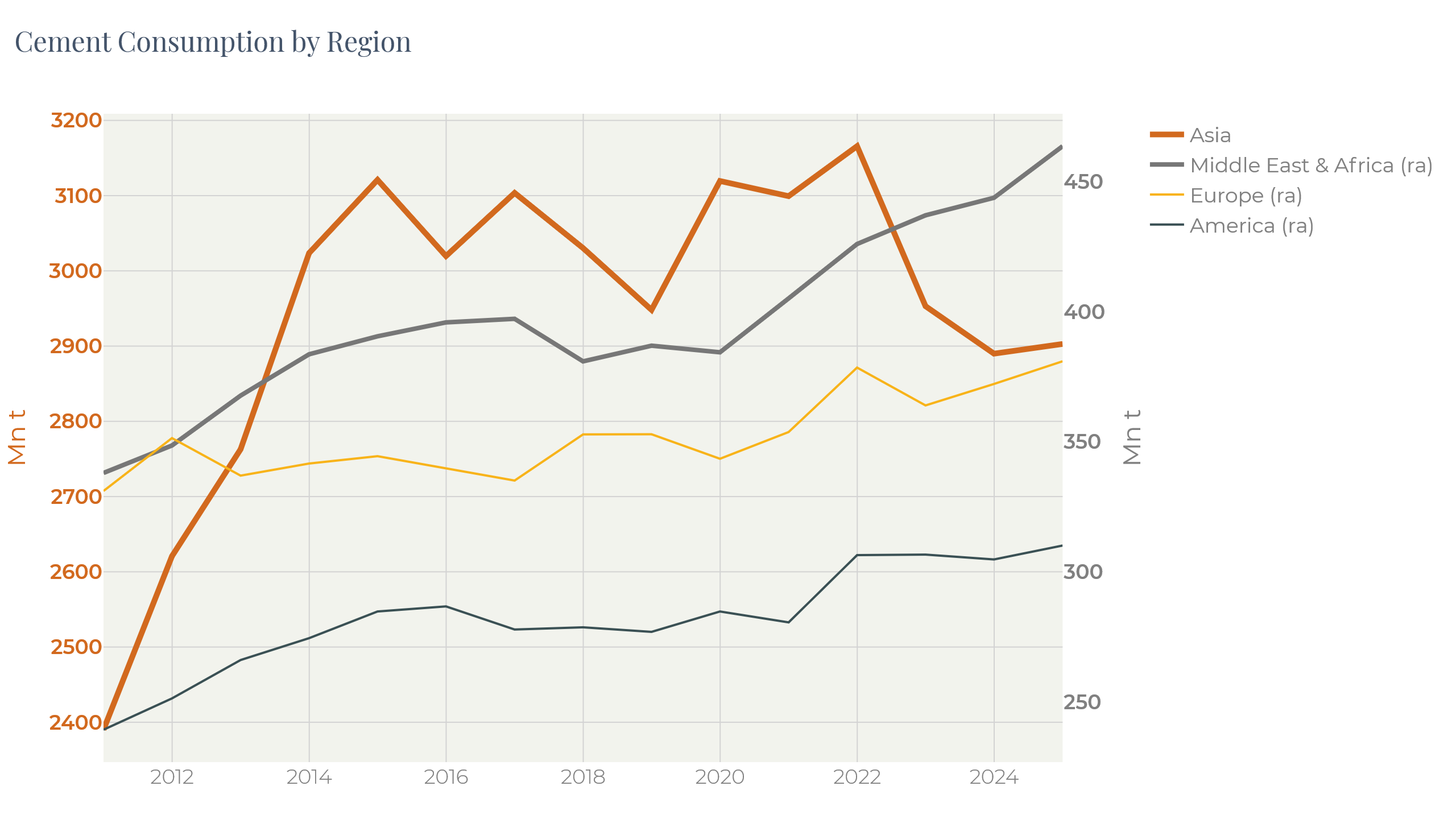

While the US having been experiencing a construction boom, the Asian market lead by China, soured. This resulted in weakening global demand for commodities linked to the construction market. For example, the reduction in cement consumption in the Asian market in 2022—2024 was circa 250Mn t which more than offset growth in other countries (Figure 13):

Figure 13

The property market slowdown in China is a result of the urbanization trend coming to its final stage. This heavily pressures local building material prices:

Figure 14

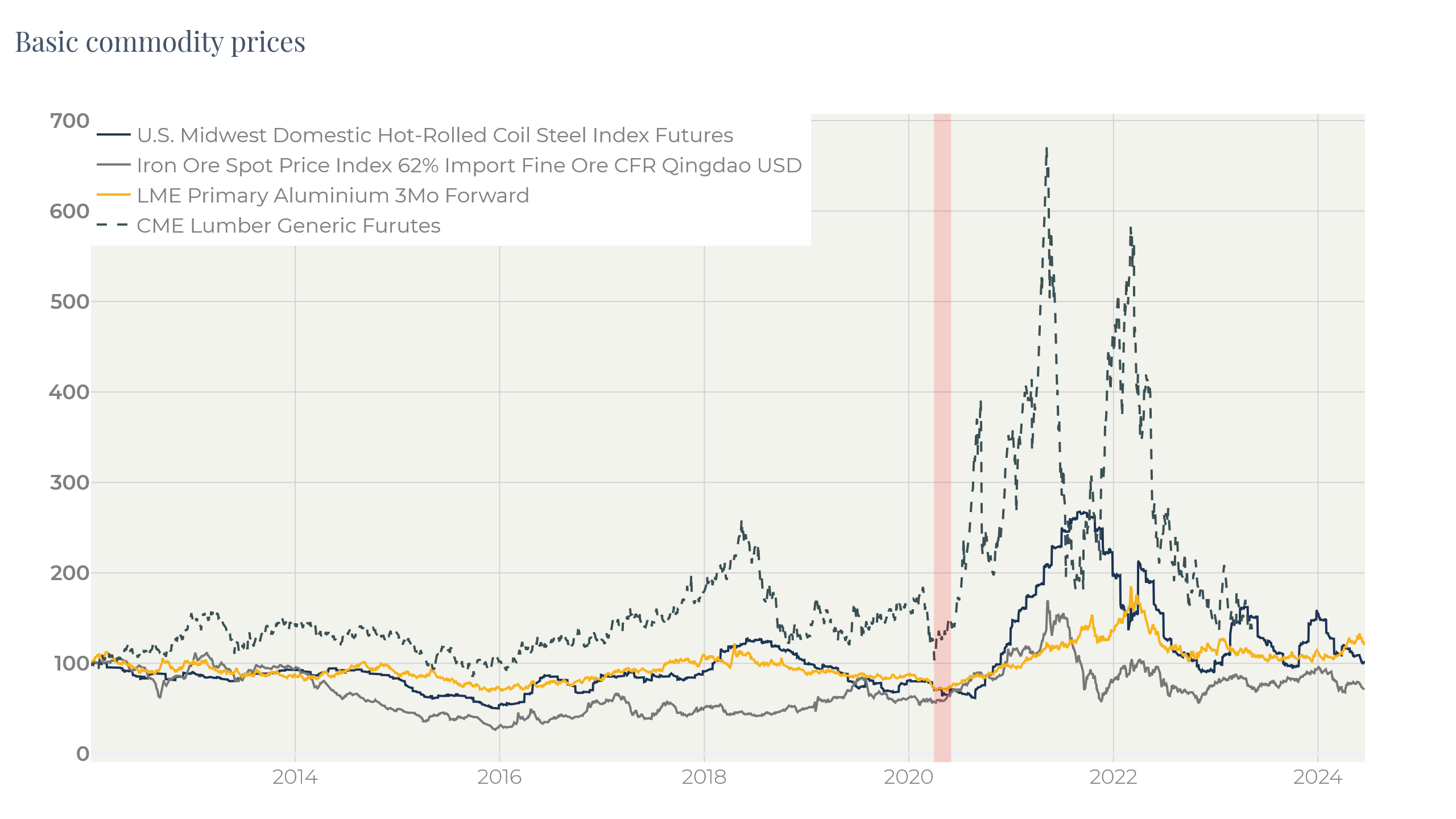

The huge size of the Chinese economy is sending base commodity prices down. Major commodities have returned to their pre-pandemic levels:

Figure 15

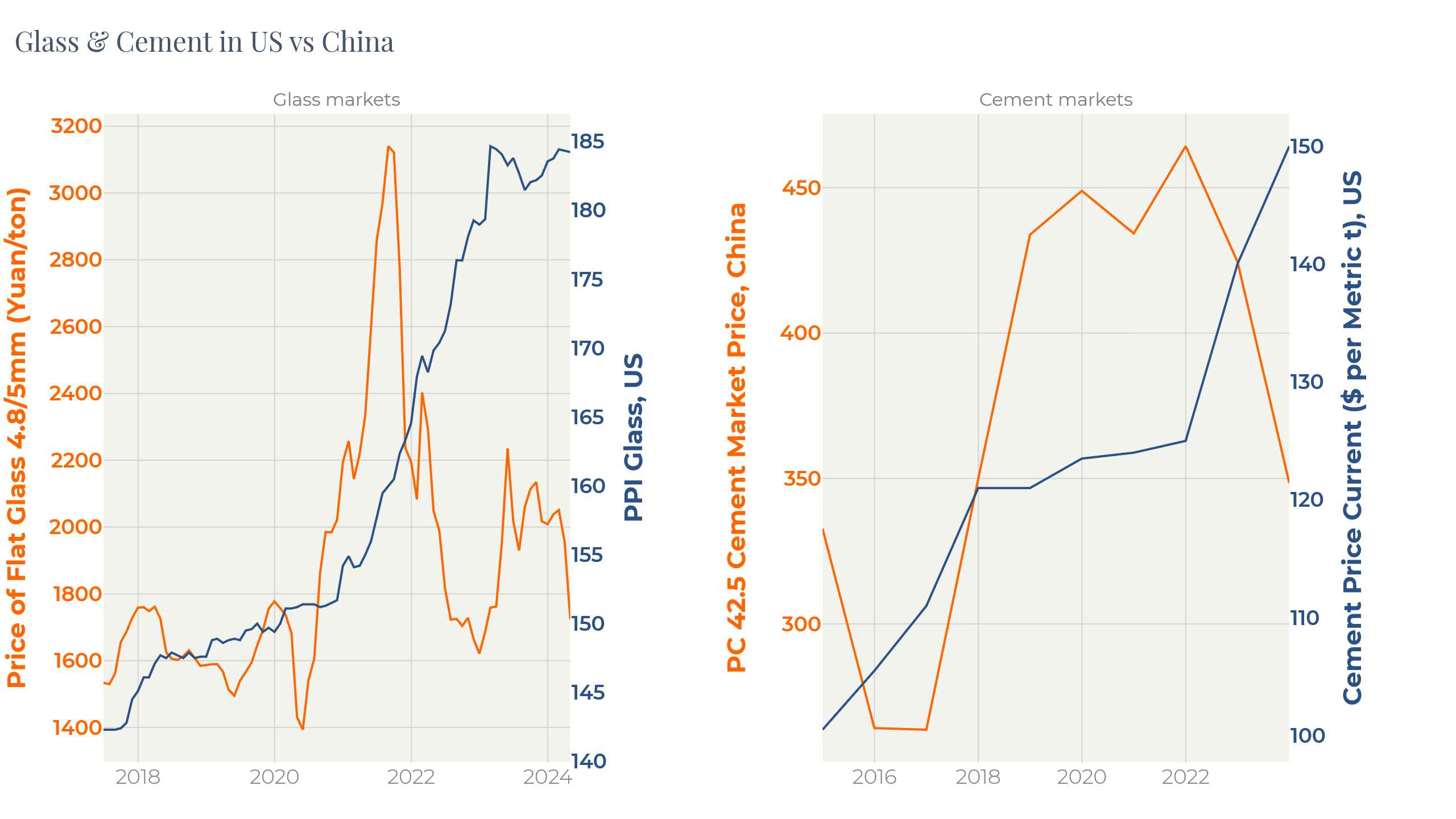

Construction material prices can behave differently in different countries because of the cost of transportation. So, construction materials in US look much better than their peers in China:

Figure 16

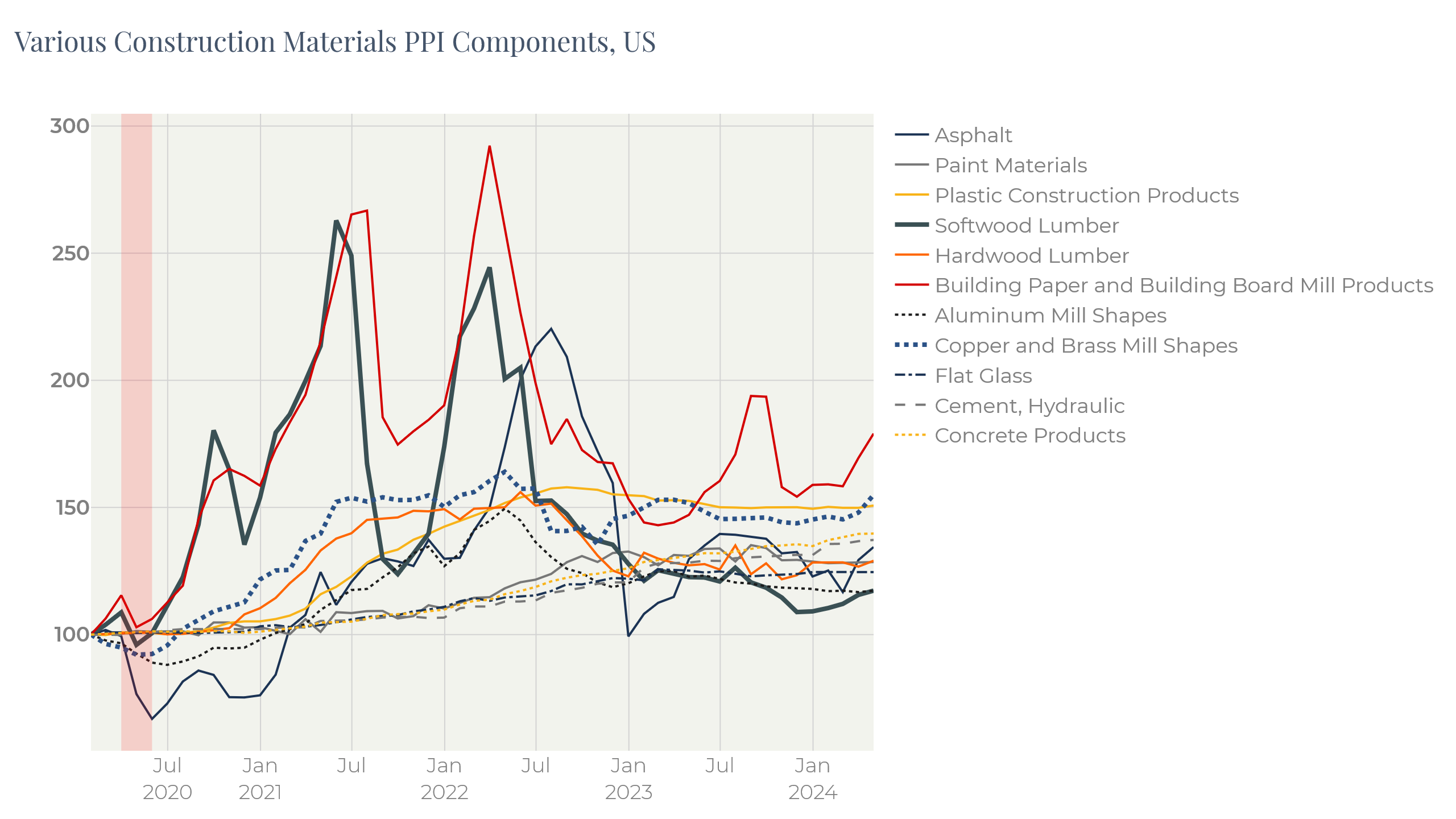

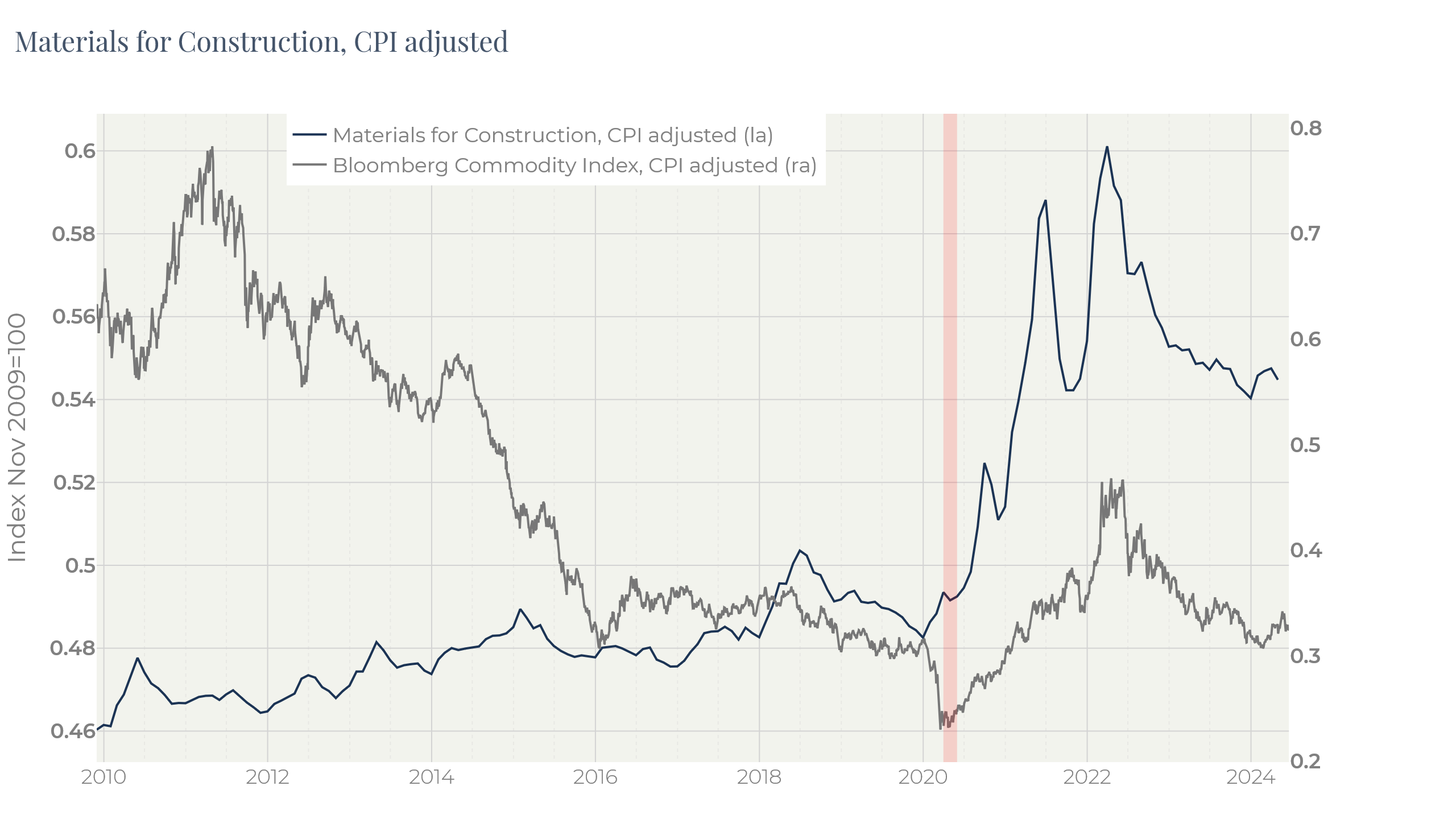

Hot US real estate market has sent construction materials prices well above the broad commodity index:

Figure 17

Selected stock names

The commodity market experiencing pressure from the slowdown in China on the one hand, and surged construction activity in the US on the other, created a favorable situation for corporations being able to take part of this gap. Different companies are sensitive to various stages of this construction cycle:

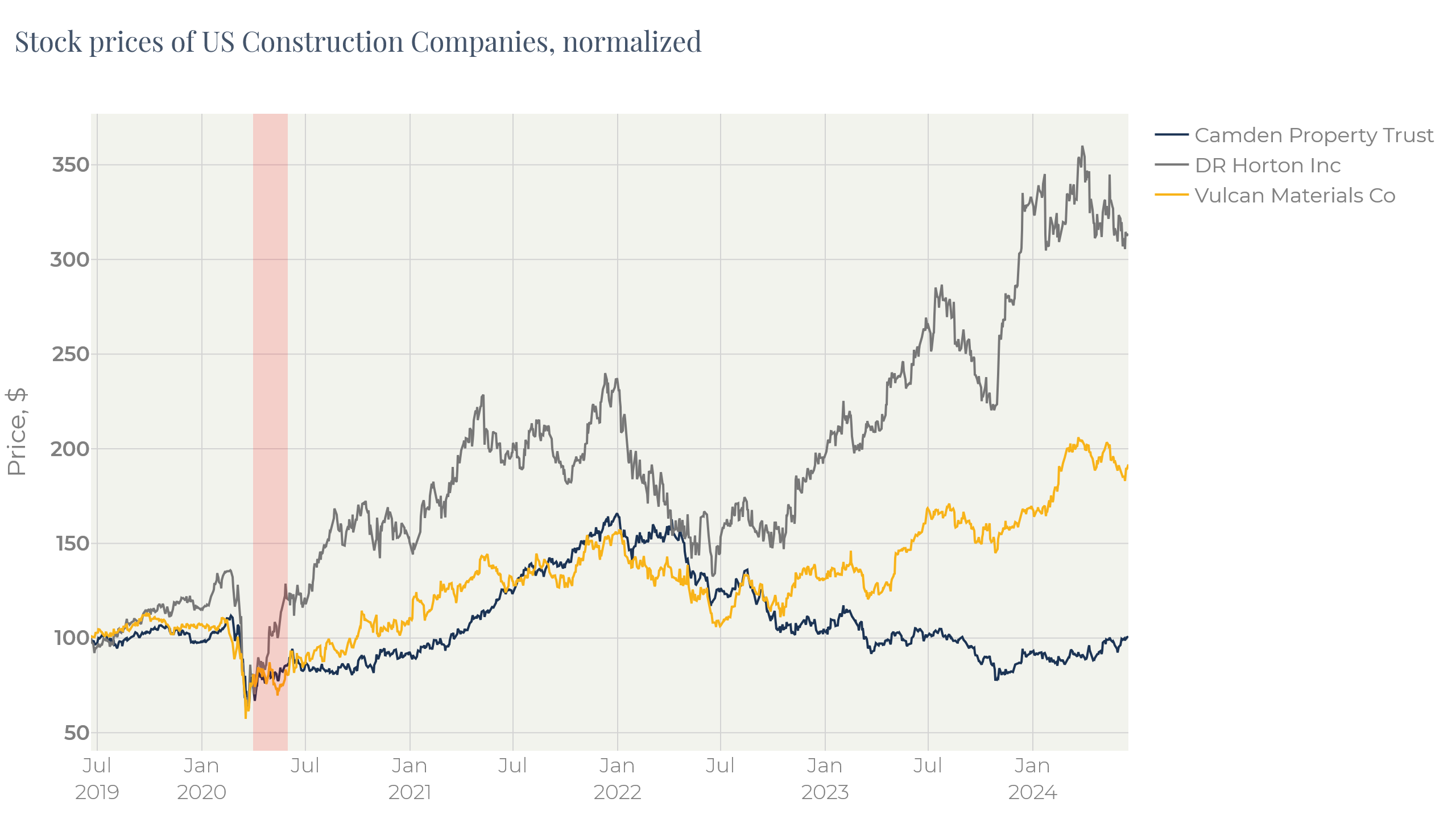

Figure 18

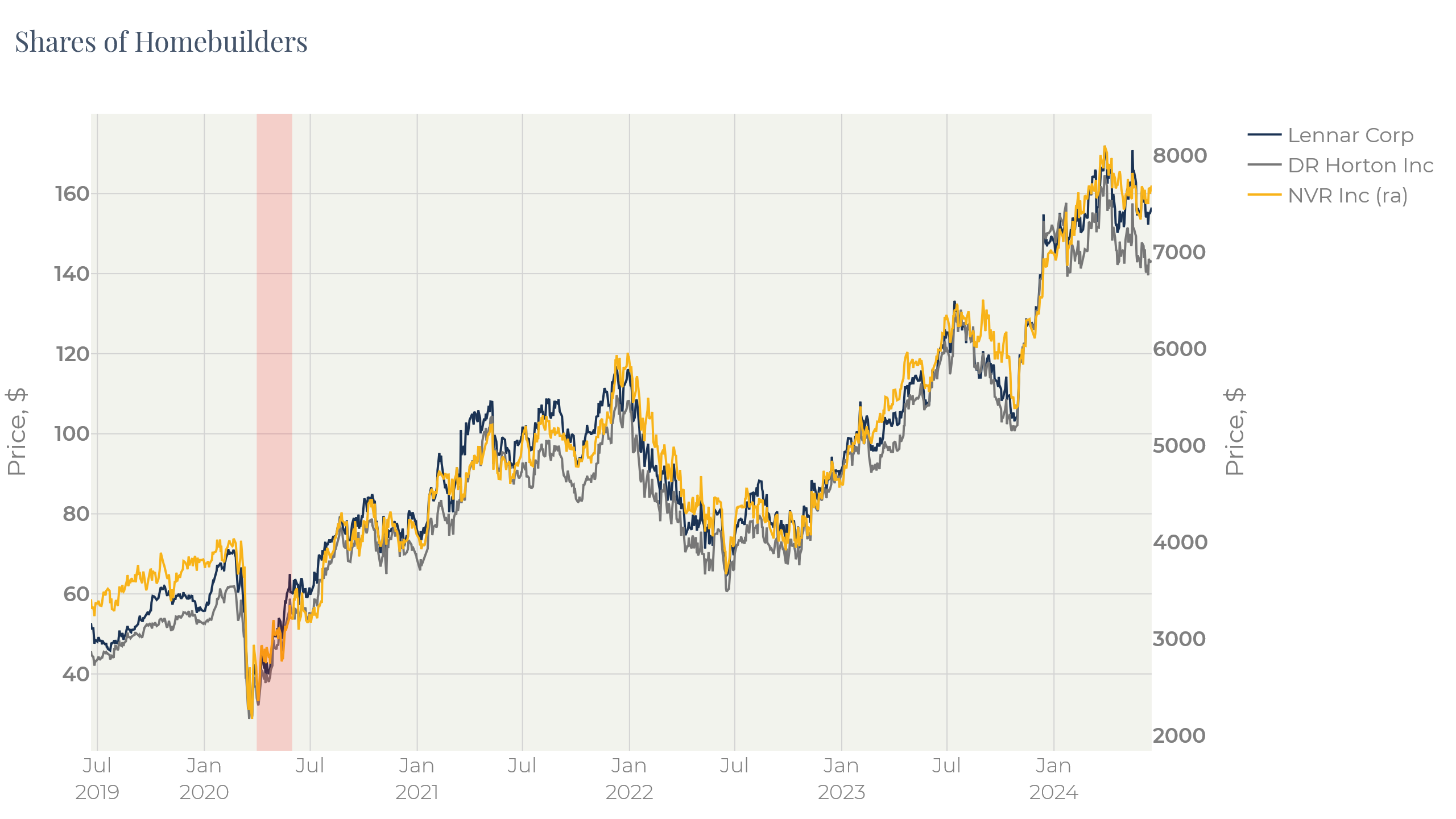

As one can see on Figure 18 DR Horton — one of the largest homebuilding companies in the US — is a winner of the stock price competition by far. Comparison to other homebuilders demonstrates that this price behavior is specific for the whole sector:

Figure 19

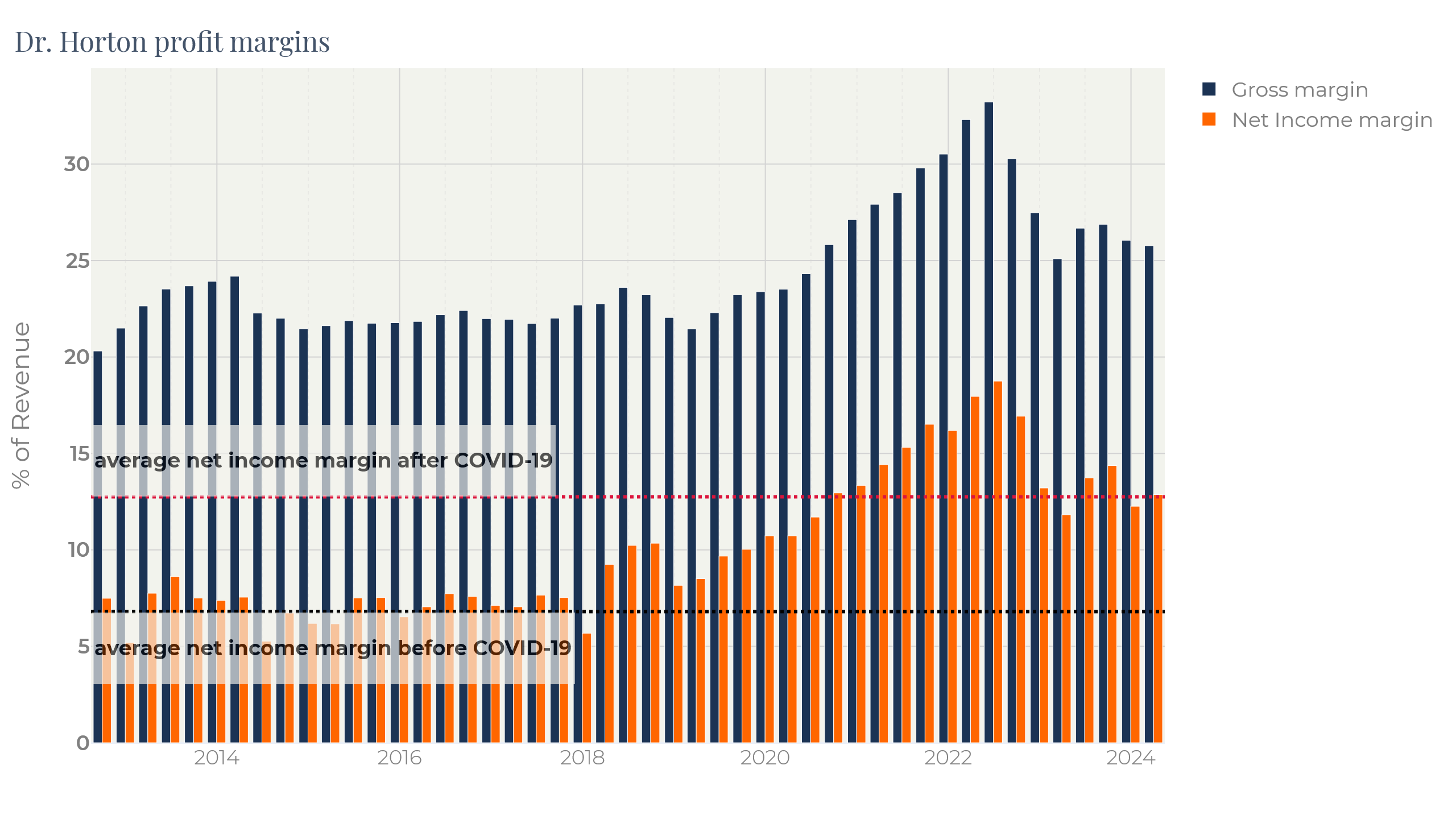

Dr. Horton’s balance sheet demonstrates the fundamental background for this move: the rise of net income is mainly caused by the gross margin expansion:

Figure 20

Inflated demand on the back of limited capacity of the homebuilders created the bottleneck in the sector. Another example of a company that became a beneficiary of this bottleneck is Caterpillar whose behavior is like one of the homebuilders:

Figure 21

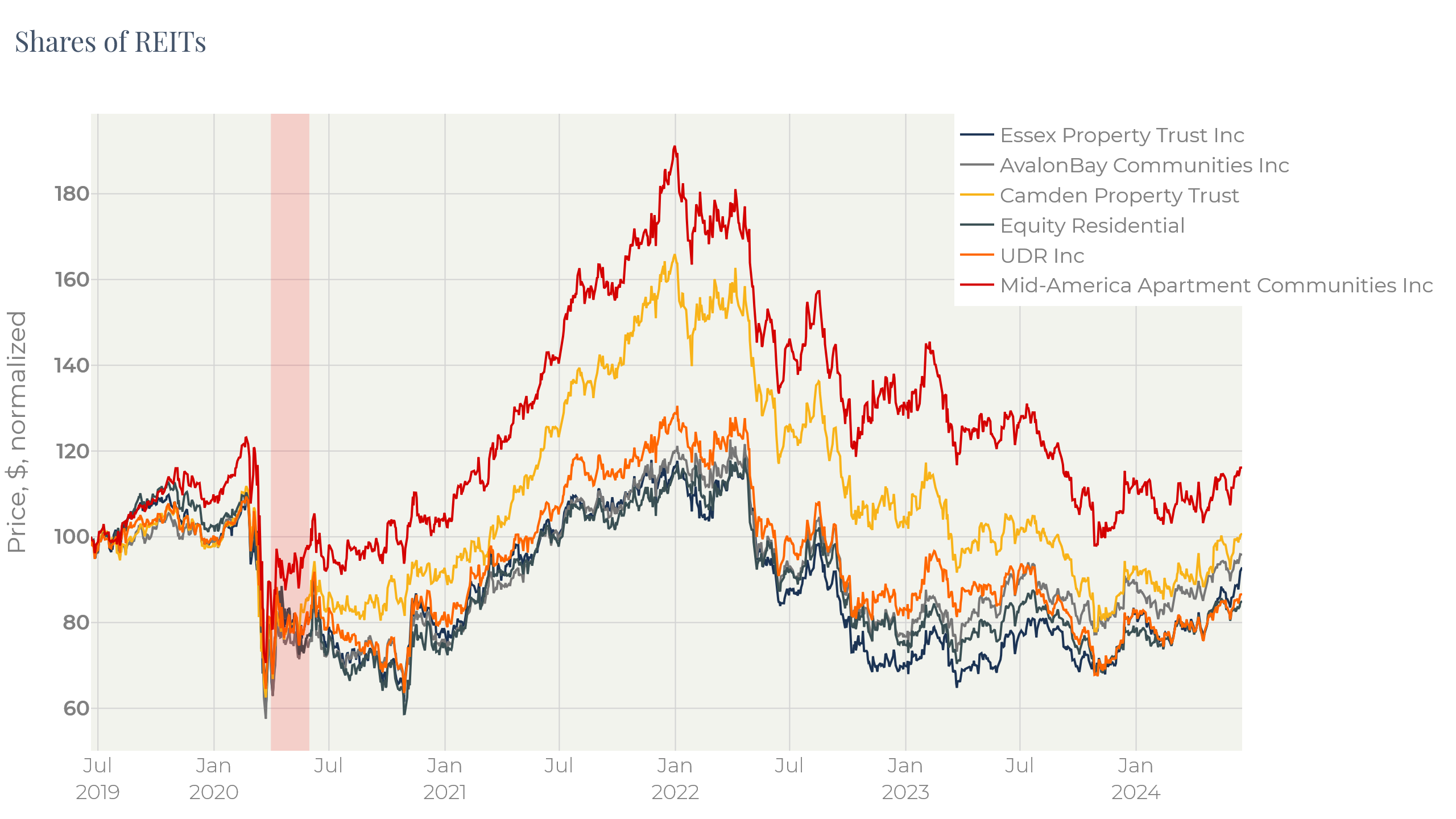

By contrast, REITs stocks does not reveal optimism (Figure 22). If the correction in 2022 seems common for the whole market, REITs did not recover in 2023 H2, unlike homebuilders. Construction companies make their profits during the whole period of construction which generally takes 1.5—2 years. REITs start feeling pressure right when demand sours. Moreover, the business model of REITs implies high leverage which eats up their profits at the opposite end.

Figure 22

Both homebuilders and constructing machinery producers are mostly exposed to new homes sales. As we mentioned above, new home sales are much solid than the existing home sales now (Figure 3, Figure 4).

Figure 23 display the pattern of two companies exposed to the existing home sales. These are Stanley Black&Decker producing hardware and tools for renovations and gardening and Zillow which is a marketplace for the real estate market.

These companies have different sorts of businesses in different sectors. However, having an exposure to the secondary property market makes the behavior of their stocks similar.

Figure 23

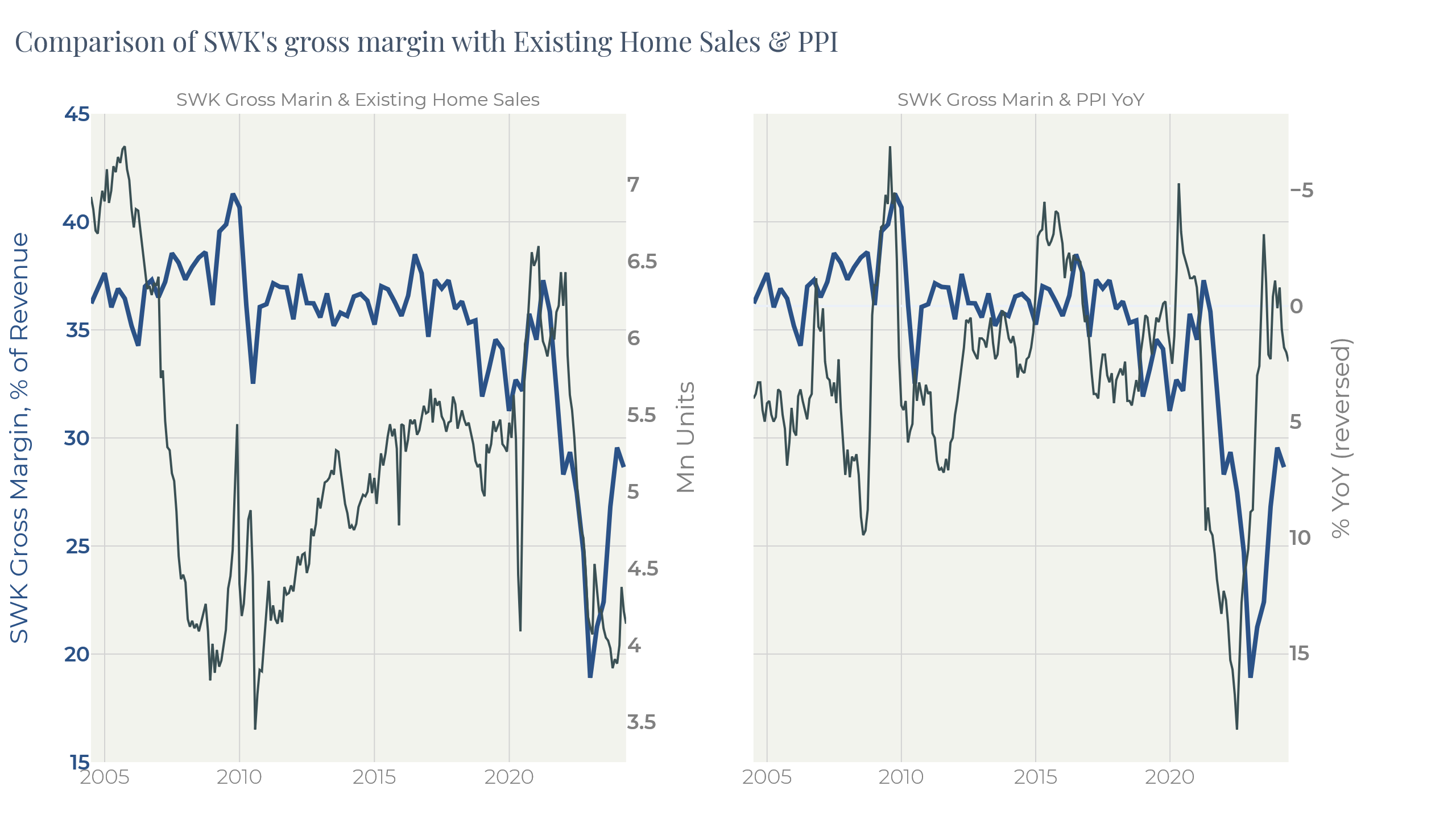

From the property macro perspective Stanley Black&Decker is affected by basic material prices (the lower the better) and the secondary market activity:

Figure 24

Since 2021 SWK has fallen more substantially than in 2008. The difference between 2008 and the current situation is that basic material plummeted in 2008 compensating the drop in sales by lower production cost. Now there is a rare combination of expensive commodities and the depressive property market. Although PPI has gone seriously down, it is not so low as in 2008.

The good thing about SWK is that it is hard to see a downside for the property market from current levels while any worsening of the economic environment will be accompanied by decreasing inflation. Despite that, it should be kept in mind that SWK is vulnerable to the equity market climate being a pure consumer discretionary play.

But even with this risk the company seems an interesting investment, especially in the case of a sharp economic slowdown. In such a scenario inflation will drop quickly and the Fed will be forced to reduce the key rate quickly. This always led to recoveries in the property market. The soft landing is less preferrable for the company as in this case both inflation and rates (hence, mortgages and the secondary market) will normalize slowly.

Figure 25

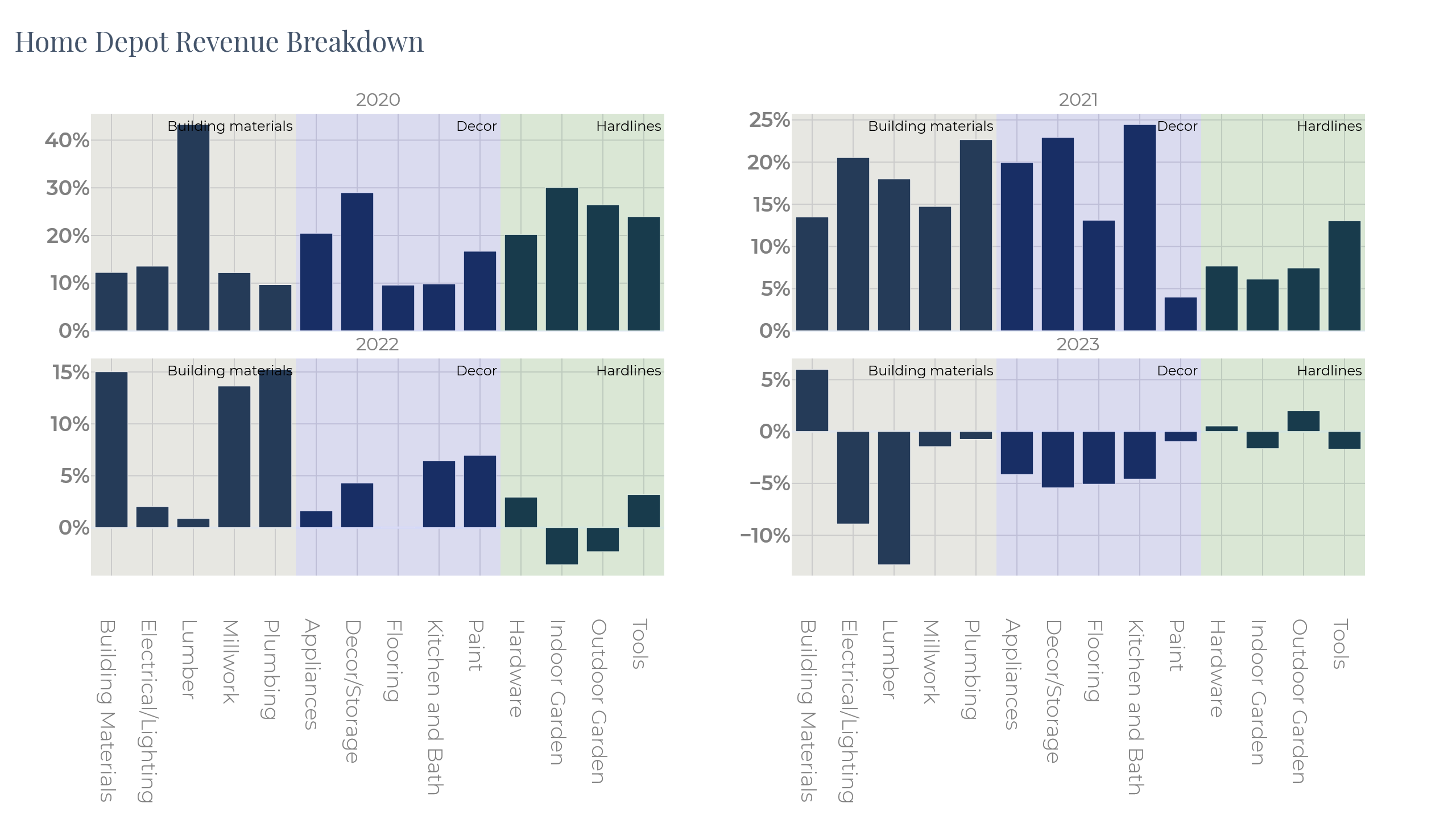

Home Depot revenue breakdown taken from the reporting of the company (Figure 25) provides an interesting insight in consumer preferences.

SWK is present in the hardlines segment. It spiked in 2020 in the back of COVID-19 restrictions. People, being locked in their houses, started improving their home and garden environment and upgrading their houses to house-offices. This trend remained in 2021 but was totally gone in 2022.

Building materials and décor gained momentum in 2022 coming along with the construction activity (Figure 5).

It is interesting that only two segments have remained positive during all four years: basic building materials and hardware. Both segments are mostly exposed to the construction of new homes. DIY tools, decorative materials and goods for the final renovation stage have gone into depression by now. In some cases, it also reflects series price corrections – this is the case of lumber.

Homebuilders’ stocks are priced now relying on the assumption that the current margin levels are stable. This makes them vulnerable to drawdowns of demand on construction. Meanwhile, this risk is not low.

Decreasing demand on materials and goods for renovation, weakening demand on the new rent and signs of a slack in consumer demand on the back of shrinking household savings might mean that demand on primary construction is nothing more than a consequence of already started projects that must be finished now. Given the current price level of houses and overheated employment in the sector which has reached pre-GFC levels, the downside risk for homebuilders and construction hardware producers cannot be ignored.

Even if the stocks do not go down, long-term stagnation in this segment is highly possible.

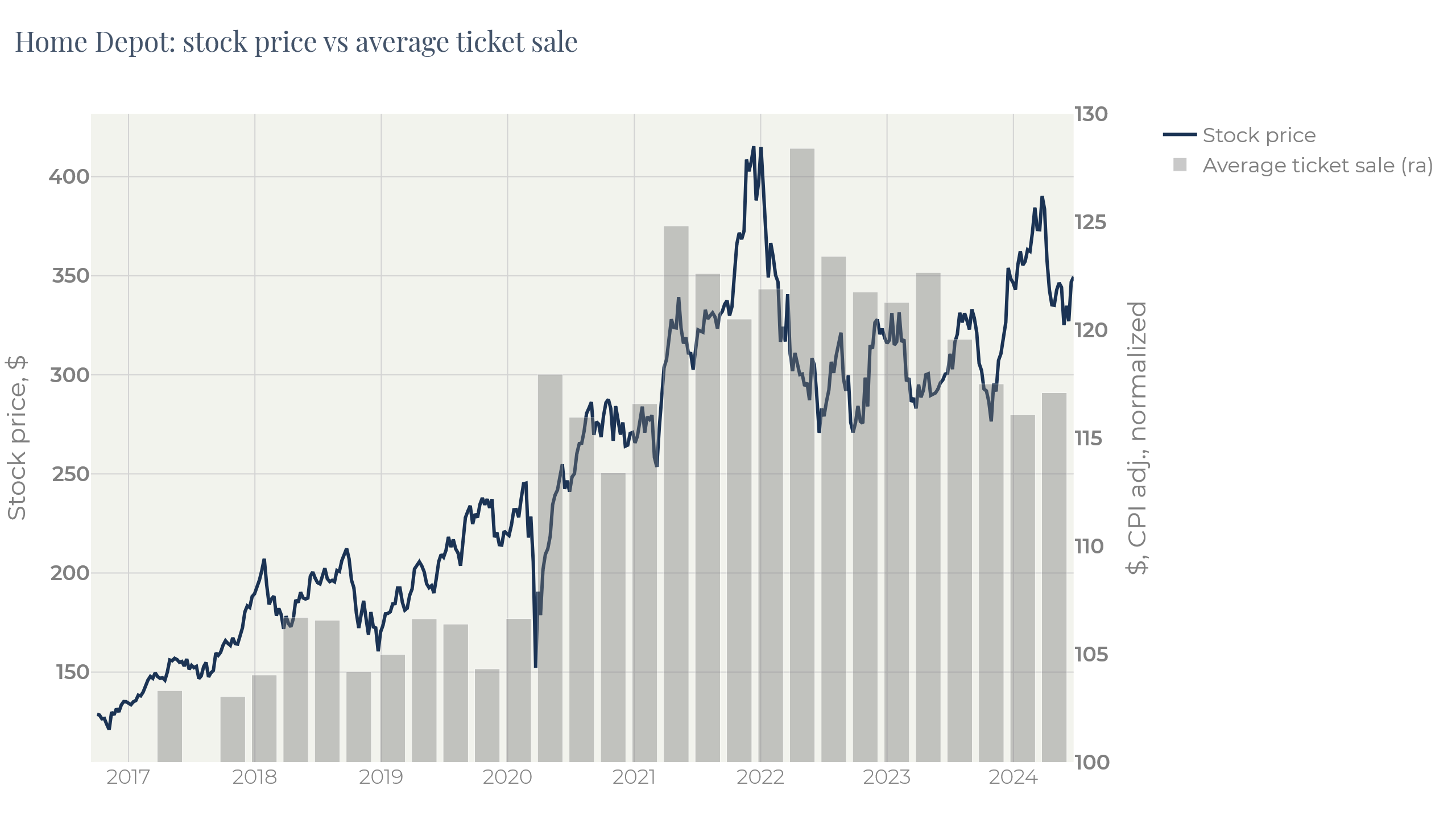

Home Depot is a typical example of a company already experiencing slowing of consumer demand:

Figure 26

As one can see on the Figure 26, average ticket sale looks overheated even after the inflation adjustment. After it reached its top and demand soured, the shares behavior turned into a stagnation mode.

Summary

COVID-19 changed the macro environment and led to overheating in the construction industry and property prices. Home prices, rental rates, employment in the industry, construction activity surged to the levels typical of pre-GFC environment. Some companies, above all those exposed to the primary property market, became the beneficiaries of this process. Those exposed to the secondary property market did not manage to take advantage of ongoing processes. One of the major reasons for this market behavior is huge anti-pandemic monetary stimuli. The excess of savings, though, is nearing the end which we highlighted in other our commentaries. Stock prices of homebuilders and constructing hardware producers do not fully account for this risk which makes such companies vulnerable to possible economic slowdown on the back of restrictive monetary policy conducted by the Federal Reserve.

1 . Camden sees favorable trends in insurance, taxes and bad debt (https://www.multifamilydive.com/news/apartment-REIT-Camden-housing-supply-bad-debt-expenses/716218/)

© 2022. All Rights Reserved

All content of this site is for informational purposes only and is intended for qualified investors. Information provided on this site is not a promotion or advertisement of securities and/or investments, is not an offer to sell or solicitation of an offer to buy any securities, funds, investment instruments, products or strategies, and should not be considered an individual investment advice or recommendation. Financial instruments mentioned on this website may not be suitable for your investment profile, experience, investment goals, risk and return objectives. Before making an investment decision, investor needs to independently evaluate the economic risks and benefits of such investments, tax and legal consequences of investing, his/her willingness and ability to accept such risks, or consult with his/her investment adviser. Movchan’s Group companies and employees are not investment advisers and are not responsible for possible losses of the investor in case of investing in the financial instruments mentioned on this website. Information provided on this site does not guarantee or promise any future investment returns. Past investment returns do not guarantee or promise any future investment returns.